The European Hero Spreading Inclusive Salary Infrastructure to New Terrains

The European Hero Spreading Inclusive Salary Infrastructure to New Terrains

How Kadmos is Bringing Seamless Cross-Border Payments to the Global Migratory Workforce

Welcome back to The Innovation Armory! Today’s piece explores the global financial infrastructure that serves the global migratory workforce, a population of 169+ million people. Specifically, I dive deep into how new age salary disbursement and management technologies are ushering in a new age of financial inclusion for one of the world’s most critical workforces. Thank you to Sasha Makarovych (Co-Founder of Kadmos) for sharing your perspective for this piece. Read on for more about:

The under-the-radar market opportunity in serving global migratory workers

Why the global migratory workforce will continue to grow in size

How inefficient the migratory financial tech stack is today

How Kadmos is bringing greater transparency and efficiency to marine and construction employers and workers

How to craft a B2BC go-to-market approach that optimizes your network effects, embedded growth opportunities and potential operating leverage

The cross-border embedded wage access opportunity

This is a long post so if your email gets clipped at the bottom, make sure to click unclip / visit The Innovation Armory to check out the full read.

If you liked this piece feel free to subscribe for future updates below:

Or share with your friends :)

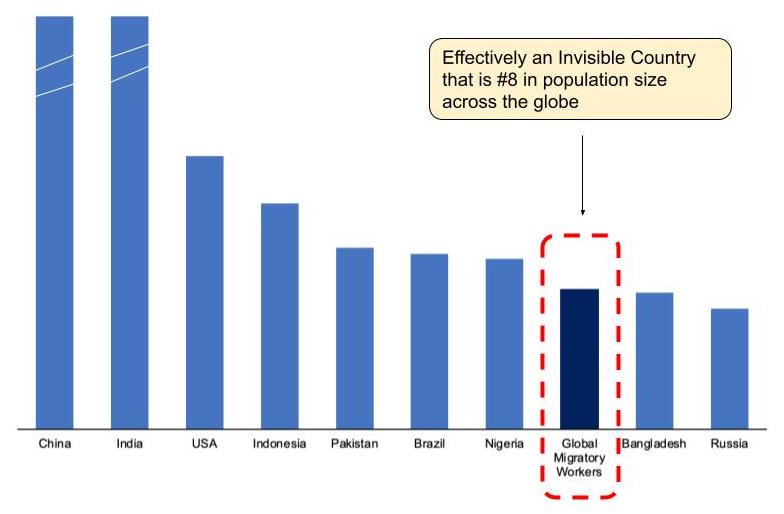

The global migrant workforce population has outgrown world population growth in recent years. Migratory workers now represent nearly ~5% of the world’s total labor population, up from 3.8% nearly a decade ago. Migratory workers generally perform blue collar and unskilled labor work by systematically moving between countries to perform project-based jobs, often on a seasonal basis. With the explosion in global and emerging market fintech over the last bull cycle, the tech community has seen countless players vying to become the neobanks and payment rails of their respective countries and regions. Migratory workers have historically been underserved both to their own detriment and to the financial detriment of their employers by virtue of constantly working in and experiencing the world across multiple regions. The global migrant worker population generally performs absolutely critical roles in their destination countries including in key industries like marine shipping, construction, healthcare, agriculture and manufacturing services. This population is fairly disenfranchised by the global political system by virtue of limited domestic oversight combined with an unwillingness of the international community to step up to enforce multilateral norms to their benefit. These workers build foundational infrastructure and are economically dependent on projects in destination countries but can’t ever vote and are often unfortunately treated as disposable, second class citizens. With a total population of 169+ million per ILO estimates, the migratory worker population would independently be a top 10 country in terms of population addressable market if you were to stack it side-by-side with today’s most populous nation-states.

I’m not actually suggesting this population would ever become a sovereign territory – just that they are large and important enough to merit being treated as a key interest group in international decision making. However, this population isn’t sufficiently protected by global bodies like the UN and also have even been de-prioritized from an innovation perspective since their distributed presence and lower purchasing power make them appear tougher to service. Let’s say this interest group were theoretically represented at the UN:

While the pace of global migrant worker growth has already accelerated, I believe we have reason to believe it will grow further from impending refugee crises, the evident shortage of unskilled labor in developed markets through the pandemic and increasing globalization and urbanization.

Particularly in certain sectors like marine shipping and construction, the migrant worker population is a sleeper market for selling fintech products with a B2B distribution strategy. At face value, it would appear as though this market has relatively low purchasing power as migrant worker consumers often perform unskilled blue collar jobs. That may be true, but there is meaningful upmarket inefficiency in the migrant salary system from FX middlemen, payment fees, payment delays and cumbersome back office work that enables a player like Kadmos to come in and offer an end-to-end solution that creates massive consumer and business value even for a lower purchasing power demographic.

Kadmos: Pioneering Financial Inclusion for Migrant Workers

Kádmos / Cadmus was one of the first Greek heroes in the historical record who helped found Thebes. Legend says he is the Hero that brought the first alphabetic writing to the Greeks, which formed the basis of Western language and civilization. Just like Kádmos the Greek hero helped lay the foundation for Western civilization, Kadmos the German fintech is laying the foundation that will usher in financial inclusion for the “invisible” migratory worker population across the world.

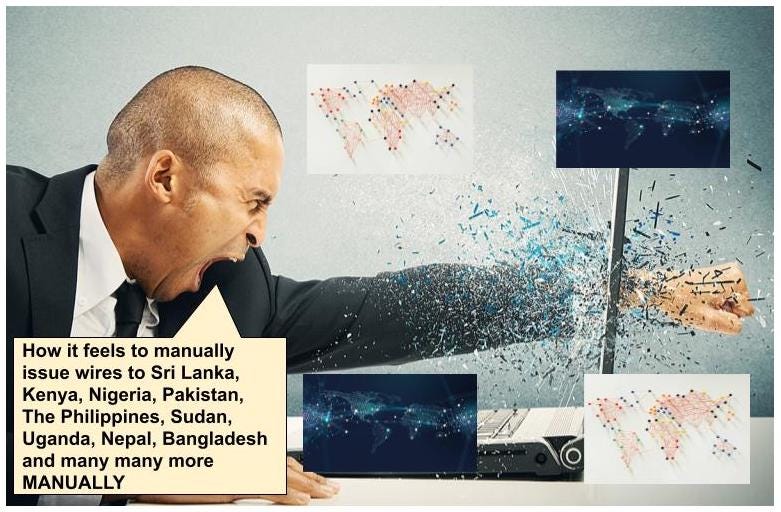

Migratory workers and employers both suffer from costly inefficiencies in the financial supply chain that eat into earnings. Since migratory workers are often working blue collar jobs, they have little excess to give in the first place and their wages are often eaten into by: i) FX inefficiencies (sometimes multiple conversions through intermediaries are required since they aren’t paid out in their desired currency), ii) high transaction fees (potentially as high as $50+ USD per transfer) and iii) regular payment delays. Employers of migratory labor are by definition global organizations and they have a massive backend workload to handle routing of payments to basically every geography imaginable and bear most of the cost of high transfer fees for sending SWIFT payments manually to those territories. Managing the global payment complexity is a huge back-office strain on global employers operating in sectors with already razor thin margins like marine shipping and construction.

The disconnect that exists today between the disbursement and receipt of payments for migratory workers is what is largely responsible for these inefficiencies both on the employee and employer side. Kadmos helps close the loop between salary payments from employers and management by global blue collar workers by offering an end-to-end dual-sided e-wallet system that helps employers manage all payments through a centralized, automated platform and for employees to quickly designate their disbursement currencies and payment destinations with full transparency without the use of costly intermediaries. There are of course B2C remittance solutions that seafarers and construction workers can use to remit earnings to a country of choice, but selling into the business / corporate allows Kadmos to capture the benefits of B2C cross-border fintech solutions while realizing additional upstream fee and FX efficiencies and the benefit of a streamlined, end-to-end user experience.

I caught up with Sasha Makarovych, Co-Founder of Kadmos, to learn more about how Kadmos is driving more financial inclusion within the migratory worker population:

“Even with all the new financial technologies being developed these days, we saw that a certain segment of workers was missing out. In industries that employ workers from around the world, such as shipping and construction, we saw first-hand the difficulties they faced in getting paid on time and sending money home. Existing payment processes were inefficient, non-transparent, and put extreme burdens on both businesses and workers. Moreover, migrant workers lacked a secure and cost-effective way to send money home to their families. In response, we devised a solution that gives these workers more control over their finances and helps them keep more of their hard-earned money. Our solution benefits workers as well as the companies that pay them by streamlining processes and increasing transparency. It really is a win-win situation for everyone.”

B2B2C Model Affords Unique Go-to-Market Advantage

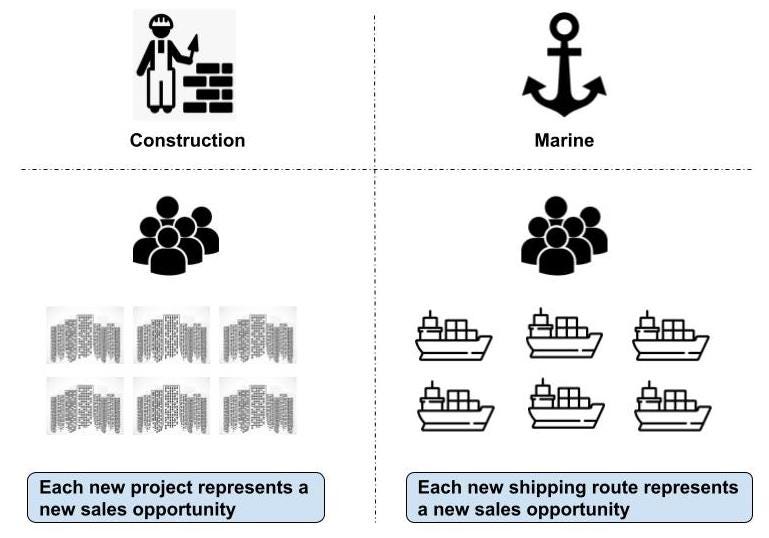

In Waking the Sleeping Giant in the Global Financial System, I discussed the competitive advantage that Kwara would have in selling banking services in emerging markets by leveraging existing SACCOs and credit unions to acquire users at a low customer acquisition cost. Kadmos’ model affords it a similar advantage. Kadmos is initially targeting the marine shipping and construction industries and is partnering with corporates to give them access to automated payout management and centralized compliance in exchange for the opportunity to market its wallet and financial products to end user migratory construction workers and seafarers. This population is traveling regularly and generally underbanked and so otherwise would be fairly tough to access and distribute to through more traditional marketing methods. This B2B2C approach gives Kadmos go-to-market superpowers, namely three primary advantages servicing the migratory community: i) Embedded growth opportunity on blue collar projects, ii) Operating Leverage on Customer Acquisition and iii) Greater Network Effects for New Sales Due to Temporary Nature of Migratory Work.

Regional / global construction contractors and seafarers have multiple projects and shipping routes they operate simultaneously. As these business clients’ core businesses grow organically, there is also an embedded growth opportunity for Kadmos to sell more software. For example, as a contractor wins a new mega project in a different city, that project will likely have different workers but it will prefer to use the same solution from an organizational efficiency and data management perspective. This creates a one-to-many growth model where each corporate win includes meaningful future upsell assuming that customer is itself growing naturally.

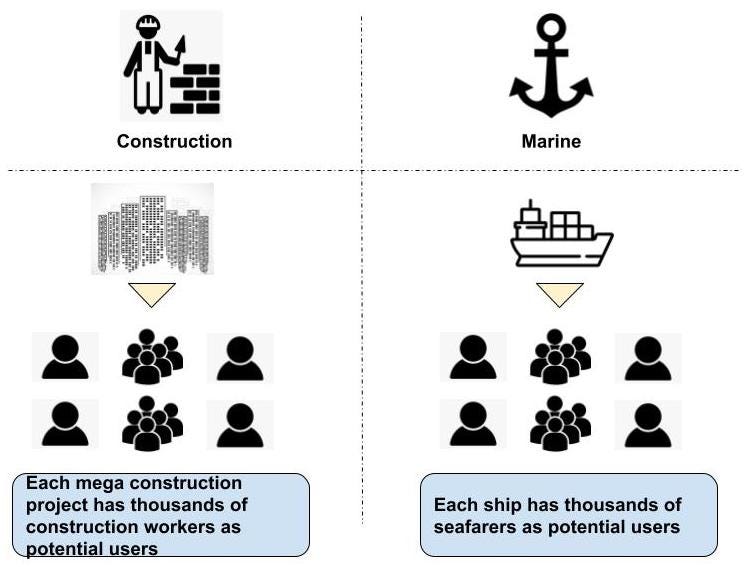

Similar to Kwara where acquiring one SACCO meant accessing all of its end users, acquiring one contractor or shipping corporate means accessing thousands of end user workers. This provides meaningful operating leverage on customer acquisition costs as the CAC from one corporate is spread across an army of potential end user migratory workers on jobsites and ships.

Given this migratory blue collar work is seasonal and temporary, workers move between global and regional employers quite frequently. The frequency of job change / transfer means that Kadmos will likely benefit from supercharged word of mouth marketing at the consumer / end user level since workers will bring their experience with the product forward to their new organization (and will have a financial incentive to try to continue using the same platform going forward).

Operating leverage, embedded growth and network effects walk into a bar. I know you’re wondering, this is an odd joke, what’s the punchline here? It’s not a joke, they win the market.

This B2BC closed-loop salary model has the opportunity to also cannibalize and disintermediate transaction volumes over time from B2C cross-border payment remittance players like TransferWise and Remitly. Remitting through the B2BC employer-linked wallet will win out on convenience, seamlessness of the user experience and can offer superior economics if employers pass some savings onto workers in the form of higher net disbursements.

Doubling Down on Each Ecosystem Stakeholder

By building out the financial rails that seamlessly connect employers and migratory workers, Kadmos is in an interesting position to leverage that relationship to double down on each stakeholder to create additional value. On the employer front, workforce management is a logical expansion area since by virtue of paying out all centralized salaries, Kadmos will also need to have a dynamic roster of employees on specific projects. Adding time tracking and workplace compliance modules that directly integrate with the salary disbursement could create additional cost and time efficiencies for the back office and also help spur labor productivity improvements. Even once specific migratory workers leave a given employer, Kadmos will still have a registry of their work history (potentially also an active wallet for that employee). It can leverage this data to try to act as a matchmaker between temporary / seasonal workers and corporate clients. This could be utilized both for existing corporate clients to deliver additional value (perhaps even charging a headhunting fee) or more interestingly, could be leveraged as a sales tool to accelerate sales processes with new corporations. This matching is mutually beneficial for the user and corporate by driving towards employment faster and has an incredibly low marginal cost. This could create a carrot to push along sales processes by enticing corporations with batch leads of workers ready to fill vacancies in key projects.

The existing salary advance players that exist often don’t have multi-currency payout and aren’t built to service a global workforce. For example, Wagestream (UK/US), Payflow (Spain), Earnipay (Nigeria) and Refyne (India) all focus on particular geographies and also don’t support multi-currency cashout / remittance. A wage advance in a different currency that you end up losing value on due to FX inefficiencies is less valuable than one done seamlessly through an end-to-end salary management system that can offer both competitive interest and FX rates through one singular platform. Moreover, since migratory workers change jobs seasonally and frequently, there is often friction when they arrive at a new destination to find housing, essential goods and also struggle to access relevant integration services given language barriers and lack of familiarity with the region. Kadmos could let relevant relocation services and essential goods providers integrate with the end user wallet to offer deals to workers on critical needs and also generate leads for local service providers who can begin to tap into surges in temporary demand from seasonal workers more effectively.

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.