Extending David’s Runway Against Goliath in D2C E-Commerce

Extending David’s Runway Against Goliath in D2C E-Commerce

Arming independent D2C e-commerce brands against brand aggregators

Welcome back to The Innovation Armory! Today’s piece takes a contrarian view on the D2C aggregator gold rush. Namely that the success of the aggregator model points to a critical need by digitally native lifestyle brands for an e-commerce operating system that empowers them to extend their independent growth runway on their own terms. Thank you to AJ Orbach (CEO & Founder of Triple Whale) for sharing your perspective for this piece. Read on for more about:

How today’s aggregators create value

The issues independent lifestyle brands face i) valuing their businesses and ii) extending their growth runway past critical scale inflection

The hidden market opportunity in arming digitally native brands to capture more value from aggregators

How Triple Whale is hooking a multi-billion dollar e-commerce OS market opportunity starting with advertising and financial analytics for Shopify brands

The opportunity to democratize aggregator value creation tactics for independent brands through a multi-modal e-commerce OS

Why lending + OS software may be the best business model to capture the most value in this emerging sector

This is a long post so if your email gets clipped at the bottom, make sure to click unclip / visit The Innovation Armory to check out the full read.

If you liked this piece feel free to subscribe for future updates below:

Or share with your friends :)

D2C aggregators like Thrasio, Branded and Merama are growing to become gorillas in the e-commerce landscape on the backs of independent e-commerce businesses. According to Crunchbase, over $2.3 billion dollars in investment has flown into the D2C aggregator space throughout 2021. While Thrasio pioneered the D2C aggregation model starting in 2018, these platforms are popping up all over the world and have a presence across US, European, Asian and Latin American commerce marketplaces including Amazon, Shopify, Flipkart and Mercado Libre.

While D2C aggregators often try to position themselves as technology businesses, they make money effectively as tech-enabled private equity firms that use best-in-class data and technology tools to acquire and scale independent e-commerce businesses. The three primary sources of value creation for these businesses include:

Multiple Arbitrage - larger portfolios of D2C brands will trade for higher valuation multiples than small, nichey independent businesses on commerce marketplaces that often only have between a couple hundred thousand to $1 million of sales. Scaled consumer brands can trade anywhere from 8x - 12x+ EBITDA depending on the quality of the business. Sometimes D2C aggregators are able to buy small lifestyle businesses for as low as 0.5x-1.0x EBITDA (at the low end), albeit this has been creeping up over time to 3-5x. If you’re not familiar with multiple arbitrage, here’s the layman’s definition 🙃:

The issue is that small sellers are less financially sophisticated, often don’t understand the value of their own business at scale and most saliently will hit a growth plateau once they reach a critical phase in their business lifecycle. In effect, when your brand is sub-scale and you face capital constraints, selling to an aggregator might be your best option in its current state even if you know your business will be worth meaningfully more if scaled further. Aggregators capitalize on these factors to acquire lifestyle businesses for quite cheap relative to what they expect them to be worth at scale or when folded into their broader corporate structure.

Growth Strategy Optimization - independent lifestyle commerce brands are often less sophisticated when it comes to optimizing growth strategies for their business specifically around a couple of key areas: 1) digital marketing and paid advertising channels, 2) channel investment and distribution mix (e.g. optimizing which commerce channel is best for your products) and 3) keyword and profile optimization to ensure better ranking placement on selling channels. Aggregators leverage seller data across a wider portfolio of brands, advanced data analytics and marketing best practices to pour fuel on the fire for these initiatives and help e-commerce brands reignite growth

Cost Savings Initiatives - larger portfolios of brands are able to better realize cost efficiencies across their brands through a couple of mechanisms. For brands with similar inputs, they can realize greater purchasing power / leverage over common suppliers. Further, for backend and administrative workflows, these brands all share a common back office, which provides operating leverage to each individual brand. Further, many aggregators invest meaningfully in more advanced supply chain capabilities to drive more efficient inventory management and demand planning

The Hidden Market in Extending Independent Commerce Runway

There is a large hidden market opportunity in providing independent e-commerce businesses the tools to stay independent for longer and data measuring tools to better understand the fundamental current and potential value of their underlying assets.

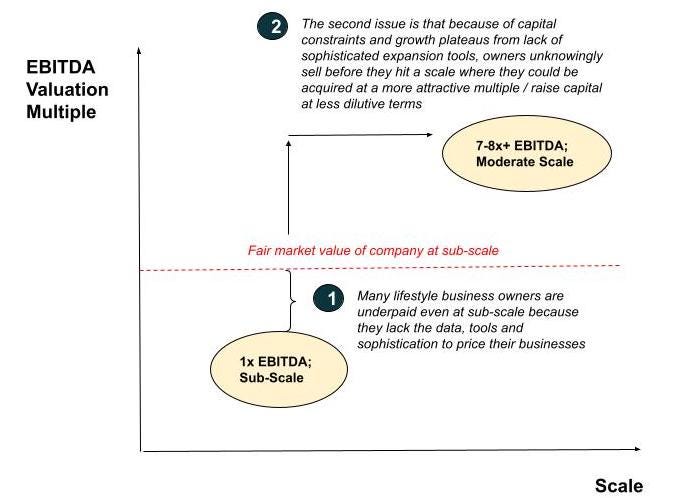

Independent e-commerce businesses lack visibility on how much they are even worth at sub-scales because they: i) can’t aggregate data effectively across various selling channels, ii) lack dashboards to track detailed customer analyses to validate the scalability of their unit economics and iii) don’t have access to data that will help them accurately forecast demand in their consumer category. Software that provides them the tools to be able to more effectively track their underlying unit economics / financials to more optimally price their business will help them move from position 1 to the red line above and leave less money on the table.

There is a separate issue that these smaller lifestyle brands will face capital constraints and growth plateaus that cause them to exit at a less attractive sub-scale multiple and choose to share in the upside of an aggregator business instead through cash earnouts or rollover consideration. In reality, there is an opportunity for many of these sub-scale brands to use best-in-class technologies to ignite growth and scale their brands to a more moderate level before selling to achieve more reasonable EBITDA multiple outcomes. Aggregators position themselves as being able to help brands overcome this growth plateau by bringing the resources of a larger parent structure to bear on a sub-scale asset. That may be true, but democratizing access to the sorts of technologies aggregators use in-house for their portfolios of brands could achieve a similar medium-term result without diluting ownership of the founder.

Independent commerce needs an operating system that will help them better resist the urges by aggregators to sell for too little and sell too early.

The value proposition for this independent e-commerce OS relative to aggregators is akin to the value of Pipe’s recurring revenue financing model for subscription businesses. Extend your business’ growth runway without selling equity or diluting ownership in your asset.

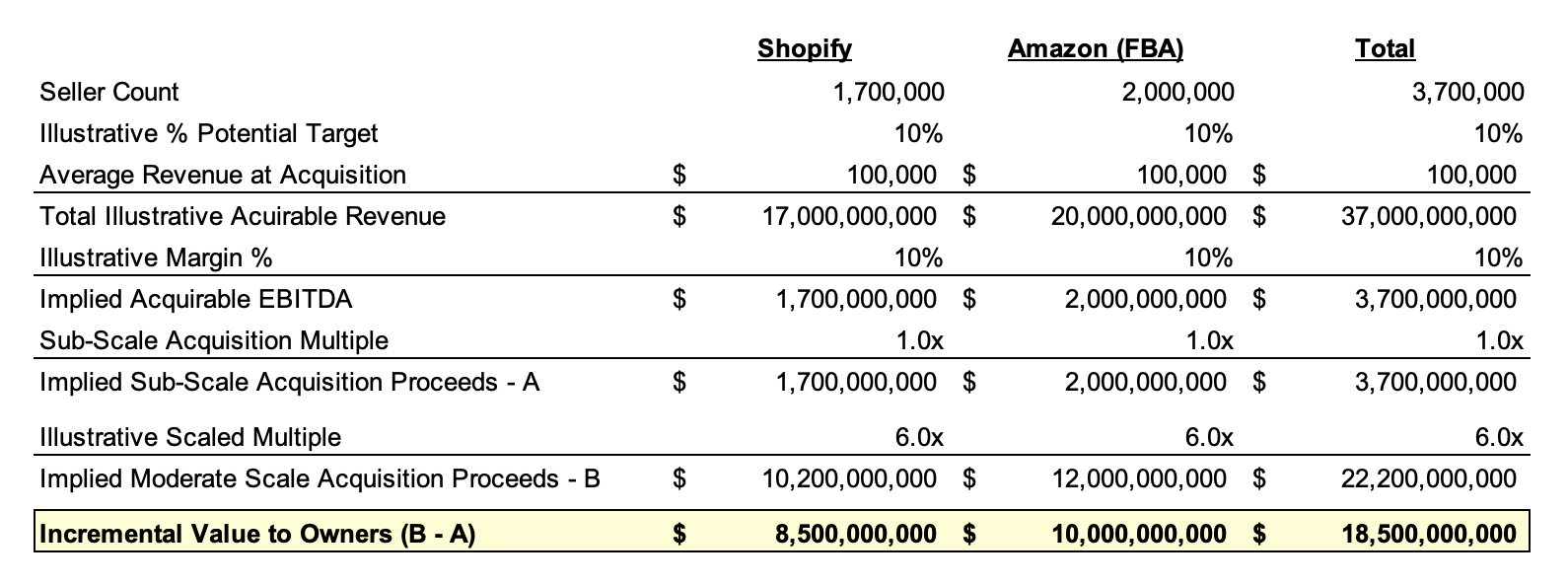

When you start doing the math on the potential value unlock just by eating into the multiple arbitrage pie alone, it becomes really clear how large the underlying opportunity is to transfer value back from aggregators to independent brand owners. If you look at just Shopify and Amazon, the potential value creation opportunity is upwards of $18.5+ billion for independent commerce brand owners where you can extend their runway and educate them about fair value of their businesses. In the below illustrative analysis, I took approximate Shopify and third party Amazon seller counts and assumed that ~10% of potential sellers fit the profile of a D2C aggregator from a sector category and size perspective. By making illustrative margin assumptions and calculating incremental proceeds from future sale at a more moderate scale multiple, there is clearly lots of value being left on the table by brand owners. Even though I made these assumptions illustratively from a bottoms up build perspective, I sense-checked the $37 billion of acquirable revenue by comparing to Amazon’s GMV attributable to third party sellers of $300 billion.

When you account for other selling platforms abroad like Flipkart, Mercado Libre and others, the total pie is much larger. If independent brand owners were educated better about the value loss they are suffering at the hands of aggregators purely from multiple arbitrage, it would open the floodgates for a multi-billion dollar market opportunity in arming and empowering lifestyle brands to scale for longer on an independent basis. I don’t think it’s unreasonable to expect an operating system that unlocks this value to capture 10% or nearly $2 billion of this value creation opportunity.

Triple Whale is Hooking the Start of a Multi-Billion Independent Commerce Opportunity

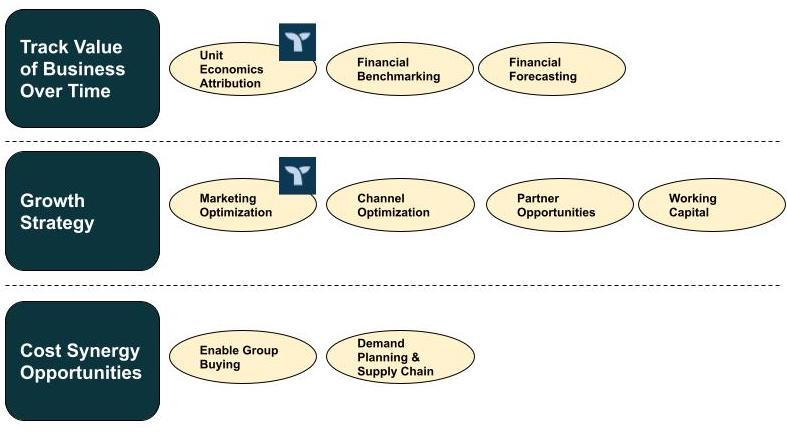

There aren’t any players today that are offering all of the capabilities needed by independent commerce players in this battle to extend their runway against aggregator goliaths. However, Triple Whale is a very promising player in the space that is building out an e-commerce operating system that helps digital first brands centralize all of their relevant financial and marketing metrics to better track their businesses over time.

Triple Whale is focused first on Shopify marketplace businesses and leans more heavily on marketing and advertising attribution analytics, but also allows business owners to track overall financial profile and profitability across their different advertising and distribution channels. Triple Whale empowers e-commerce brands with aggregator-like dashboard sophistication as its base layer and plans to add additional modules to build out a broader OS suite over time. The starting point is focused on advertising workflows, helping centralize data across key D2C advertising channels to help attribute where purchases come from by growth channel:

I caught up with AJ Orbach, Co-Founder of Triple Whale to discuss his vision for the opportunity of building an independent e-commerce operating system:

“Triple Whale is building an automation tool on top of e-commerce. We’ve engineered the centralization and visualization components to our platform and now are building out other modules on top of our e-commerce operating system (creative management, finance management, supply chain management to name a few). We are starting with a centralized dashboard / summary page where retailers can see all the relevant metrics for their brand to gain visibility over their businesses. We want to manage all of these e-commerce capabilities in one ecosystem and then use AI to automate and further optimize e-commerce businesses. While we’re focused on Shopify today, we will expand to Amazon, WooCommerce, Magento and others over time. While we see a lot of value in adding e-commerce modules over time, we are focused on a couple of specific jobs to be done at present: those of the ad buyer, the inventory manager, the finance manager and the e-commerce analyst. We believe our e-commerce operating system will help level the playing field between independent e-commerce brands and aggregators.”

Going back to our framework from Part I about the ways aggregators generate value, Triple Whale is beginning to hook a couple of these areas (basic P&L tracking, attributing unit economics like ROAS and marketing optimization), but there is a much bigger play here in building out a cross-distribution channel operating system that democratizes the types of tools that aggregators leverage in-house to track and scale their portfolios of brands.

From both a business value and growth strategy perspective, it is critical that the independent e-commerce OS eventually extends across channels. This allows for better visibility into financials across selling regions to paint a clearer picture of the current value of the business but also is important from a growth perspective to provide recommendations as to which distribution channels brands should double down on depending on relative competition, profitability and user unit economics. Over time, as businesses like Triple Whale collect more data both i) on a particular company’s performance in certain channels and ii) how comparable peers and categories are performing in that channel, these operating systems could offer more bespoke financial forecasting tools to better predict demand. This can create both cost efficiency opportunities through more efficient demand planning on the supply chain side but also help founders better visualize and articulate the future value of their businesses to would-be acquirers.

In addition to the advertising attribution Triple Whale does today, there are also opportunities for these platforms to assist in product information management and keyword optimization to boost the ranking of specific D2C products in the search results on commerce platforms. Another meaningful growth area that aggregators tend to invest in is facilitating cross-brand partnerships across companies in their portfolios. Once you become the system of record for independent e-commerce businesses, you can create partner marketplaces to help facilitate connections and collaboration between non-competitive brands where there might be underlying similar user and audience demographics (e.g. pairing sales of sunglasses and sunscreen brands in the consumer category). Operating systems that have access to the underlying advertising data by distribution and media channel will have an advantage in being able to pair potential partner brands together.

In the same way aggregators leverage common vendors to create input cost synergies for their brands, the OS of independent commerce brands track and analyze vendor payables to help pool vendor B2B manufacturing and input orders together through B2B group buying. A good example of a model to emulate here in the F&B space is food procurement technology vendors like Buyer’s Edge (BE). BE provides independent restaurants a software procurement product, but also offers discounted group buying for restaurant owners by pooling orders across different categories of F&B products. The e-commerce OS could be used as a wedge to enable similar B2B buying efficiencies across common consumer categories.

When you combine all of these capabilities together, the result is an outsourced aggregator-light software platform and B2B marketplace offering that monetizes through subscription pricing and transaction take-rates rather than through equity appreciation. I know this is the reverse of the expression, but it’s kind of like a sheep in wolf’s clothes. It looks like an aggregator in terms of the superpowers it affords sub-scale brands, but monetizes in a much more brand founder-friendly way that increases the size of the total e-commerce pie for more founders and doesn’t hinge on multiple arbitrage to generate a majority of value.

Candidly, both of those pictures are horrifying and if I were a founder, I’d be really confused and scared to pick either 🙃.

Interestingly, there is a third monetization strategy that could be one of the more effective ways to capture value from independent brands. The OS of record would have access to the paid marketing, channel profitability and customer cohort metrics to be able to underwrite and offer working capital loans with advantaged and competitive pricing to independent brands on its platform. Lenders could entice brands by offering the OS and workflow software at a discount or as a loss leader with the plan to earn most of their margin from working capital loans that help brands navigate from sub-scale to become more mature. This solves the capital constraint challenge that forces many founders to sell to aggregators in a way that is not dilutive to the founder, while still enabling the OS to create aggregator-like value through marketing, financial and other workflows. OS Software + Lending might be the goldilocks of independent commerce in terms of building the most value but also ensuring it is proportionately captured by initial founders.

If you’re interested in building or investing in the D2C aggregator space, it might be more profitable and socially desirable to take the contrarian stance that empowers independent brands with the tools to extend their runway against aggregators. This model has the potential to shift more value back in the hands of lifestyle brand founders (benefiting small businesses), while simultaneously increasing the discoverability, quality and scale of D2C targets for the aggregators over the long run.

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.