The Advertising 3.0 Revolution

How shifts in the attention economy will unlock innovation opportunities in emerging advertising ecosystems, vertical advertising infrastructure and media cybersecurity tools

Welcome back to The Innovation Armory. This week’s piece lays out a framework for the burgeoning “Advertising 3.0” technology revolution, detailing key differences vs. the digital advertising revolution of the past 1-2 decades. I also interview management at leading businesses across 5 advertising technology sub-sectors that should benefit substantially from ongoing dramatic shifts in the advertising sector. The Facebook boycotts of the past couple weeks is representative of the accelerating shift to “Advertising 3.0”. Thank you to Itamar Benedy (CEO of Anzu), Roy Taylor (CEO of Ryff), Arsen Avakian (CEO of Cooler Screens), Dylan Collins (CEO of SuperAwesome) and Daniel Avital (CSO of CHEQ) for speaking with me about how their companies are driving meaningful transformation in AdTech.

Next week’s piece discusses how intellectual and professional range predict founder success across the various stages of investment.

Advertising technology serves an attention-based industry. Marketers earn dollars by connecting members from a relevant target audience with brands and products. The location of ideal target audiences is determined by where consumers decide to allocate their attention. Attention-based economies are being dramatically shaken up by COVID-19 as audiences shift where they place their mindful attention. eSports viewership is accelerating, with Amazon’s Twitch streaming platform experiencing 20%+ viewership growth in March and 50% hourly growth from April over March. Netflix more than doubled its expected new subscriber additions due to COVID-19 last quarter. It remains to be seen the full magnitude and permanency of these attention shifts, but they will undoubtedly shakeup the advertising technology landscape which is intimately tied to attention trends. Many venture capital firms have de-emphasized AdTech as an investment area in recent years due to numerous complexities including:

Google / Facebook Dominance - Google and Facebook are massively dominant in the online advertising sector, accounting for 25% of online / offline advertising and 70%+ of US digital advertising. Amazon has become so pervasive in every part of retail, that retailers consistently use the term “Amazon Effect” to explain the impact of Amazon on other traditional retail businesses. Google and Facebook have had a similar effect in disrupting traditional advertising channels. This has created a divergence between M&A and venture capital deal volumes where there is substantially more and often distressed M&A for late-stage AdTech businesses selling to technology giants. More earlier stage VC firms have backed away from AdTech as a category given incumbent moats and due to prior experiences of being burned by AdTech businesses (for example, Rocket Fuel which went from a $2B+ valuation to selling for $100M+ over a couple of years).

Data Privacy - Most consumers do not want to trade data privacy for more targeted advertisements. However, targeting plays an important role in delivering ROI to brands who want to connect the best customers (most interested and most willing to pay) with their products. Data breadth and quality is key to delivering quality targeting. However, there are numerous privacy headwinds that cast doubt on the future viability of data-centric targeting, including GDPR in Europe, California Consumer Privacy Act and Google’s phase-out of third party cookies in Chrome to name a few. Consumer, regulatory and digital decision makers appear to be aligning on a stricter paradigm that will make effective targeting harder.

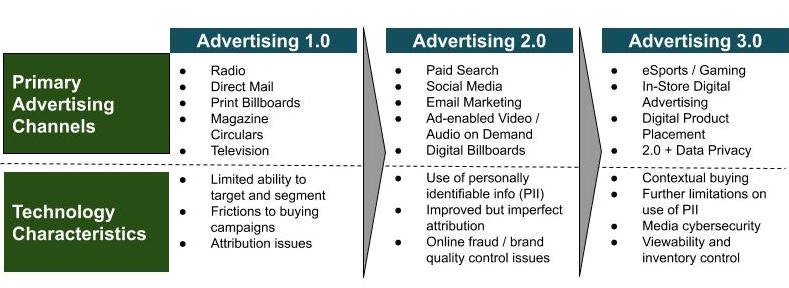

Many brands are significantly reducing advertising spend for this year with some analysts forecasting upwards of $50 billion slashed from budgets. These budget decreases will prompt brands to reconsider the qualities they will look for in advertising ecosystems and AdTech tools when they are eventually ready to re-up their marketing spend post-coronavirus. In addition, in recent weeks, Facebook has been boycotted by hundreds of its most significant advertisers including Coca-Cola, Unilever and Starbucks, for allowing the spread of hateful and fake content on the website. These boycotts should further accelerate the shift to the next generation of AdTech and create white space for new advertising ecosystems. “Advertising 1.0” consisted of traditional advertising media including print, billboards and radio, with limited technological investment. “Advertising 2.0” was the first digital advertising revolution from which Google and Facebook were the largest beneficiaries. “Advertising 3.0” is coming. Investors and founders should realize that platforms with “Advertising 3.0” qualities will shape the new reality of advertising ecosystems and have the potential to win big as customer attention shifts have cascading effects on advertising wallet shares. Below is a summary of this advertising evolution over time:

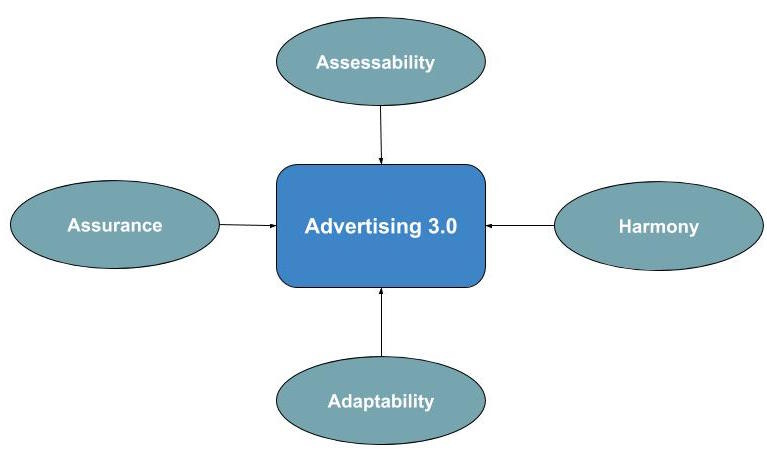

What core features are part of the ongoing “Advertising 3.0” revolution? “Advertising 3.0” businesses should keep the following criteria in mind when building and scaling to best meet the demands of brands while also respecting consumer audiences: Assurance, Assessibility, Harmony and Adaptability.

Assurance - Brands want assurance that their advertisements are not being displayed by or associated with negative content. In “Advertising 2.0” this meant ensuring ads were not displayed near profane content such as drugs, nudity, etc. In “Advertising 3.0” this means ensuring brands can trust their campaigns are not associated with or undermined by the spread of fake news or hateful content. The current Facebook boycotts demonstrate mainstream brands are actively demanding their advertisements be disentangled from sites allowing the spread of harmful media content. The prevalence of fake news is substantially on the rise. 84% of brands fear the effects of adversarial fake news. The potentially deleterious effects on brands has the potential to be accelerated by automation, if algorithms are not structured properly to dampen placement by fake news. Fake news can cause consumers to accept false or negative associations with a brand but also prevent them from consuming or accepting associated information due to lack of trust, which mutes the effectiveness of advertising spend on product recall. In “Advertising 3.0”, assurance also means not automatically over-screening out advertisement placements, which can conversely have a negative revenue impact. For example, brand quality control keyword blacklists prevented brands who wanted to reach the Game of Thrones audience during the series finale from displaying ads in highly relevant inventory on the basis that the content was deemed as dangerous due to use of the words “Death”, “Sex”, etc. in articles. However, these words are bound to appear in most Game of Thrones content given the nature of the show. In this sense, assurance demands smarter and contextual advertising screening to reduce filter opportunity costs. Lastly, “Advertising 3.0” will bring a surge of vertical tools that provide assurance that ads are safe for a specific group, i.e. kid-safe advertising.

Assessability – Brands want campaigns to be easily assessable to measure, track and benchmark return on investment across advertising channels while respecting privacy and reaching real audiences. Online advertising has been so successful in part due to its ability to better attribute purchase intent than traditional media channels. In “Advertising 2.0”, digital advertising was able to improve assessibility with loose data standards and personally identifiable information. Moreover, usage of online platforms has continued to grow in spite of a large “bot” or fraudulent impression issues. Ad fraud in the current system costs advertisers billions of dollars per year. In “Advertising 3.0”, advertising tools will need to adapt to deliver the same or better ROI measurement and purchase attribution tools while adapting to new data constraints. The ongoing shift towards contextual advertising, segmenting based on content type, will play an important role here. In addition, technology giants and advertising platforms will seek out tools that help combat fraud to maintain brand legitimacy and trust in their platforms. Lastly, brands will seek out advertising channels where bot fraud does not exist and where they know they are reaching real eyeballs, i.e. gaming, in-store digital advertising.

Harmony – Brands demand the advertisement serving experience to be impactful and viewable but not disruptive to a consumer’s activities. 83% of people agree with the statement that “Not all ads are bad, but I want to filter out the obnoxious ones”. Consumers are open to advertising that exposes them to relevant products in non-disruptive ways. A majority would favor “Ad filters” instead of “Ad blockers”. However, brands also need advertisements to be viewable and highly visible to guarantee a better ROI. In “Advertising 2.0”, these two demands were at odds and technologies eventually heavily favored viewability often at a detriment to the user experience. In “Advertising 3.0”, with continued prevalence of ad blockers, advertising technology must be smarter about balancing viewability with non-disruption. As I discuss in the next section, certain emerging advertising ecosystems are better positioned to achieve this delicate balance in my opinion.

Adaptability - Brands seek to leverage platforms that are scalable both to their own demands and within the context of new innovations demanded by the industry at-large. Adaptability exhibits itself through limited financial costs to new integrations and flexibility of an underlying technology stack. For advertising ecosystems, this can manifest via horizontal adaptation, i.e. a video game advertising ecosystem adding the newest popular consumer game or vertical adaptation, adding new advertising functionality in-game for brands that want to double down on a particular game. “Advertising 3.0” emerging ecosystems are being developed in gaming, streaming / online TV and tech-enabled digital in-store. To reduce total cost of ownership of benchmarking and campaign placement tools, brands will seek increased interoperability between these new ecosystems and existing tools from the era of “Advertising 2.0”.

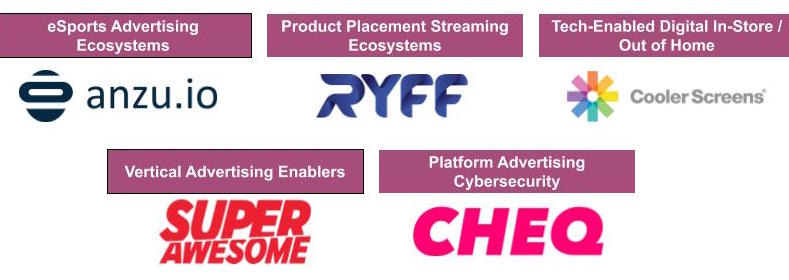

The “Advertising 3.0” innovation framework above will favor a new set of business models that should attract renewed VC interest in the AdTech sector. Below is a summary of AdTech areas that should benefit and an example of one company in each category.

eSports Advertising Ecosystems - platforms that allow for the programmatic insertion of digital advertisements into video games. Anzu is an in-game advertising exchange that connects brands with gamers by partnering with developers to seamlessly integrate advertising inventory into video games. In-game ads are highly viewable, many having the viewability of a real-world billboard but with better assessibility and tracking of impressions because it is digitally-based but without bot fraud. Gamers are intensely focused on game-play and value authenticity of brand engagement. Anzu partners with developers to blend immersive advertisements that are non-disruptive and match the feel of a game. A mixture of gamer profile information and contextual audience targeting also makes segmentation capabilities highly scalable across game titles.

I caught up with Itamar Benedy, CEO of Anzu, to get his take on how Anzu is helping to usher in the next phase of advertising technology: “Today, gaming is finally being seen as a mainstream channel, right alongside TV, OOH, and other forms of digital advertising. Anzu’s cutting-edge solution offers new, authentic, and completely immersive ways for brands to reach their potential customers using programmatic technology. With the acceleration of gaming during and beyond COVID-19, we’re leading the way in the development of new AdTech industry standards that don’t compromise. I’m talking about the absolute highest levels of brand safety, data privacy, and ad viewability, all combined with the power of precise targeting. Add to this the ability to measure campaign effectiveness, and you’ll see how the advertising 3.0 ecosystem is taking shape!”

Product Placement Streaming Ecosystems - with the large COVID-19 related growth in video streaming also comes significant competition amongst both subscription video on demand players (Netflix, Hulu, Disney+) and advertising video on demand players (Tubi, Pluto, Crackle, Xumo) all competing for online TV viewership attention. The heightened competition will encourage companies to look for new ways to diversify revenue streams. At the same time, upholding a monetization strategy that is least disruptive to the viewing experience will remain key in maintaining a highly engaged audience. Dynamic product placements into online TV content offers a potentially lucrative incremental revenue stream with visible advertisements that are minimally disruptive to the user experience. In addition, contextual content targeting, streamer profile information and streaming geo-location can be informative in helping better segment and target streamers. More saliently, analytics on preferred content can be extremely formative in understanding consumer preferences, which is part of how Netflix distinguished itself with its predictive analytics capabilities. Ryff uses artificial intelligence to dynamically insert product placements into content streams. By partnering with content creator sources, who then place this content across many streaming platforms, it can ensure better scalability of its technology stack.

I chatted with Roy Taylor, CEO of Ryff, to hear his perspective about the role product placement technologies, like Ryff, will play in transforming advertising: “ Ryff is a part of a new breed of Hollywood player, rewriting the rules of product placement using our proprietary AI technology. We virtually insert viewable, but non-disruptive products into fully mastered and edited content leveraging contextual content targeting to reach the right consumer. Welcome to Advertising 3.0 and the future of brand integration.”

Tech-Enabled Digital In-Store / Out of Home - Digital out of home (DOOH), site-based digital billboards and screens, is a highly visible advertising medium. Traditional (non-digital) OOH has historically struggled with assessibility and measurability. Because DOOH is digitally-enabled, but not fully online, it does not struggle with the same assurance / fake news / bot issues of digital advertising but captures some of its assessibility benefits. While ROI and lift have historically been tougher to measure for OOH, all views are real impressions and there is no bot problem. In-Store digital media provides better attribution and lift measurement given the impression is served at the point of sale. In addition, advances in facial recognition technology and geofencing have helped to better quantify lift. Moreover, post-coronavirus, because of capacity constraints imposed by social distancing, there could be a greater adoption of sensor technologies that track people count and audience proximity to screens. For example, VergeSense recently raised capital for its office people counting technology. Increased sensor prevalence for public health reasons, could have a spillover benefit to digital out of home if operators can partner to also leverage these new sensor installations. Cooler Screens installs screen displays on freezer and refrigerator aisle doors in grocery stores. Coming out of coronavirus, vertical DOOH operators in the grocery, pharmacy, QSR and C-Store sectors are better positioned as they provide more essential goods and their units have seen less severe traffic declines. Cooler Screens’ product makes the freezer aisle itself more “viewable” by displaying relevant product information and also displays highly viewable ads augmented by segmentation aided by sensor technology. Moreover, in-store DOOH businesses, like Cooler Screens, are highly assessible and measurable when data is cross-referenced with point-of-sale data at the store-level. These businesses can require more hardware investment to scale, but improved assessibility and viewability should justify the return on investment for top players.

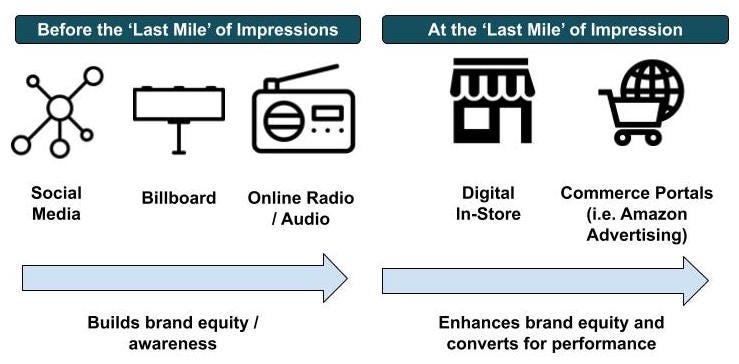

I chatted with Arsen Avakian, Co-Founder and CEO of Cooler Screens to learn more about his view on the critical pillars of “Advertising 3.0” and how they will benefit in-store media. First, he believes that “in ‘advertising 3.0’, CMOs will need to provide performance and that brands will prioritize channels that bring the building of brand equity and performance together.” For example, Amazon’s nascent advertising business builds on “Advertising 2.0” online advertising by providing attribution by tying advertisements to Amazon cart data, thereby melding brand equity and performance. This newer segment of Amazon’s business recorded $4+ billion of revenue in Q4 2019 and grew 40%. Second, Arsen believes “advertisers must reach real eyeballs by winning the hearts and minds of customers to earn the right to advertise.” People should be more receptive to advertisements if they associate the technology infrastructure with a non-advertising benefit to them. Cooler Screens earns this right by providing easily readable product information on the freezer / refrigerator case. Similarly, Ryff and Anzu earn this right through non-disruption by integrating their advertisements seamlessly into gaming or streaming content. Their advertisements are deeply integrated with the content and are thereby viewed less as a marketing attempt while still advertising effectively. Third, he believes it will be important for brands to “understand campaigns from a full customer journey perspective. Much of “Advertising 2.0” is missing the ‘last mile’ impression at the store, which is delivered at the moment of greatest potential impact to sway a purchase.” Advertisements prior to the last mile still build brand equity, but the last impression as a consumer is already in the mood to shop, has the higher probability of converting positive brand associations to new sales dollars:

Vertical Advertising Enablers - in “Advertising 2.0”, Facebook and Google have had a horizontal strategy of attacking the advertising ecosystem, attracting audiences of many ages and demographics to target. However, there are specific community niches and use cases that require additional attention and nuanced resource allocation to adhere to regulations and tailor offerings to a specific use case. One of those use cases is advertising targeted at children, for which there are many nuances of a safe and effective advertising strategy including enhanced regulation and data constraints related to the use of personally identifiable information (PII). SuperAwesome is a leading provider of technology tools that enable kid brands to safely engage with child audiences globally. Vertical advertising tools, like kidtech, will benefit from increased data regulations over the coming years, able to provide assurances of kid safe content and assess advertising impact through legally-compliant targeting and measuring. SuperAwesome offers tools beyond advertising including a kid-safe social engagement platform and parental consent infrastructure for app developers. These additional tools advantage SuperAwesome by enabling it to offer a full KidTech platform. Moreover, SuperAwesome wins the hearts and minds of parents and earns the right to place children’s advertisements by making the internet safer for children with their portfolio of other media and consent tools.

Interestingly, SuperAwesome views kid advertising as just the first part of the advertising ecosystem to require zero PII usage, but that regulation should create change in other areas of advertising over the medium to long term. I touched base with Dylan Collins, CEO of SuperAwesome, to hear his perspective on this industry trend and the critical role SuperAwesome is playing in kidtech innovation: “The kids digital space is unique in being shaped by laws which mandate zero PII engagement. Not only are these increasing in geographic scope (from the US to Europe to Asia), they are also increasing their coverage (EU kids privacy laws now define a child as under 16, versus 13 in the US). We're effectively seeing a government-driven undermining of the PII-based advertising model, starting with the under-16 cohort. Even today, the kids ad space is the biggest privacy-based media sector in the world with a TAM of $4b and growing. Ultimately the internet was never designed for kids (and their privacy laws) so this really heralds a huge displacement in the underlying delivery technology required at scale for the entire ad ecosystem.”

Platform Advertising Cybersecurity - technology tools that address the aforementioned issues with digital advertising, including click / impression fraud, brand quality control, fake news associations and bot prevalence. The long-term winners in this sector must offer “platform cybersecurity” capabilities rather than point solutions. Platform functionality is key in order to integrate solutions to the many security and quality issues that plague advertising tools and campaigns. Platform channel breadth is also important, addressing campaign issues across digital, DOOH, gaming, TV and other emerging channels to reduce total cost of ownership to subscribers. CHEQ is a leading digital media cybersecurity platform with products that address viewability, ad fraud and brand safety issues across video, paid search, social media and gaming (via a partnership with Anzu).

I spoke with Daniel Avital, Chief Strategy Officer of CHEQ, to learn more about the role cybersecurity media businesses will play in boosting the entire AdTech ecosystem: "The fact that cybersecurity companies like CHEQ are stepping in where AdTech has seemingly failed, is probably good news for the industry and will drive technological players in advertising to step up their game. There's a reason why AdTech, for a while now, has failed to attract big VC dollars and maybe this will give the industry the push it needs."

Coronavirus is accelerating shifts in audience attention that will accelerate the emergence of new advertising ecosystems and spur experimentation and then adoption with new AdTech tools. After the crisis, a rebound in advertising wallet allocations will make brands consider new channels and innovations that enhance the security and measurability of existing channels. “Advertising 3.0” should attract more venture capital to the AdTech sector to back new innovations just at the time brands will be most open to trying new strategies to enhance their marketing campaign efforts.

All Innovation Armory publications represent expressly my individual views and the views of those interviewed and do not represent the views of companies with which I have previously been associated or with which am soon to be associated. These publications are my personal opinions and are not meant to be relied upon as a basis for investment decisions.