Electrifying Automotive Financing for EV-eryone

Electrifying Automotive Financing for EV-eryone

How Tenet is revolutionizing electric vehicle financing

Welcome back to The Innovation Armory! This week’s post is about the opportunity to supercharge EV adoption by transforming the framework for consumer auto loans to focus on characteristics unique to electric vehicles. Thanks to Andreas Wallendahl, COO & Co-Founder of Tenet for sharing your perspective for this piece. Read on for more about:

The purchasing power disconnect in EVs driven by demography

How Tenet allows consumers to unlock EV financing at lower upfront and effective costs

The impact of higher residual value, distinct depreciation curves and lower ESG cost of capital on EV financing potential

The opportunity to bundle EV financing with other smart home hardware financing including virtual power plant (VPP) systems

Why incumbent lenders are slower to move in the EV auto loan space

The opportunity to sell picks & shovels to global used car marketplaces

This is a long post so if your email gets clipped at the bottom, make sure to click unclip / visit The Innovation Armory to check out the full read.

If you liked this piece feel free to subscribe for future updates below:

Or share with your friends below :)

The Purchasing Power Disconnect for EVs

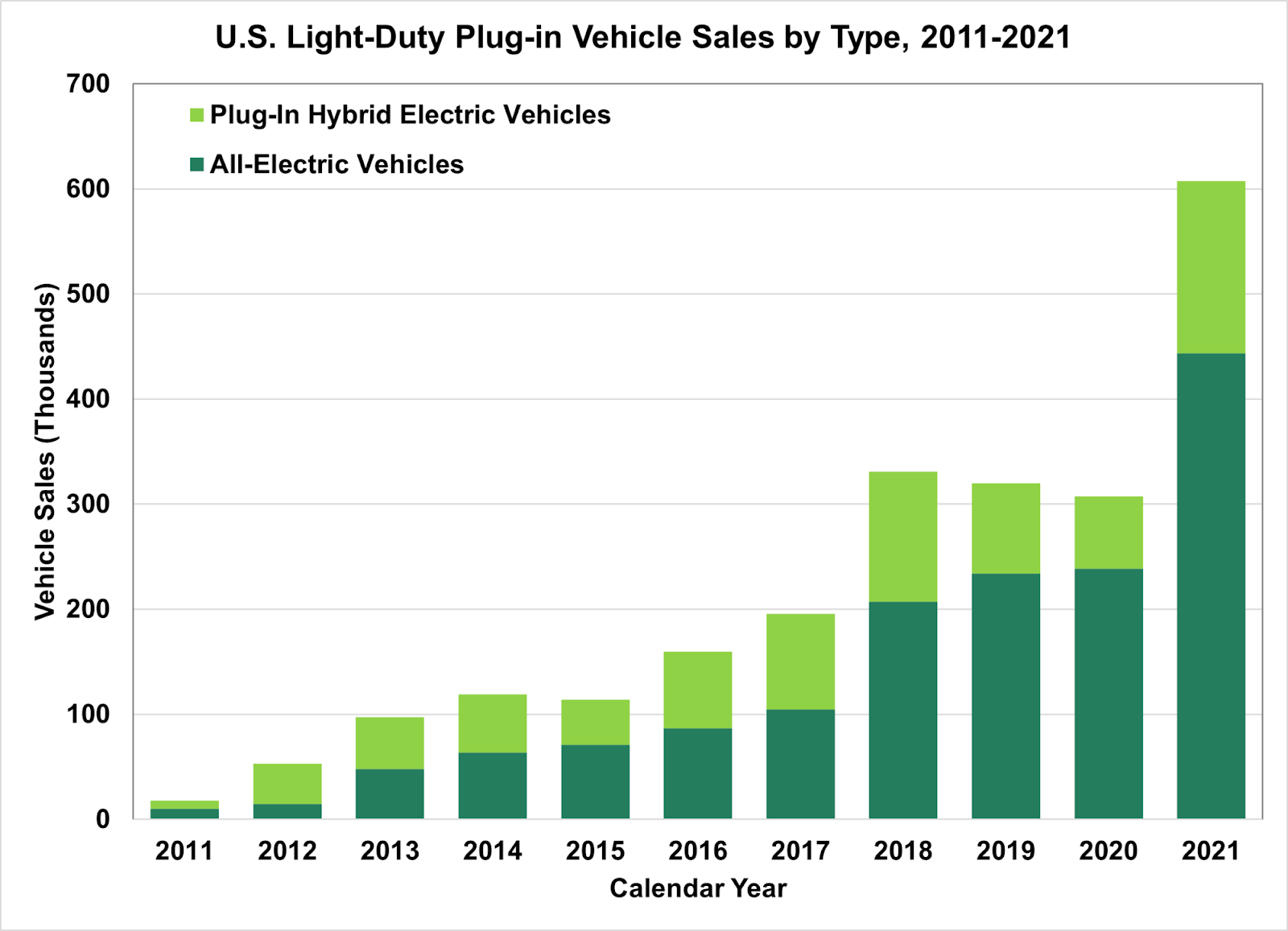

Electric vehicle purchases in the US have been rising rapidly over the last couple of years with OEMs releasing new EV models and scrambling to get a piece of the action from early entrants like Tesla. According to the Department of Energy, total EV unit sales (including plug-in hybrids) grew by nearly 100% in the US in 2021:

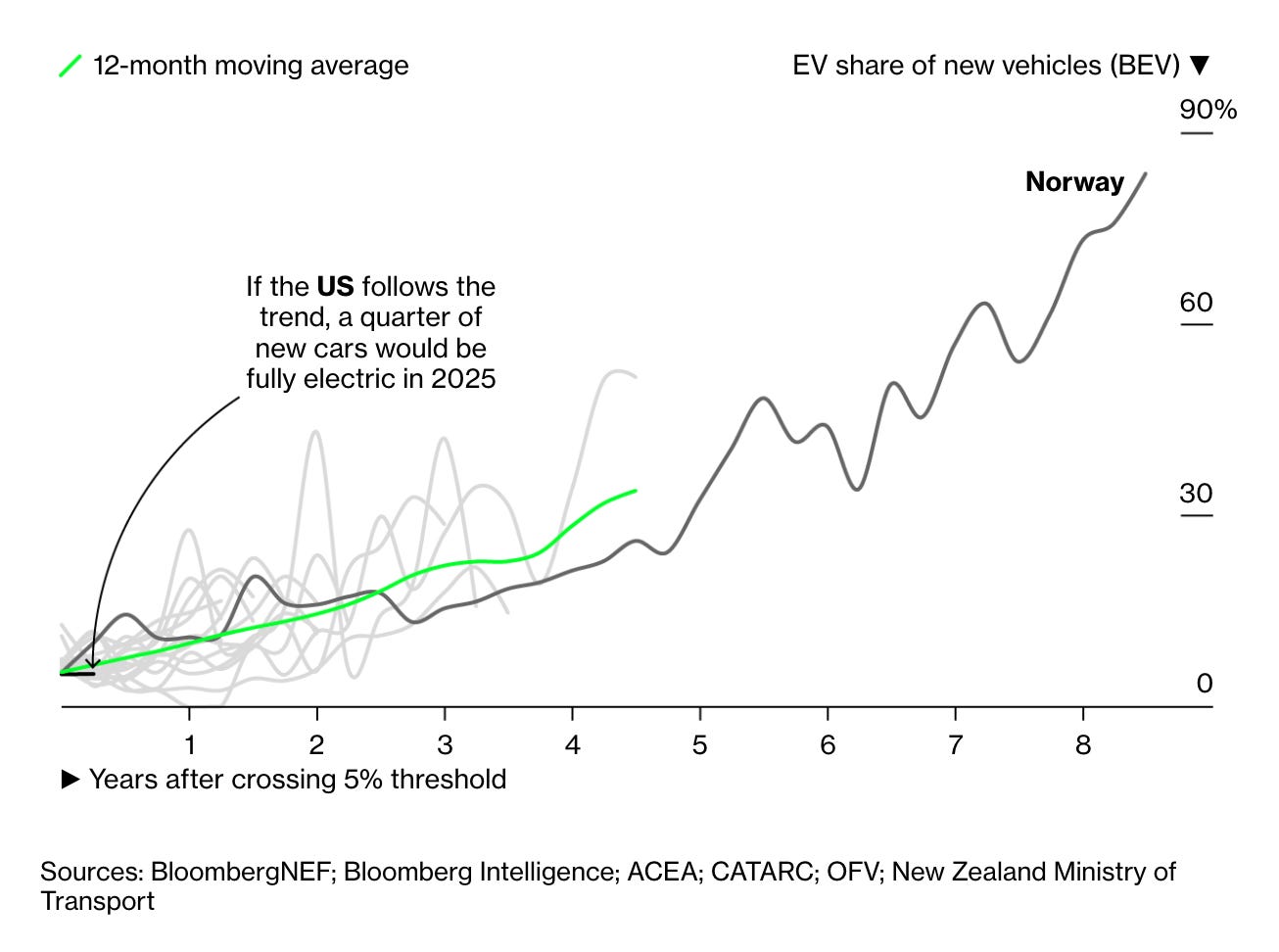

The US recently crossed a penetration rate of 5% (% of all new vehicle sales that are EVs), which some industry experts believe is an important inflection point when it comes to adoption demand. In a cohort of 18+ developed countries that have crossed this threshold, there appears to be an acceleration of sales past the early adoption phase to a phase of more reliable demand for electric vehicles. If the US follows the same curve as other developed countries that have crossed this 5% threshold, nearly 25%+ of new car sales could be electric by 2025!

If this is the case, the US government has a lot of work to do to improve our “no outlet” signage for the electric vehicle age to avoid a tremendous amount of confusion 🙃:

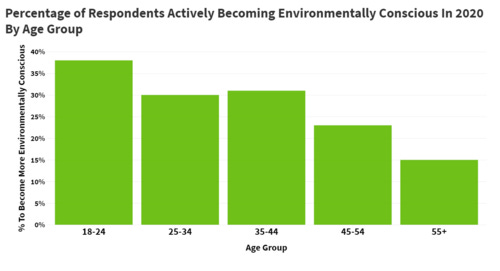

As electric vehicle sales have risen, there is also a disconnect between age cohorts that want to transition to a sustainable / green lifestyle and those that are most able to afford electric vehicles. The average upfront electric vehicle transaction price is $10,000 higher than traditional vehicles and this amount is higher (at least on a % basis) in the lower end of the vehicle distribution for starter and commuter cars when you exclude luxury / sport. However, younger cohorts that have had less time to accrue and build wealth are the most excited to accelerate adoption of greener lifestyles. According to a HelloFresh study, as of 2020, nearly twice as many millennials as baby boomers were prepared to actively adopt green lifestyles. This amount will be higher today in 2022, but the relative age effects should still scale:

I know what you’re thinking - what does HelloFresh, a meal delivery company have to do with green travel? Don’t worry, their study covered travel and food :) habits.

Across cohorts there have been two separate adoption issues:

Older, richer cohorts that are more financially motivated are less likely to buy EVs when they can instead buy traditional luxury vehicles for less money

Younger, less wealthy cohorts that are more socially and environmentally motivated are less likely to have the financial wherewithal to buy EVs

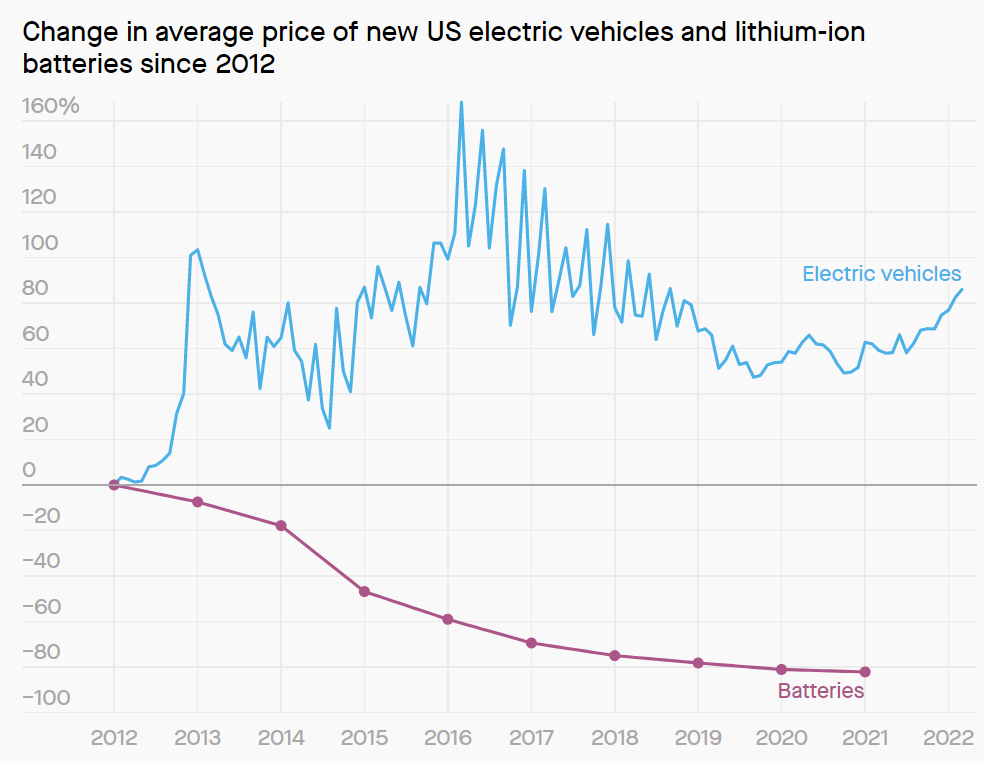

If the upfront cost of EVs decreased, older cohorts would be more financially likely to substitute their traditional car choice and younger cohorts would also have greater access. In the US, however, EV prices have risen over time (partially driven by the recent car shortage). This is a bit confusing at first because battery technology costs have decreased pretty rapidly, innovating at a rate much faster than many industry experts thought would occur. One of the main drivers of this increase has simply been because early EV models have been focused on the luxury category while EVs are still in their early adoption phase. Since 2012, battery costs have dropped nearly 80% but EV sticker prices have simultaneously risen by a cumulative 80%:

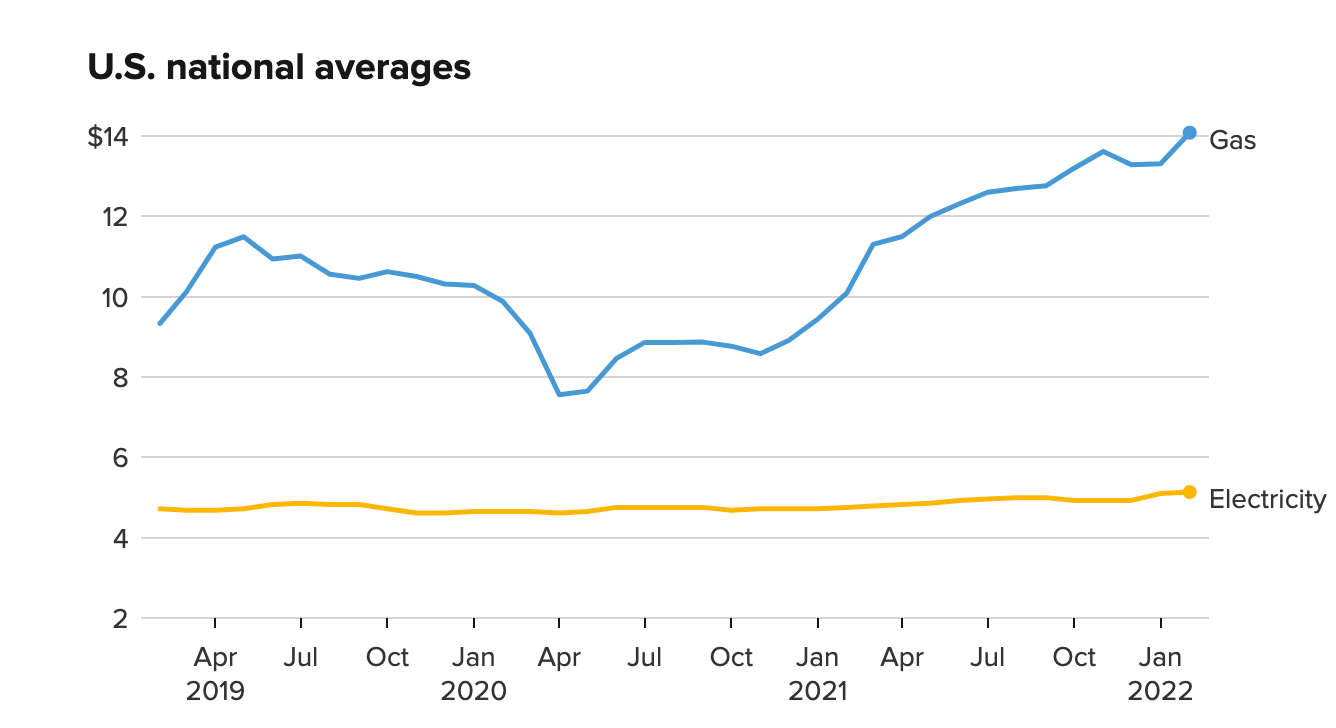

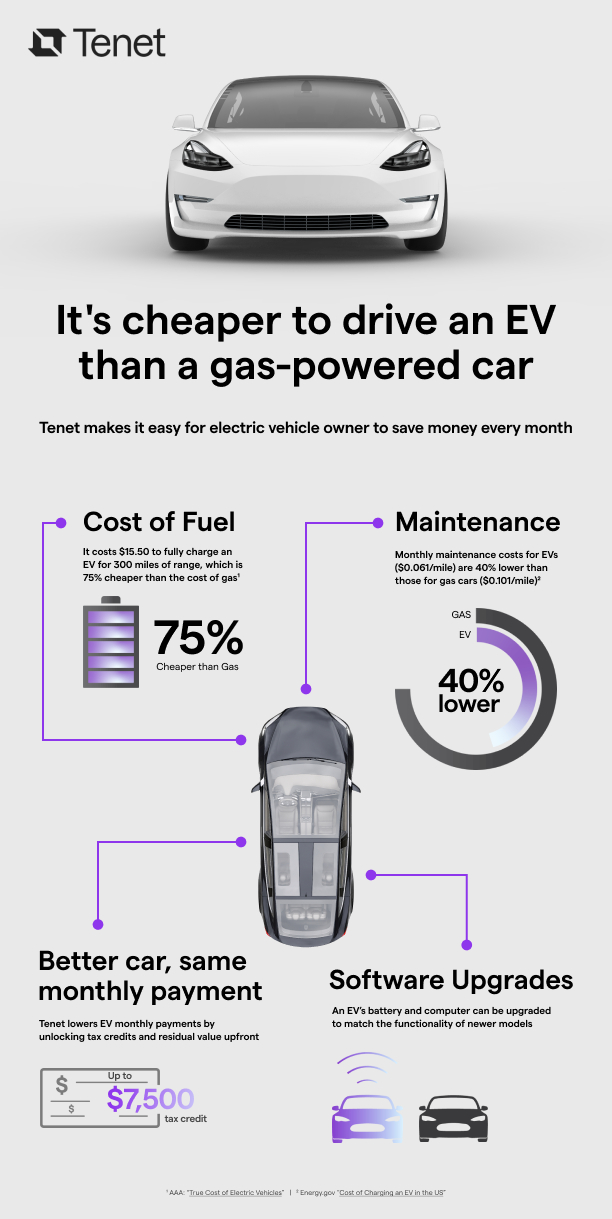

As the underlying battery technology in EVs improves, until there is further adoption and more budget models of EVs are released, they won’t necessarily correlate 1:1 with commensurate pricing drops in the vehicles. The total cost of ownership of electric vehicles (especially when you factor in the impacts of green subsidies in certain states) is actually lower for longer vehicle hold periods because of how much cheaper it is to fuel with electricity instead of gas, particularly in the current inflationary environment. The below chart shows the cost of adding 100 miles of range to an average vehicle using gas vs. electricity. The disparity is even greater now as gas prices have risen at a much faster rate since January!

At the end of the day, financially, there are many consumers who would prefer to purchase an EV especially at current gas price levels, but who aren’t able to afford high short-term lease costs given the higher sticker price. For many customers, the choice not to purchase an EV is driven by a cash flow issue. What if there was a different vehicle financing alternative that solved this cash flow issue by deferring payments towards the end of the lease at more attractive rates?

Electric Vehicle Financing is Stuck in the Past

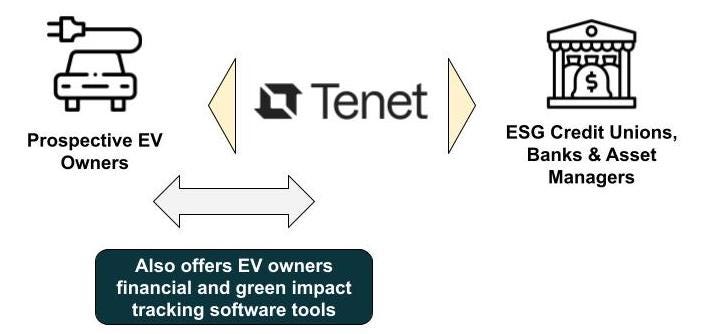

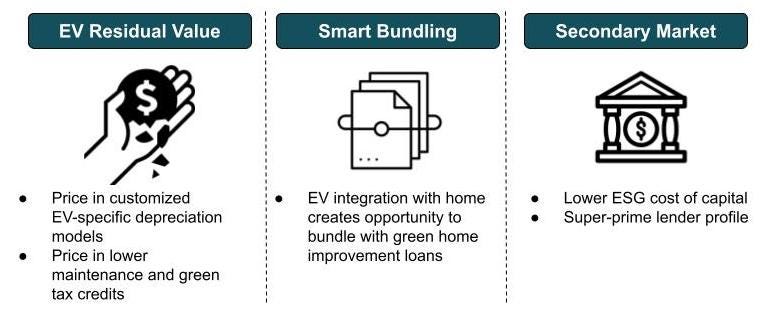

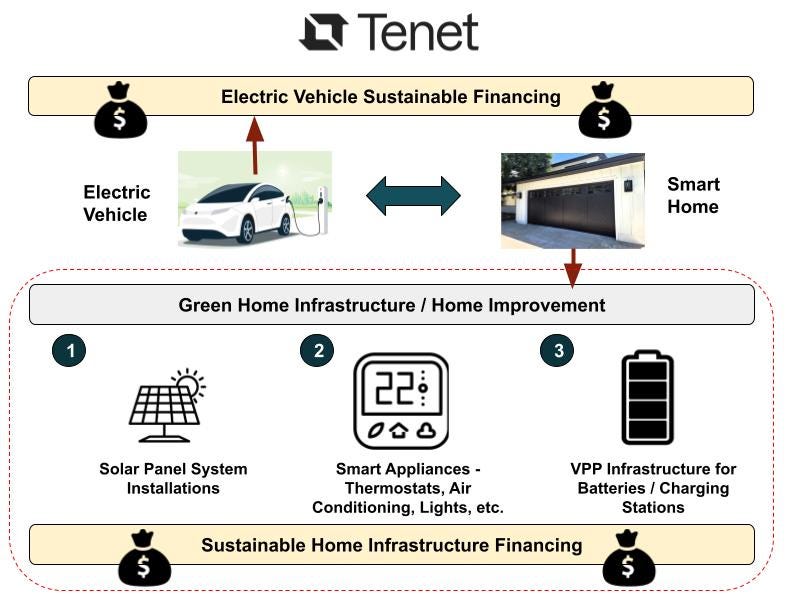

Unfortunately, to-date automotive lenders have applied the same financing models from traditional vehicular financing to electric vehicles. Tenet is building an “electric bank”, starting first by offering electric vehicle financing alternatives that allow the average consumer to unlock the value of EVs at a lower upfront cost and lower cost of ownership. While the business is starting in the EV space, it also plans to expand over time into home improvements related to green technology and sustainability. Tenet uses EV specific depreciation models as well as the benefit of lower car maintenance and green tax credits to price loans for more expensive vehicles at comparable or lower monthly payments terms to traditional vehicles. It doesn’t hold most of these loans but rather connects EV owners with ESG-minded credit unions, green banks and asset managers.

The application of traditional automotive financing models to EVs has constrained the growth of the EV market by providing potential consumers with less attractive financing options on a relative basis. By offering financing specifically tailored to EV profiles, Tenet is able to offer lower monthly payments. Tenet’s model capitalizes on some unique dynamics in the primary and secondary electric vehicle financing space that are quite distinct from traditional automotive finance:

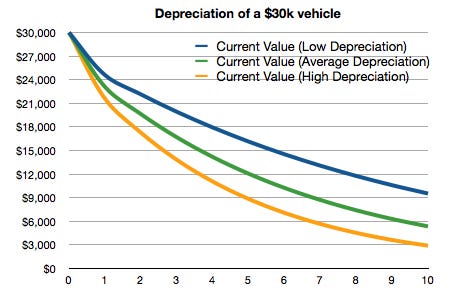

Residual Value / Depreciation Models - traditional auto loans are structured around solving for traditional automobile depreciation curves, which differ pretty meaningfully from EV curves. Tenet is betting on the fact that depreciation curves will be less steep for EVs especially as they mature further and will yield higher residual values as compared with standard depreciation curves. This means that monthly payments can be lower and loans can be structured with larger balloon payments towards the end of a lease tied to a higher residual car value:

Higher end electric vehicles like Tesla’s Model S have residual values of 71% after 3 years, above the industry average. In certain markets, OEMs like Mercedes-Benz are already predicting higher resale values for electric vehicles over traditional automobiles. While there are numerous factors that contribute to this potential for higher residual value in EVs, a couple of the highest impact contributors include:

Technological Innovation - Tenet is betting on the fact that at scale electric engines will fundamentally depreciate at slower rates than internal combustion engines. The pace of technological progress in battery technology is promising here in terms of driving battery charge speed and longevity. As Tenet prices more EV loans, it will also have the data to pre-emptively predict the impact of innovations on depreciation curves before new models are even released.

Smart Batteries - EV OEMs are configuring their batteries and computers in such a way that enables them to receive remote software updates. This allows current models to avoid obsolescence in the same way that “dumb” combustion engines on standard vehicles don’t. The ability to administer these software updates can theoretically also occur in non-electric vehicles but these OEMs aren’t investing to make these powertrain systems as “smart”.

Cost of Ownership - lower fuel (especially in an inflationary gas environment) and lower monthly maintenance costs (up to 40% lower) both slow depreciation and make the residual value higher as the cost to ownership of a new buyer is higher since marginal cost of electricity is lower than gas.

Supply / Demand Imbalances - once we pass the inflection point for EV adoption, I expect there to be supply/demand imbalances as legacy OEMs look to catch up further to industry leaders (potentially also caused by battery shortage issues). In the short-to-medium term, this could have an upwards effect on resale price.

Tax Subsidies - these may not last forever, but multiple states have tax credits that make electric vehicles more valuable and can also be priced in upfront to reduce monthly lease payments. For example, the Qualified Plug-In Electric Vehicle Tax Credit can be worth up to $7,500

{kind=link}

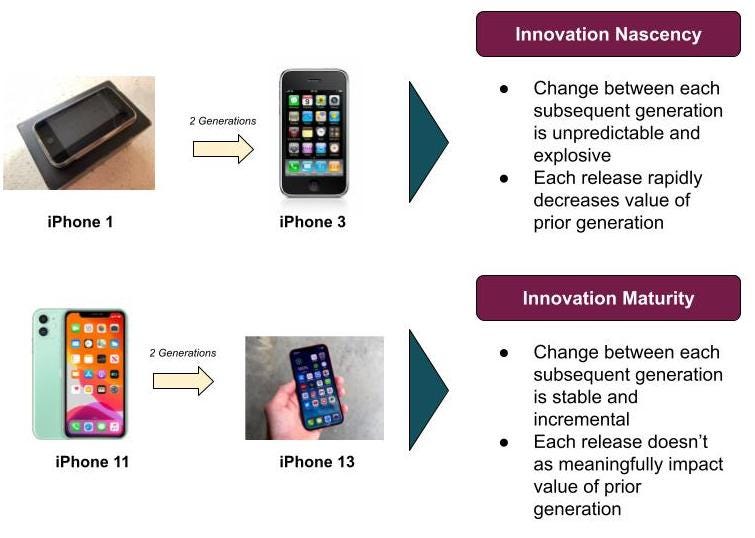

Interestingly, the pace of innovation in EVs historically cut both ways. On earlier EV models, because they were newer, the risk of technological obsolescence was higher than traditional vehicles because gains in battery technology in a new car would be “innovated away” faster. This made resale value less certain as new buyers would place more of a premium on buying new models sooner. More incremental gains today rather than massive step changes in the quality of better technology and the ability to deliver software updates seamlessly has mitigated this issue. I would argue that innovation which occurred too fast initially artificially deflated resale values at each generation vs. phasing out over a couple of generations. As the market matures, the resale value won’t be as meaningfully impacted by subsequent model releases. This is akin to how the iPhone 13 is not that different from the iPhone 11, but the iPhone 3 was much more superior than the iPhone 1 in terms of functionality.

The meaningful monthly car payment savings that Tenet is able to deliver is like a degree removed from a “drive now, pay later” model in the EV space since much of the loan payment is ballooned at the end of the lease term, except that the balloon should theoretically be collateralized to higher residual value, which is a win-win for both Tenet and consumers.

Smart Bundling - While electric vehicles can be charged at public charging stations, that infrastructure is less developed across the US today. The majority of charging activity today occurs at the home and this will continue to be a predominant means of recharge over time. Combustion engine cars are never refueled at home. Because electric vehicles are intimately tied to the home through the point of recharge, Tenet has a unique opportunity to leverage EV financing as a wedge into financing other types of sustainable / green home infrastructure. Electric vehicles often aren’t just a solo purchase for sustainably-minded consumers, but rather part of a broader portfolio of green lifestyle choices, of which Tenet can get a bigger slice of the total financing pie:

Tenet’s initial offering in the EV space also helps consumers track their carbon footprint and monthly cost savings via a software dashboard. Consumers who make a proactive choice to shift their lifestyle towards green goals likely would care about tracking green impact and cost savings across their full portfolio of smart and green appliances / infrastructure. Therefore, Tenet should be able to bundle financing packages between the automotive and home green spaces since once a consumer uses Tenet for their EV, they will value interoperability on the software side of tracking financial and green impact across all of their sustainability vectors. Moreover, building a strong brand in the EV space, which is often a first sustainability step for consumers vs. something more permanent in the home, gives Tenet a marketing advantage in the broader consumer sustainability financing space.

Beyond solar installation, there are some really interesting virtual power plant (VPP) applications that Tenet has the potential to track and also price into its loan pricing algorithms. VPP systems are a form of decentralized power grid whereby fragmented users, homes and devices effectively contribute power back to the grid in a decentralized fashion and are compensated for their value-add. The purpose of VPP is to allow utilities to more effectively coordinate distributed power resources to solve supply / demand power gaps at moments of peak power usage in the local grid. Both smart appliances and home batteries can have implications for “passive” and “active” VPP:

As Tenet expands into home financing, it can leverage its software package to help homeowners track their savings and impact from VPP assets. It can also serve as a lead generation source for utility companies to source assets for VPP that are already connected into Tenet’s financing and tracking platform. Because assets are compensated for VPP contribution, Tenet’s asset data on VPP can also help it further price these sustainable home improvement loans at more competitive rates over time if Tenet can also earn a margin as a VPP market maker between homes and utility companies.

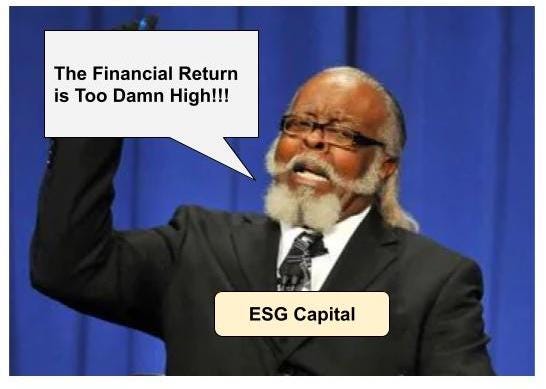

Secondary Market - Tenet sells its portfolio of loans in monthly take-outs to largely credit unions but also some green banks and ESG asset managers. It works with financial institutions that are ESG focused and because of that, they have a different returns profile on debt transactions. Because their investors care about environmental and social impact, they are benchmarked to a mix of green impact and financial returns so these institutions can sometimes have a lower cost of capital. This lower financial returns threshold allows Tenet to offer more competitive rates even on loans that defer payments due to high residual value on EVs.

In reality, many ESG investors would argue that their returns are superior when you price in the negative externality of carbon emissions into the business models of non-ESG investors. They are just preemptively pricing it in before government regulations catch up. Separately,, credit unions and ESG financial institutions will buy paper with these competitive rates because of how super-prime the current base of EV owners is. 65% of EV owners are over the age of 40, 70% are college educated and nearly 70% make more than $75,000 per year. By virtue of EVs today being a luxury class of vehicle, the owner base is super-prime by automotive financing standards. Paradoxically, as technology improves and OEMs offer more budget electric vehicle models, this cohort may converge with the current prime status of traditional auto companies. Still, in the short-term this superprime cohort dynamic gives Tenet an advantage in selling its loan portfolios to ESG financial institutions through lower default rates.

EV Market Doesn’t Quite Move the Needle Yet for Incumbent Lenders

Electric vehicle financing is still a relatively small part of the total automotive financing market. In 2020, electric vehicle financing represented 8% of new vehicle financing. This is changing as the rate doubled to nearly 16% in 2021. However, this completely ignores the used car market which is nearly 0% EV. This is because a) EV technology is newer so used supply is naturally lower / there are fewer sellers, b) buyers tend to hold EVs for longer to recoup more value from a higher upfront cost and c) residual values on the earliest models were deflated due to the the aformentioned technology obsolescence factor in early generations discussed above. However, used car financing represented a majority of the automotive financing market as of Q2 2020 (60%). This represents pre-covid levels and is likely meaningfully higher now given a) the growth in used car marketplaces and b) the new car supply chain shortages. Therefore, when you include the used car market (which is growing faster than new car sales), EVs probably represent somewhere between 5-8% of total automotive loan volumes on a blended basis.

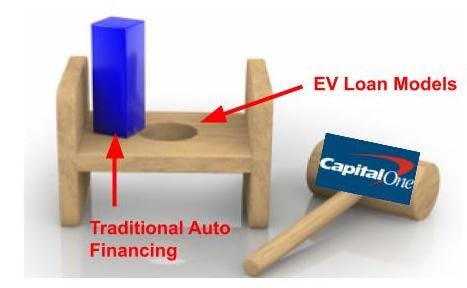

While this is a large market, traditional auto lenders like Capital One (largest auto financer in North America) feel the need to prioritize the traditional auto finance space and capture more market share there to most move the needle on their top-line growth. More saliently, even though larger financers like Capital One go after the EV market, the market historically was not large enough for them bear the costs to carve out separate lending policies and protocols from their core auto business. This makes them less competitive in the short-term as they’re trying to fit a square peg in a round hole, namely servicing EV loans with traditional auto financing models:

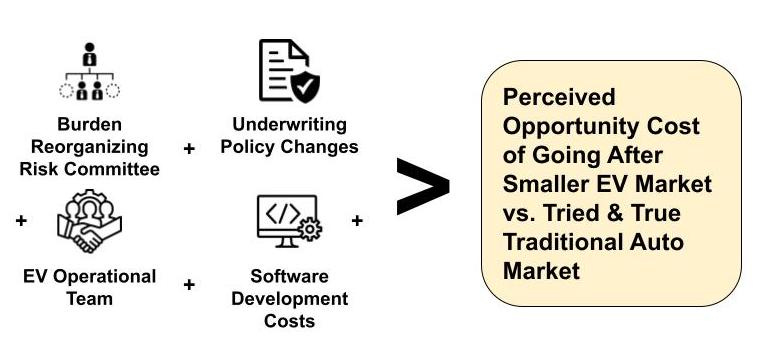

When you utilize the same depreciation, residual value, maintenance and tax assumptions to structure EV loans as traditional auto loans, the loans will inevitably result in less compelling consumer finance offerings for vehicle owners. Given a smaller market size, it isn’t necessarily economically worthwhile for these institutions to create bespoke EV financing products that are wholly separate from their traditional auto business. This would require creating a whole host of costly operational changes for FIs including building out a decision tree of different underwriting criteria, totally different policies for adherence and wholesale changes to the risk committee process. If the EV underwriting process should truly be distinct as Tenet stipulates, this requires spinning up a new business unit to go after a smaller pie and risks losing share to traditional financing competitors from lack of focus in a core market. Moreover, software development is not the core competency of these institutions so building the same level of financial dashboard and impact tracking software that Tenet has may prove challenging:

Despite the fact that traditional FIs like Capital One feel less incentivized to create bespoke products for the space given current market size, 61% of car buyers believe that EVs are the future. However, 59% are concerned that they are too costly. I believe that Tenet is going after the EV financing market at a unique window where they will face less competition from incumbents, but be able to build a brand that will well capitalize on rapid TAM growth over the medium-term that comes from:

Declining EV costs from OEMs as they launch budget versions of electric vehicles as the broader technology becomes more mainstream

Greater availability of used car EV inventory (as earlier cohorts age) - more on this later

We are on the precipice of a rapid TAM expansion - the doubling of new vehicle financing % for EVs in 2021 is an early indication of that. The expansion will only accelerate faster when EV prices drop into a range that is more accessible for millennial and younger cohorts. Tenet is building the brand, the wedge into home sustainability financing and the loyal customer base to lock down this sleeper market early while incumbents still focus on whitespace in their core segment. Until the minnow swallows the whale as EV sales rapidly overtake traditional vehicle sales long-term…

Over time, the potential market here is even larger than the consumer sustainability financing space (EVs and home) including add-on products and commercial financing:

Selling Picks & Shovels to the Used Car Mania

According to Cox Automotive, used car sales hit an all-time high in 2021 of 40.9 million vehicles, up about 10% over 2020. Sales are down in 2022 as the pandemic has eased and new vehicle starts have slowed. However, the market remains competitive amongst used car marketplaces who are fighting for share in an increasingly challenging macro environment. Over the last cycle, there was an explosion of businesses that rode the funding wave in the used car marketplace sector across the globe. Here are a couple of global leaders:

As discussed earlier, across these used car marketplaces, penetration of EVs as a % of total inventory base is very small because of the relative age of the EV cohort compared to standard vehicles. As the heavily funded used car marketplace competes globally for market share, Tenet has an interesting opportunity to strike partnerships to help these marketplaces penetrate EVs as their next leg of growth and also to differentiate from one another by attracting EV buyers and sellers into their networks. Since these partners have low EV supply today, it is beneficial to try to strike these partnerships early to help usher in an EV sea change in the used vehicle space, which would meaningfully grow the overall TAM for Tenet’s business beyond a focus on new vehicle sales. While it’s possible used car marketplaces could try to build out their own bespoke EV financing offerings, they may struggle if consumers place a premium on tracking sustainability activity across the EV and the home as one unit as Tenet is betting. A neutral third party like Tenet may be better positioned to create the interoperability with the home than any one used car marketplace player.

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.