The Manifesto of Social Commerce: It’s For Real This Time

The Inspiration, Opportunity, Enablers and Endgame: How Creators Will Ultimately Win Big in the New Distributed Commerce Landscape

This week’s piece for The Innovation Armory is a deep dive into the future of distributed creator-focused social commerce. I cover a variety of topics including how Western social commerce will co-opt the benefits of experiential brick & mortar retail and what Western retail can learn from leading Chinese technology companies paving the way in social commerce. Social commerce 2.0 in the west will build on themes of gamification, group buying, live video and personalized discovery with a further emphasis on distributed creator-focused selling that will help power the burgeoning passion economy. I conclude by discussing which companies are best positioned to capture the most value from this transition to distributed creator-focused social commerce. Thank you to Manohar Charan (CFO of ShareChat), Maryam Ghahremani (CEO of Bambuser), Louis Chen (CSO at Perfect) and Zach Oschin (CEO of Elenas) for sharing your perspectives for this piece. This is a long post so if your email gets clipped at the bottom make sure to click unclip / visit The Innovation Armory to check out the full read.

My next piece will be about how the rise of digitally-native professional academies are helping future proof education by integrating job-tailored training with employment marketplaces. Thanks in advance to Shaan Hathiramani (CEO of Flockjay) for sharing his thoughts for the piece.

If you liked this piece, you can subscribe to future Innovation Armory updates below:

Western Social Commerce Will Co-Opt The Benefits of Pre-Pandemic Experiential Retail

E-Commerce in the Western world is built primarily on a transactional and functional model that under-monetizes the potential to merge shopping with experiential entertainment. Amazon revolutionized the e-commerce landscape by building out backend logistics infrastructure, recommendation algorithms and a best-in-class user interface to rapidly decrease frictions to shopping. The result was to save customers money, time and frustration compared with the average in-store retail experience. Shopify helped to democratize comparable digital and logistics infrastructure, but for independent retailers. The result was to distribute commerce to empower smaller retailer businesses. In response, pre-pandemic, many traditional brick & mortar retailers doubled down on the in-store experience to differentiate. I’ve selected a couple of examples of in-store experiences below that I think are particularly creative:

The belief was that this pivot to experiential shopping offered numerous benefits to traditional brick & mortar retailers:

Drove greater traffic to stores for experiences which would spill over to higher volume of in-store product purchases

Enhanced a retailer’s brand and spurred viral word of mouth marketing hype

Converted more in-store purchases through digitally enhanced discovery / try-on and premium services by store associates to recommend / curate products

Created a willingness to pay a premium for goods associated with an entertaining and luxurious / VIP in-store experience

Drive meaningful social experiences around their brands and products

While these benefits did bear results for numerous traditional retail brands, it is interesting to note that most of these high-end experiential concepts exist primarily in tier 1 cities like NYC / Tokyo where both the real estate and service costs to pull off these concepts are high and the scope of impact is inherently geographically limited. Not to mention, now fewer consumers are willing to attend these retail experiences in person due to COVID-19. The last wave of Western e-commerce beat out brick & mortar on convenience, time and price. The next generation of social e-commerce will co-opt the traffic, engagement, brand and social benefits of experiential retail with the zero / minimal marginal cost unit economics of the internet to deliver unique, creative and memorable consumer experiences alongside shopping:

Look East for a Taste of the Future

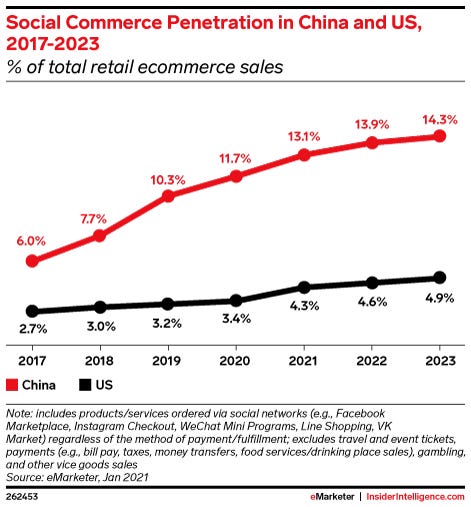

Across Asia, particularly in China, the initial wave of entertainment and creator focused social commerce has been a smashing success. The unique blend of technological and process innovations in China have yielded a much higher penetration rate of social commerce in China relative to the US e-commerce market:

The Chinese innovation spectrum in social commerce largely melds features of lifestyle commerce, gamified commerce, team buying and live video commerce:

Within lifestyle commerce, the lack of traditional advertising in Xiaohongshu’s content model fosters substantially more trust than Facebook, Twitter or Snapchat could garner with product reviews and recommendations. Further, its content model also leverages a healthier balance of Key Opinion Consumers (KOCs), normal consumers who attract a following as tastemakers in a specific category, vs. Key Opinion leaders (KOLs), celebrities who have the power to promote products but come off as less authentic. Consumers form meaningful micro-communities spearheaded by KOCs and this trust-based content drives more sustainable lifestyle / value driven purchase online. Within gamified commerce, Duo Duo Orchard is one of Pinduoduo’s most popular games. Users own a tree for which they need to earn water and fertilizer to grow. They can earn these items by taking actions that are desirable for Pinduoduo growth like making a purchase, achieving daily check-in streaks, inviting friends or visiting a specific brand’s marketplaces.

All of these elements of Chinese social commerce also have two further areas in common: First, these features are displayed in a mobile first / native format as smartphones leapfrogged PC usage in many areas of China. Second, unlike Western e-commerce which is largely key-word focused, these players focus on mobile discovery through picture and video feeds that recommend products to users.

Expanding the Horizon of Gamified Commerce

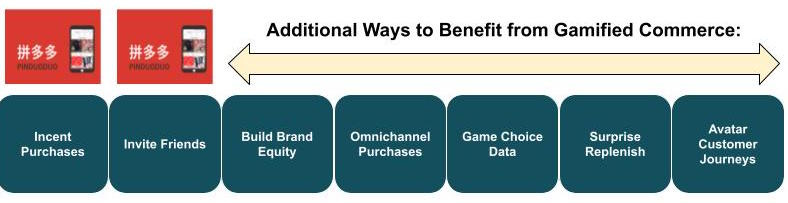

Duo Duo Orchard primarily leverages games to incent purchase and expand the network of PDD users. However, there are numerous untapped ways for creators, brands and retailers to further leverage gaming to supercharge commerce experiences. Below are just a couple of examples:

Build Brand Equity - Suppliers can create virtual skins for games to build a particular brand association for a new product launch. For example, Nike created a short form game where users could wear a digitally animated form of a new shoe release on a personalized avatar and navigate an obstacle course where their player bounced on clouds. This game reinforced the association that Nike shoes make you “fly” figuratively and are durable. Further, these gamified experiences can be further enhanced by allowing users to snip a portion to share on social media, thereby driving more traffic to the site and supercharging word of mouth marketing.

Omnichannel Purchases - geo-location / map based games can help incent customers to make offline purchases specifically vs. an e-commerce based purchase. Applying this framework to Duo Duo Orchard, for example: checking into a specific nearby brick & mortar store could automatically level up a user’s tree.

Game Choice Data - as users play games, they are making choices about where, how and when to move their characters / avatars. These games can be intentionally structured in ways that provide valuable data that can serve two different purposes for each of supply and demand. For example, on the demand side, if a player repeatedly chooses to pick up products that are red, it can inform the discovery algorithms to display more products with their red color setting to increase click through rates for that specific consumer. On the supplier side, at scale, these games can aggregate in-game choices to inform optimal manufacturing volumes for smaller retailers.

Surprise Replenish - Pinduoduo generally gives a digital reward for real world actions taken on its platform. I do expect this reward scheme to become even more popular as the spread of non-fungible token (NFT) protocols make it easier to add a scarcity element to digital assets. However, instead of rewarding with digital assets, platforms could reward users for playing / inviting friends to company branded games with free physical goods, like replenishing a consumer staple like tissues or soap.

Avatar Customer Journeys - Platforms could enable customers to actually shop within the games in avatar form. Users could chat, interact and hang with one another as avatars and shop in animated stores that eventually redirect to a socially-enhanced supplier / retailer commerce portal. More on this avatar-based commerce interface later.

Emerging Live Video Commerce Infrastructure

Although just one piece of the social commerce puzzle, live video commerce is already starting to grow in prevalence in the West. The potential here is massive with China’s current market already estimated at $60 billion and growing rapidly in its nascent stage. To learn more about these implementations with Western retailers and nuances vs. the Chinese model, I caught up with Maryam Ghahremani, CEO of Bambuser, a Sweden-based developer of infrastructure that enables retailers to offer their own native shoppable, live broadcasts

My Conversation with Maryam Ghahremani (CEO of Bambuser)

SN: Could you talk about Bambuser’s differentiation to the retailer in enabling live video shopping?

MG: Since its beginning, e-commerce content has been dominated by pictures and text. If you look at markets like China and the rest of Asia, however, video and more specifically, live video has taken on a much bigger role, and we at Bambuser believe it will power the future of commerce. As video shopping grows in popularity, there’s an increasing number of platforms and channels a retailer can take to implement it. For retailers who focus tremendous amounts of time, energy and budget cultivating their brand identity, Bambuser is a favorite, because, unlike centralized social commerce shopping applications, we enable brands to retain control and ownership of the customer relationship while receiving the benefit of data-based insights. Another important differentiator is the experience Bambuser offers. Our technology is very plug and play and incredibly easy to use. We integrate seamlessly with brands’ e-commerce software, which allows us to instantly present accurate product and pricing information within the livestream. Because retailers don’t need to build anything, they can launch their first show quickly. Normally, we go live within 2-3 working days from the time we sign the initial contract. Even though some of these retailers have in-house R&D, technology innovation is not their core capability. Bambuser, however, was one of the first companies outside of Asia to launch live video shopping. We now work with a variety of partners across multiple verticals, from large enterprise companies to SMEs.

SN: You’ve intentionally structured the business so that the retailers control their own social commerce experience. Do you envision there being a platform where most social commerce concentrates in the West or do you view it being distributed across retailers to power their own independent social experiences?

MG: It’s hard to know because everything is so new. We will definitely have a better understanding of shoppers’ behaviors and preferences as adoption continues climbing in the West. That said, based on my experience, I think we are going to see a much more fragmented market than we currently see in China. In China, 90%+ of live shopping is going through T-Mall or Alibaba. In the West, there isn’t a single, dominant social media player, and I don’t see any platform in the West taking this role on because the landscape is so much more fragmented. Many social platforms today aren’t even monetizing commerce at all. Our vision is to be platform agnostic, but when you click the buy button, you will be redirected to the actual site of the brand so they can own the experience. This is particularly important to preserve economics for independent retailers and creators in the distributed commerce world. When you are doing a livestream, you want it distributed across as many viewers as possible between platforms, but you want that traffic to redirect to your own commerce portal as an endpoint. Therefore, our strategy is to have open APIs and integrate with as many of the social networks as possible, so we can first attract the audiences where they are on the retailer’s behalf and then deliver them to the retailer.

SN: Could you talk about some of the nuances in use cases you have observed between live-streaming in Asia vs. the West for the limited Western use cases to-date?

MG: In the West, the content is very different. Live-streaming is about entertainment, customer service, getting closer to the end consumer, increasing engagement and education. In Asia, it is much more about coupons, discounted pricing and bulk / volume sales. In the West, we, of course, see discounts and special offers, but they’re not as core to why consumers choose live-streaming as their preferred mode of commerce.

Li Jin (Founder of Atelier Ventures) who coined the term “Passion Economy”, has discussed how the passion economy will lead to the “enterprization of the consumer” , a phenomenon where individual creators and producers will increasingly “want to grow into businesses in their own right”. Distributed creator-focused social commerce will inevitably blend product sales with individual creators’ media along with that of traditional retail brands. Both traditional companies and independent, single unit creators will look to monetize their brands, grow audiences, optimize engagement and drive profit through commerce. Neither traditional retail brands nor creators necessarily have strong engineering / development talent or resources. Therefore, it is important that these backend tools that enable social commerce are easy to implement with limited to no code required. These no code tools will democratize live-streaming, and more broadly, the full stack of commerce tools as creators seek to fully own their own brands and associated social commerce experiences.

The Socialized Customer Journey

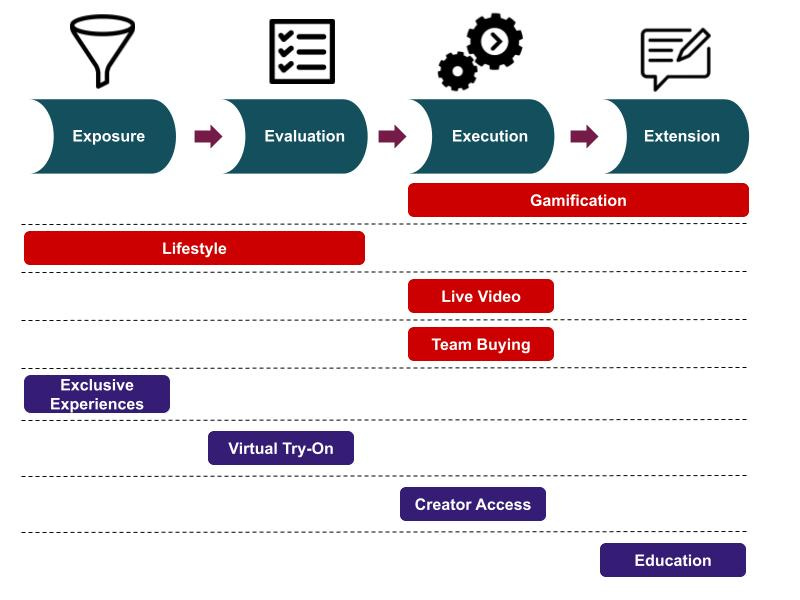

The social customer path can be broken down into four primary phases (4 Es): product exposure, evaluation, execution and extension. The primary platforms of Chinese social commerce span the full customer journey and each differentiates on primarily 1-2 vectors. However, there is further opportunity to optimize commerce experiences to double down on each of these key decision points in the customer journey. Select examples include exclusive experiences, virtual try-on, creator access and education:

Exposure - Much of the existing strategy in the exposure phase has been in two primary areas: algorithmic personalization and content discovery. Xiaohongshu’s lifestyle commerce platform innovated in both of these areas. There is further opportunity to leverage exclusive digital experiences to drive further traffic and seed product exposure through those experiences. The Hermès Carré Club and other pop ups leverage art installations to drive in-store retail traffic. As rare digital art becomes more popular, platforms could attract traffic with a one-time, rare digital art installation (See: Hashmask’s sale of $10M of digital art to get a sense for the growing demand here). Separately, VIP virtual concerts (from real artists or VTuber avatars) could spur site traffic and even be audio-only to encourage shopping while listening.

Evaluation - there is a large opportunity to build digital infrastructure that enables try-on / virtual testing of products to provide consumers more comfort with a decision before executing a purchase. One category that would particularly benefit from these try-on technologies is the beauty space. To learn more about the progress and potential within the virtual try-on category, I caught up with Louis Chen, SVP and Chief Strategy Officer, at Perfect Corp, a developer of AR-based virtual makeup try-on software:

My Conversation with Louis Chen (SVP and CSO at Perfect Corp)

SN: What is Perfect’s mission and could you describe your product set for The Innovation Armory audience?

LC: We have two main lines of business: B2B and B2C beauty technology tools. For B2C, we developed YouCam Perfect, a selfie camera app, and YouCam makeup, an augmented reality virtual makeup app. The latter is focused on augmented reality filters. The larger portion of our business is in B2B. We offer 16-17 different software services to beauty brands and beauty retailers while also exploring other categories such as jewelry and accessories. We help these beauty brands facilitate a digital transformation. For example, if they want to offer augmented reality on their website or for in-store makeup counters, they can license our technology. We built the cloud platform so that brands can digitize their makeup assets effectively to create the right shades, textures, palettes, foundation (up to all 8 core categories of cosmetic products). Once they put the assets on our cloud, they can push these assets through different channels: WeChat or through our recent partnerships with YouTube or Snapchat to name a few. We have 300-400 beauty brands using our technology currently.

Below is a sample of the technology in action, recommending products based on a woman’s facial complexion, moisture, texture, etc. and then overlaying the product with AI-powered augmented reality in real-time.

SN: What has been the impact of COVID-19 on the beauty industry? As compared to other sectors in retail / consumer, how prepared were beauty brands to adapt?

LC: Some brands have been better prepared, others less prepared but no beauty brands were truly ready.. It is important to sub-divide the pandemic reactions into sub-categories like makeup, skin care, hair, etc. The traditional cosmetic segment has been impacted because people are doing fewer social activities as they go out less and therefore use less makeup. However, their skin care categories have been increasing significantly. Skin care takes longer than makeup to apply and since people have had more time at home, they have more time to take care of their skin. Also, because of the lockdown, people see their skin more often on their face through video-conferencing. This is part of the psychology driving sales. You see yourself more often and feel compelled to use more skin care products. On the shift from physical to digital, before the pandemic, for North America, only 10% was happening online for beauty. That has tremendously shifted where big brands are reporting 30-40%+ of sales occurring online. This is where we come into the picture. For makeup products, consumers care about styling for new products. We have helped expand digital sales from replenishment into the actual purchase of new products. Physically, when users went into the store, they tried 2-3 colors of lipsticks. With augmented reality, we see users trying 12-13 different shades. The technology looks so good that 99% of users would not be able to tell the difference between applying virtual vs. real lipstick. Same with skin care: in the past they have had beauty advisors (BAs) who advise the consumer on products for their skin. That can be augmented now through artificial intelligence and BAs can also interact with consumers through tele-appointments. Beauty brands know the future is digital and that is why they are investing a lot.

SN: On the B2B side, what do you view as the main benefit of these cosmetic experience technologies for brands? Is it expansion of the user base, higher conversions, reduction of return rates?

LC: First, some brands want to raise awareness when they launch new products as they use these tools for marketing. With regards to younger consumers, some of these brands knew their engagement had been declining through traditional advertising channels. Our tools give them better access to a younger audience with socially linked products. Sometimes you get more social value out of it because if the consumer is taking a selfie, she will likely be sharing back to Instagram or another social network. Second, these brands tend to have little access to who their consumer is when they sell through indirect channels as opposed to D2C. When they use these technologies to drive D2C sales and as consumers spend more time on their website, they get a better idea of average customer profiles. Third, shopping is no longer about going through boring online catalogues. It is about shoppertainment and actually entertaining these consumers to increase conversion rates. Fourth, there is an old expression, the “more you try the more you buy” and we have seen that in uplift rates for clients as consumers try on more makeup products. This drives more impulse buying where a consumer didn’t expect to buy as much lipstick but buys more because they tried more on. Fifth, for return rates, we are seeing reductions of 5-10%. Consumers have a better sense of what the shade will look like on their skin, which means they are less likely to return.

SN: Could you talk about your partnerships with social networks and how you think about the opportunity within social shopping experience and the importance of overlaying experience management tools to drive social engagement and sales through social channels for these brands?

LC: We do think social commerce is going to take over the world eventually. If you go to China or Southeast Asia, livestreaming shopping and other social commerce experiences are more prevalent. We work with Google, Snapchat and WeChat because we know the consumer journey does not start in a single place in an omnichannel world. Even if a consumer buys a product in stores, she is also searching online for reviews, following influencers to hear their thoughts and watching makeup tutorials on Youtube. The technology should not just be a single silo because each platform has its own audience and the same consumer the brand wants to target wants to have a consistent experience across channels. Imagine if I am a shopper on Estee Lauder’s website. If I try shade 008, it should look the same on the website vs. in an AR application on YouTube. Our technology is useful because we work with all of these partners to build the same set of parameters for virtual try-on across these different platforms. More and more consumers want to hear less directly from the brand and do more social commerce. On live streaming, we are still building this and bringing it to the US. For example, one of our key partners ULTA is running livestreams with our technology like a revamped, mobile QVC while also having the opportunity to try on the product. Imagine if while you were watching QVC on your TV, you could simultaneously try on the cosmetic product: that is the experience we are enabling.

SN: How technologically sophisticated are these brands from an R&D perspective (especially those on the SMB side)? I noticed that you have a Shopify integration. To what extent, do you need to go through these existing platforms and leverage their distribution to access the SMB space?

LC: Beauty is a very long tail business. That’s why we created the plug-in for Shopify. If you look at the edges of the long tail, there are numerous up and coming amateur, influencer or indie beauty brands emerging everyday. They don’t have the luxury of a development team to help with this sort of functionality so they will likely rely on existing resources. Our-plug in makes it easy to integrate this module into this Shopify store with no coding. We want to democratize the technology to make it available to the lower end of the spectrum of the long tail. There are potentially 100,000+ merchants we could target on Shopify. The more consumers are exposed to this technology even in the long tail, the technology will become a must-have. In the future, if you don’t offer virtual try-on for beauty, we see this significantly negatively impacting your beauty brand’s sales. In terms of technology investment, brands are investing a lot more, but beauty brands traditionally don’t have a strong background in software development. More and more companies are creating the software tools that a brand needs. We are at the age where the integration between these customer commerce tools becomes more important for brands.

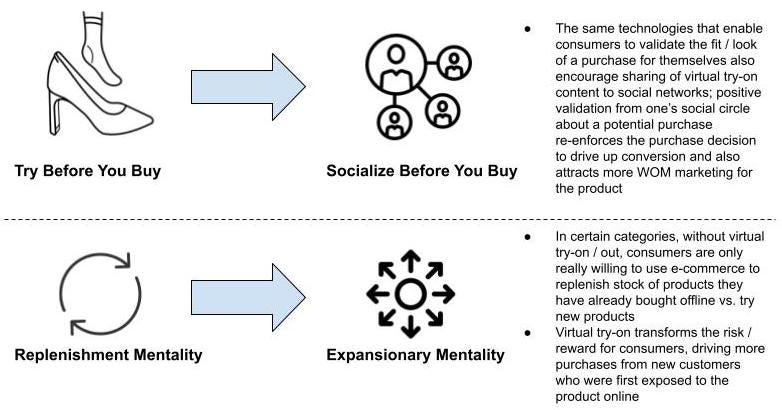

When done effectively, these social evaluation technologies facilitate two important transformations and shifts in consumer mindset: i) a move from “try before you buy” to “socialize before you buy” and ii) unlocking an expansionary consumer mentality:

Execution - As distributed social commerce enables more individual / independent creators to sell products to customers, there is an opportunity to leverage proprietary creator access to drive high purchase executions. For example, the first 100 people to purchase a new product release and share it with friends get to chat with the creator or receive exclusive content related to the creation of the product that provides more meaningful artistic context on the product consumption.

Extension - Live video shopping today is used primarily in the execution phase to deliver high transaction volumes for a new product. However, there is a large opportunity to leverage livestreams from creators, KOIs and KOCs post-purchase to educate about interesting use cases of a product and build communities to keep a consumer engaged with a brand post-consumption. This strategy blends the trifecta of entertainment, shopping and consumption to build brand affinity. AI-based digital concierge technology can also automatically follow up with customers that purchased a good about any post-purchase questions. These concierges can also play an important role in the consumer evaluation process pre-purchase.

For purposes of this piece, I am focused on the customer journey, but there is also a whole set of technologies to help creators better optimize for demand, design, distribute and monetize content and products that leverage their brand prior to product exposure at the consumer level. There is also an opportunity for end-to-end social commerce platforms to expand up the funnel by enabling more effective creator content product monetization. These social commerce platforms are advantaged in enabling better creator monetization by closing the loop on content engagement, product purchase and gaming data to inform how much, in which channels and exactly which products and content media creators ought to monetize.

Evaluating the Positioning of North America’s Usual Suspects

Understanding the state of social commerce abroad, the next logical question is, which player in the West is best positioned to compete to capture the future of global social commerce? Let’s evaluate the usual suspects:

There are three players that I believe each have three distinct moats in separate critical features of a robust social commerce platform:

Shopify is the closest scaled commerce-first platform we have to enable “Creator Focused” commerce by empowering independent retailers with commerce and logistics tools to compete with big retail. Shopify has one of the largest networks of independent retailers using its commerce infrastructure. While this stack isn’t optimized for micro-level, single person creator monetization, this network of independent retailers is valuable and its technology stack may be adaptable enough to drive value for creators. However, in its current state, Shopify lacks both expertise in gaming and the engaging content to generate meaningful social communities across its commerce portals. It could benefit from acquiring a gaming engine that independent retailers could leverage to monetize games around their own portals. Shopify did recently announce a partnership with Tik Tok to feature Shopify merchants in a new Shopify x Tik Tok business channel. On the one hand, this could mitigate the need for gaming if Shopify can help its merchants enhance its brand with video entertainment via Tik Tok instead of game-based entertainment. On the other hand, Shopify may be lending out its greatest asset to a Chinese player that dominates discovery, entertainment and social. What stops them from building out more proprietary / native commerce features within Tik Tok? As this section is focused on North American players, I don’t discuss Tik Tok in detail, but it of course has the building blocks to capture a lot of social commerce value.

Epic Games is world class in gaming and animation design. Its largest two assets as entrants into social commerce are i) its Unreal Creator Engine and ii) its massive user base with robust community effects within Fortnite. Epic can encourage creators and retailers to leverage the Unreal Engine to create digitally rendered virtual stores on animated maps that Epic stitches together in one unified avatar-based commerce interface. In effect, Epic could control the next generation commerce interface connecting distributed creator and retailer commerce portals. Further, the large existing user base from Fortnite serves as a massive initial demand source for creators to monetize. Epic lacks the network of retailers / creators selling physical products, but could easily own the UI layer of commerce. Their existing backend infrastructure (such as payments) that help it monetize in-app purchases could serve as an initial platform for a portfolio of creator-focused commerce tools, but it would have to acquire, develop or partner with other commerce tools to build out these capabilities further.

Pinterest has a large starting user base of 400M+ MAUs and a discovery interface that is more amenable to shopping than Facebook, Snapchat or Twitter. The discovery interface feels much like the curated lifestyle content focus of Xiaohongshu in China. Although its model is reliant on advertising, its attention economy focus has not been as publicly destructive to its brand as Facebook. Moreover, it is making meaningful strides to diversify its business to focus on creators and commerce. In September 2020, Pinterest announced a new slate of creator-focused tools. It is also launching some cool new commerce tools like Shop from Pins and Shop from Boards. Pinterest needs to continue to move aggressively away from a traditional advertising model, acquire gaming assets and build more frictionless and robust commerce capabilities to have a chance of competing against Epic or Shopify.

Twitter gets an honorable mention because of its recent acquisition of Revue, a newsletter service competitor to Substack, which is certainly a win for the creator community on Twitter. Moreover, it has become willing to experiment with subscription models to diversify away from traditional advertising. Still, given the recency of these efforts, I believe there is greater execution risk than Pinterest in executing the transition away from the attention economy. Further, the text-focused discovery feed is a handicap when it comes to shopping discovery.

My readers might be surprised to see Amazon and Facebook both outside the contender list. Regarding Amazon, its positioning as a third party marketplace vs. enabling sellers to own an independent, personalized commerce portal is hindering to creator-focused commerce. Third party sellers have to compete with core Amazon products and the best independent retailers and creators will gravitate towards owning their own shopping experiences in a world of distributed commerce. However, Amazon’s recent acquisition of Selz, a competitor to Shopify and BigCommerce, does signal an active effort to pivot its independent seller strategy. However, I am skeptical Amazon can transition to an environment more favorable for its third party sellers than Shopify without cannibalizing its core retail business. If it can, it does have a robust multi-media library and an unrivaled jewel in the gaming community and creator monetization (Twitch) that it could leverage to merge shopping and entertainment.

Facebook also faces a number of challenges: First, a large portion of the FTC investigation into Facebook revolves around anti-competitive restrictions on use of its APIs by developers that could pose a competitive risk to Facebook’s business. While it is by far the world’s largest social network, I believe that as Facebook is forced to offer a more open set of APIs linking to user social graphs over the medium-term, the value of its data moat will decline. Second, given its public misappropriation of user data over the years, Facebook’s public image is too tainted to give it credibility as a trusted commerce hub even if its recent attempts at creator monetization are successful. Third, Facebook has a track record of turning on the brands on its platform as it did in 2018 when it forced brands to pay an access fee to access their existing organic audiences. Brand and creators are less likely to have trust in building their businesses on the platform after seeing anti-creator moves like that manifest.

Still, I wanted to explore how newer social media platforms were thinking about the opportunity in social commerce to see if / how they differed from some of the longstanding social media giants. To learn more, I caught up with Manohar Charan, CFO of Sharechat, one of the largest social media networks in India and owner of Moj, the largest live video social network in India since Tik Tok was banned from the country. Interestingly, Sharechat’s approach especially through Moj is turning heads in the West. Snap just announced a partnership to integrate its camera kit into the app and Twitter reportedly offered to buy the company for $1.1 billion but was rejected.

My Conversation with Manohar Charan (CFO of Sharechat)

SN: Could you provide an overview of the founding story of ShareChat and how you differentiate vs. other social media players?

MC: Our founders realized in 2014, when the internet user base in India was just starting to grow that new users coming on the internet were not from tier 1 cities like Delhi, Mumbai, etc. They were not necessarily English speakers and culturally were different than those users from tier 1 cities. When they talked to their spheres of friends, they preferred to speak in their local language. Many users in tier 2 and tier 3 cities did not see enough content in their local language on traditional platforms. ShareChat started as a repository content platform where you could like and share content in your local language through WhatsApp. Eventually, data became extremely cheap in the country as Chinese OEMs came in and flooded the market with affordable smartphones. ShareChat was well tailored to meet the needs of these local users as more of them came online and began organizing digital communities. In July of last year, a bunch of content apps got banned in India and we were the only local player with capabilities to run a AI driven content platform at scale. We also sensed a large open market opportunity in the short video segment and since ShareChat was a multi-format content platform, we decided to launch a dedicated short video app Moj. It took us only 7 days to make this newly launched app #1 in Play Store in India. This new application, Moj, is the largest video network in the country.

SN: Given ShareChat’s roots as focused on tier 2 / tier 3 cities, are there certain features of the application that better tailor the platform and content to local levels?

MC: The platform is solely based on user-generated content. If you open different language versions of ShareChat, you will find very different tonality, unique content and cultural elements. For example, in one of the South Indian languages, it will be more about cinema and celebrities. In another language, it will be more about celebrities and jokes. If you go more into the hinterlands, you will see more about politics and current events. In other areas, the content will be focused on commerce between different shopkeepers. It’s not as much about the language difference but rather what each language signifies about each different cultural community.

Because of their wide reach and drive to achieve network effects (which incentivizes user quantity over community quality), it is difficult to create horizontal social media networks that preserve offline cultural communities / identities. The ability to leverage technology to actively preserve offline cultural communities and further amplify them online is game changing. I believe the leading players in global social commerce will channel the cultural distinctness of various pockets of creator communities around the world to similarly enhance the richness of online shopping experiences. Just imagine the unique cultural adventure and depth of physically shopping abroad combined with the frictionless user experience of online commerce:

SN: Why did Facebook not serve these local markets effectively?

MC: Facebook didn’t understand the nuances in these areas outside of tier 1 cities. For example, In some parts of the country, it is not looked upon as favorably for women to speak to strangers online. In other languages it was more common. In certain parts of the country, christmas is a predominant holiday but not in others. Our platform is a melting pot of all of these preferences but we preserve the unique cultural elements within each language’s digital community. We invest a lot of effort in preserving these unique communities: First, we have a team that stays in touch with top creators in each language that helps build in unique features from cultural feedback for each area. Second, our AI algorithms that decide which content is acceptable are trained on cultural nuances across regions. For example, a word could be considered a curse word in one part of the country, but be commonly used in other areas. Our algorithms screen for that. They are also trained on undertones (i.e. what is said vs. what is meant based on cultural differences).

SN: How has the user acquisition strategy evolved over time as ShareChat has transitioned from a tier 2 / 3 city focus into penetrating more tier 1 users?

MC: We have a very good representation of the audience on the platform now given our scale. This helps train our algorithms about what is best to serve a user when they come onto the platform. The content you serve a tier 2 / 3 user is different from the content you serve a tier 1 user when they first join. Early on though, one of the larger acquisition funnels for us was sharing content through WhatsApp. That was a very strong and efficient acquisition funnel for us for a long time before we achieved this scale. For most Indian users who come onto the internet for the first time, WhatsApp is the most default app, especially in tier 2 and tier 3 areas.

It’s really interesting that Sharechat built its audience by effectively using WhatsApp for free as its marketing engine. This is a common trend of some of the larger social commerce players in China like Pinduoduo, which acquired users in part by encouraging them to share deals with their WeChat networks. From a regulatory perspective, I believe that as the FTC forces the Western social media networks to develop more open and less anti-competitive social graph APIs, an opportunity will emerge to similarly tap into existing social graphs in more cost efficient ways to power an emerging social commerce ecosystem:

SN: Have you looked to monetize commerce and how do you view the opportunity for social commerce in India especially in these tier 2 / tier 3 networks that previously were not accessible to brands?

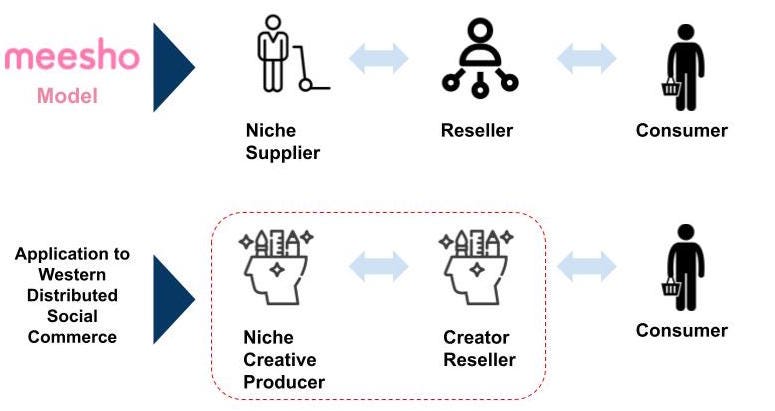

MC: We started with advertising which is the lowest hanging fruit which is part of most social networks’ strategies. In the west, all of the social media platforms continue to make most of their revenue from advertising. Average revenue per user in the East is smaller for advertising but can be larger overall when accounting for monetization in other segments such as commerce, gaming, etc. Despite having Flipkart and Amazon in the country, only a portion of tier 1 city users have been reached. ShareChat by its nature has already reached beyond this primary network. We have organically seen that some of our users have started utilizing the platform for commerce. We have noticed those trends but have not built specific features yet. One e-commerce model in India that has grown in popularity is the reseller network model, which was popularized by Meesho. This commerce model gets suppliers in place and then reaches out to individuals to ask them to sell the product in their network of friends who make reseller commissions. The sales in this model are based on trust. We believe resellers can use their platforms to reach out to their audience and drive more product sales. Going forward, we can also enable micro-transactions between users. In the country, cash-giving vs. gift-giving on holidays has been the trend. On a festival day, users already come to the platform to send their friends good wishes. These users should also be able to gift cash through the platform. Within Moj, we have deliberately not started monetizing users yet but do see the live streaming commerce opportunity there as significant going forward.

I believe that as production becomes further distributed across smaller units of creators (suppliers in the traditional retail sense), it will become increasingly important to channel elements of the Meesho model in Western social commerce. In the Meesho model, resellers helped make sense of a more fragmented retail landscape in India that consisted of smaller independent suppliers. These resellers vetted niche suppliers (who were sometimes unreliable) and curated options of potential product orders that they would share with their consumer networks and then placed volume-specific orders for group goods. Meesho applied the reseller model at a time when Indian commerce was moving from a relatively fragmented system towards more centralization.

The drive towards a creator economy shifts commerce from the centralized Amazon marketplace model towards a more decentralized and distributed commerce system where the unit of creative production shifts from corporations to individuals. In this distributed commerce world, Meesho’s model is highly relevant. Instead of traditional roles of niche suppliers and resellers, in the creator economy, these agents converge into creators that instead hold multiple hats as both producers and resellers / tastemakers recommending goods to their fanbases. The passion economy inherently increases the long tail of suppliers, creating a need for other creators to vet and curate products for their own loyal micro-communities. Further, the cost of overproduction in the passion economy is higher than the corporate economy as businesses owned by niche, individual creators have less operating leverage, i.e. can spread their fixed costs to operate over fewer product orders. Leveraging creator resellers to more accurately gauge demand from their highly engaged digital micro-communities will enable healthier supply / demand economics and mitigate overproduction. To learn more about the intersection between the creator / passion economy and social commerce, I spoke with Zach Oschin, CEO of Elenas, a leading social commerce platform focused on Latin America and based in Colombia. Meesho is actually an investor in Elenas. The business empowers women in Latin America to start, manage and optimize wholesale reseller businesses by selling into their micro-networks / follower bases.

A Snapshot of My Conversation with Zach Oschin on The Intersection of Social Commerce and the Passion Economy

SN: Could you discuss how Elenas’ business model has the potential to help power the passion economy across Latin America?

ZO: Elenas sits at the intersection of passion economy and social commerce. From my perspective, the passion economy has become very concentrated amongst top creators who thrive by monetizing on top of large user and wealth networks. There is a steep power curve of people who make the most money on Patreon, Youtube and other sites that help individual creators monetize their passions. As individual creators look to monetize their products through other channels, the supply side of giving individuals enabling infrastructure tools becomes more important. Elenas provides the technology stack for independent women to manage online sales through an out of the box solution. Any woman, even if she has no selling experience or resources has access to our at-scale logistics pricing and operations, selling technology, wholesale pricing on product portfolio, and more to build out her own small business. Our base consists of mostly regular women who have friends or family around them who view them effectively as micro-influencers and who look to them for product recommendations. From our experience in Latin America, larger scale influencers aren’t great at getting items sold. They post on a large social media site to millions of followers hoping to convert a very small percentage. The issue is that these traditional larger influencers aren’t actively pushing the sale and cultivating individual relationships with their follower base when trust is so important in purchasing behavior in the region. Our sellers have a more authentic relationship with smaller micro-communities of end-buyers and are thereby more incentivized to sell. Our model builds on the passion economy by empowering independent women with entrepreneurial aspirations in retail to achieve upward mobility by owning their own reseller business and becoming product tastemakers, without needing to have existing wealth or fame.

Similar to Xiaohongshu’s differentiation through a focus on KOCs, Elenas and other distributed commerce reseller models have the potential to drive higher sales volumes for wholesalers and D2C retailers by tapping into micro-networks with strong community effects and authentic consumer relationships. This benefit to the wholesaler is reinforced by strong creator loyalty by empowering the individual reseller or small business owner through the promise of upward mobility.

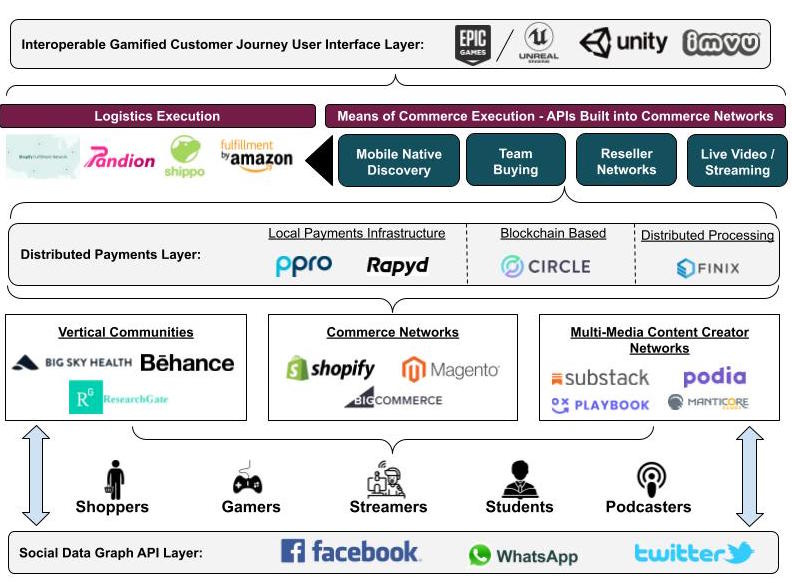

The Building Blocks for Western Social Commerce

The Pinduoduo and Sharechat model of scaling symbiotically on top of existing platforms makes a lot of sense for the development of Western social commerce. We already have nearly all of the social commerce building blocks in existence albeit in independent businesses: it will just require the right business infrastructure or set of companies to create the interoperability and integration to combine these pieces into a coherent ecosystem (or mega platform?). I think the latter is less probable as regulatory scrutiny heightens over the current big tech giants. I find it unlikely that a current technology giant will emerge as the champion in social commerce with winner-take-all economics because they will likely be constrained by regulators with regards to the sort of transformative (and likely anti-competitive) M&A that building that category of mega-platform would entail.

It is possible that while regulators clamp down on today’s largest technology players, a new entrant could slip under the radar: identifying an under-developed part of the ecosystem below as a trojan horse starting use case for their business and then strategically assembling the right combination of proprietary social commerce building blocks through organic development, M&A and partnerships to capture a disproportionate share of value in Western social commerce 2.0. Given the current regulatory environment, breadth of technological capacity required and moats of today’s ecosystem stakeholders, I think a partnership model that more evenly distributes social commerce economics across stakeholders is the most likely outcome over the coming decades.

I envision the ecosystem developing as distributed multimedia and vertical creator and community networks that foster meaningfully engaged micro-followings by tapping into open social graph APIs. These networks will power commerce and be enabled both by i) localized, distributed and creator-friendly payment layers, ii) a set of APIs that democratize best-in-class commerce execution (discovery, team buying, reseller functionality, live streaming, virtual try-on, etc.) and iii) efficient logistics execution. I believe that gaming engines will serve as the interoperability layer that controls the user interface that stitches together separate portals, creator engagements and vertical communities into a next generation unified social commerce digital world.

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.