Unpacking Enabling Infrastructure Businesses: A Two Part Series

Unpacking Enabling Infrastructure Businesses: A Two Part Series

Part I: Catalyzing VC Sourcing Leverage Superpowers

Welcome back to the Innovation Armory! This week I’ll be doing a two-part mini series breaking down enabling technology infrastructure businesses. Part I focuses on how enabling technology businesses give venture capitalists sourcing superpowers and how this fact is under-weighted when making investment decisions. Later in the week I will publish part II which is a case study unpacking open banking enabling infrastructure in Southeast Asia. Thanks in advance to Todd Schweitzer (CEO & Founder) of Brankas and Nirali Zaveri (CEO & Founder) of Friz for sharing your perspectives for this series!

Read more of today’s piece for more on:

The importance of expanding the definition of internal investment success beyond standalone investment-level return

Why portfolio sourcing and synergy power are also important benchmarks when it comes to evaluating enabling infrastructure investments

How enabling infrastructure technology businesses can afford their investors meaningful sourcing leverage

The parallels between enabling infrastructure businesses and startup accelerators

Why placing more small strategic bets in enabling infrastructure investments may yield a greater fund ROI than hiring incremental sourcing-focused junior employees

Why creator funds specifically should increase their exposure to enabling technology businesses

The convergence we will see between commercial and investing activities of venture-controlled NewCos in enabling infrastructure verticals

This is a long post so if your email gets clipped at the bottom, make sure to click unclip / visit The Innovation Armory to check out the full read.

If you’re interested in more thought pieces, you can also subscribe below for future updates from The Innovation Armory:

Also, If you like this piece, feel free to share with the link below:

Catalyzing VC Sourcing Superpowers

Enabling technology businesses particularly excite me as an investor especially those that address a critical infrastructure gap. An enabling technology business is one that sells a critical infrastructure-layer technology that enables other businesses to efficiently provide products to customers. It solves a critical infrastructure gap that once solved spurs additional innovation to be built on top of its ecosystem that previously would not have been possible to build out. That core infrastructure layer generally benefits in some way from the upside of players that choose to build on top of it. The iPhone and the app store are an enabling technology for deploying and distributing all of the applications we use everyday. APIs for open banking are one of the greatest recent examples of enabling technologies that in the US helped enable the fintech middleware that drove the creation of consumer applications we all love like Venmo and Robinhood. My affinity for these business models is not only because I believe these companies have the ingredients to generate outsized returns for a particular investment (they do!) but also because they create sourcing leverage for venture capital firms at the portfolio level.

Some venture firms take too much of an investment-specific view on enabling technology businesses vs. a portfolio-wide view. Here’s an example of what I mean. The venture firms that invested early in Plaid are making a killer return, but let’s imagine a counterfactual scenario where this was not a top performer in their fund:

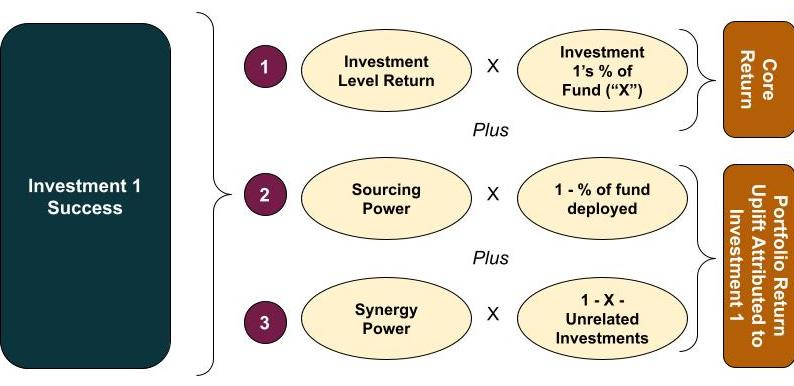

Venture Firm A invests in Plaid but it turns out Plaid was only a middle of the road performer. However, by virtue of investing in Plaid, Venture Firm A learned about Venmo, Robinhood, Coinbase, Betterment, Acorns (all early customers of Plaid) before most other tier 1 venture firms and has a better understanding of the problems they were tackling through access to commercial discussions those businesses had with Plaid. Let’s say Venture Firm A targets a return of 10x on investments and only realizes a 5x theoretically on Plaid, but is introduced to Coinbase and Venmo on which they earn way above a 10x! Does that make Plaid a successful investment for the firm? I’d argue yes because by virtue of writing a small check into Plaid, this firm had a meaningful sourcing advantage in sourcing whales that have the potential to return their whole fund as early as possible. In an increasingly competitive venture market, the success of an investment shouldn’t be held solely to the standard of IRR and MOI for a specific investment, but also contextualized to a broader standard: what was the uplift to the firm’s overall portfolio-wide return by virtue of investing in this business.

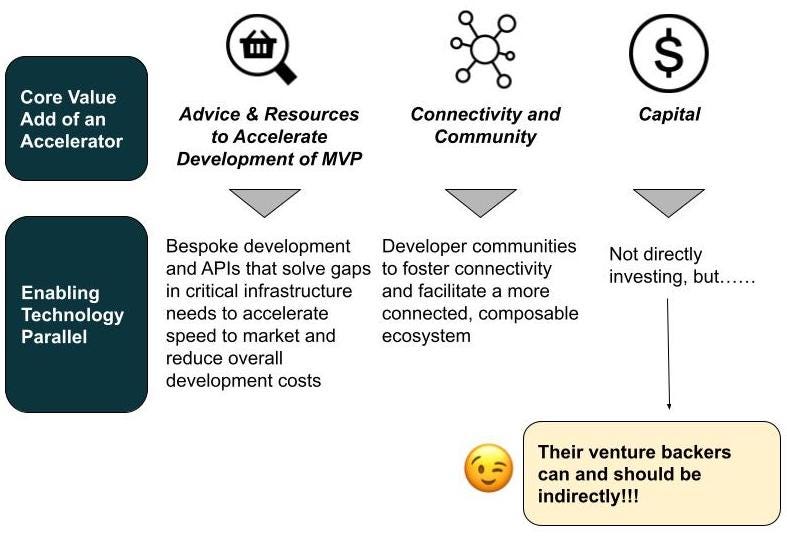

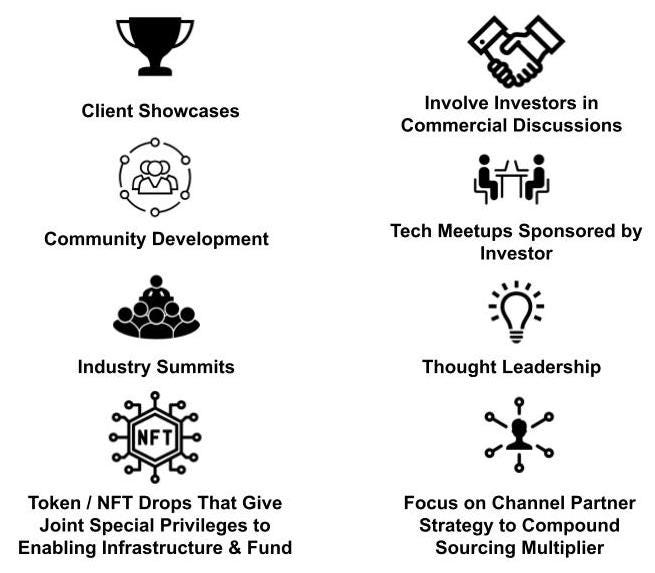

In the above, by “sourcing power”, I mean the aforementioned superior access investors can get to early stage companies building on top of an enabling technology ecosystem. By virtue of the fact that these enabling technologies are solving an infrastructure gap that has yet to be solved, these ecosystems (at least those that become successful) are necessarily one of the best places from which to source early stage investments in the particular end market that they serve because they are working to enable use cases that will spur innovation that was previously impossible before this infrastructure layer. That means these networks and their founders are most likely to have the connectivity, foresight, network effects and deep domain expertise to make smart predictive bets on the next generation of innovation in a given vertical. This term is weighted by the % of the fund undeployed since this benefit impacts all potential future, but yet to be sourced investments in the fund. By “Synergy Power”, I mean that by virtue of investing in these companies at earlier stages, investors can help shape the use cases that they focus on and give their other existing portfolio companies in adjacent verticals the opportunity to benefit from close access to get their most critical needs addressed by the enabling technology layer. This term is weighted by the % of the existing fund investments which would benefit from this close access. Venmo, Robinhood and Coinbase were great companies on their own, but I think they were in part particularly outsized winners because of this early access and partnership they had with Plaid. Now, you don’t necessarily need to invest in a company to get an existing portfolio company to benefit from their solution. That being said, there is a different level of attention, direct access to the founder / engineering teams, etc. that you get as an affiliate of an investor in the business. Taking a step back, enabling technology businesses have parallels to distributed, technical startup accelerators just without directly making equity investments into their clients. That is why you see some fintech infrastructure players hosting startup showcases and industry summits:

There is a separate kind of power that is a less pronounced kind, learning power. Some enabling technology companies create such a sea change in a sector within a given region, that being in the Boardroom and having such deep and intimate access to their strategy gives you a massive leg up from a learning perspective in being able to filter your top of funnel as a venture fund in a more powerful way.

You might be thinking, what is the probability that a venture firm would have sourced a Coinbase or a Robinhood from Plaid’s network if Plaid only returned a 5x to a seed investor? In this counterfactual, would these companies also have returned lower to their investors? Certainly the probability would be lower vs. the super successful outcome that Plaid has been in reality because it would mean that Plaid didn’t end up creating as much value for its clients. A couple important points though:

Even if this specific enabling infrastructure technology company is only moderately successful, it can still generate sourcing leverage. If Plaid won Coinbase as an early client and then churned it to a competitor (or even if it pitched and went far in a commercial process with Coinbase), both can still be avenues to making an early introduction to a winning bet

This player might end up not needing this infrastructure layer or moving to a competitor, so the opportunity indirectly sourced can still be of high caliber

There is a chance that the enabling infrastructure in question turns out to be not that critical, but I believe the type of company that seeks to form partnerships with enabling infrastructure businesses is overall of a more innovative and boundary-pushing mindset and category by tackling some of the most complex, large problems in big end markets

Investors should still have a different bar or tolerate a higher valuation for evaluating enabling infrastructure investments than pure application / product investments because of their potential to provide portfolio-wide sourcing and synergy optionality

In my opinion, if this argument is true, this is not a reason to underweight on enabling technologies but rather a reason to overweight but bet on multiple smaller players in adjacent enabling infrastructure spaces; in other words distribute fund concentration into a series of smaller checks to bet on the category as a holistic sourcing node as opposed into any one company

This also avoids the issue of indirect fund concentration, e.g. if you initially bet on just Plaid, Robinhood and Coinbase, you would have had both primary investment exposure to Plaid but also indirect critical commercial exposure through your secondary investments

My argument so far has focused on the impact of an enabling technology investment within a given fund, but FYI these benefits in reality can be larger and extend across funds. The sourcing power doesn’t just expire after you’ve deployed capital from that particular fund…

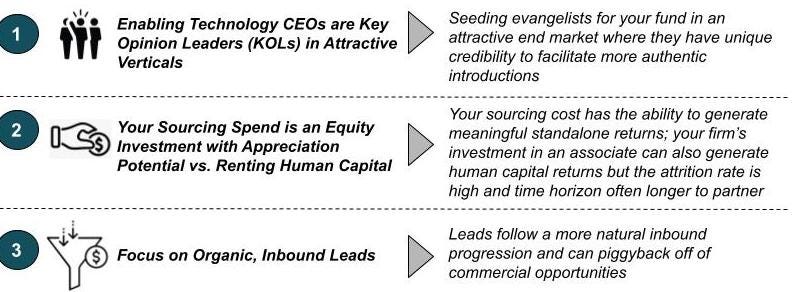

It has become a common model in venture for top firms to hire scouts and focus junior associate efforts on sourcing and hunting for new leads. These folks are paid to get smart on a market and make a ton of outbound (often cold) outreach to companies whose business models they don’t really understand until they have a conversation. Plus, these firms often have junior employees spend even more on market reports and calls with expert networks that contribute to total sourcing cost. Many firms have been very successful deploying this strategy. However, more firms should think about placing small strategic early stage investments in enabling technology businesses specifically as part of their sourcing costs, potentially even hiring fewer sourcing focused associates and re-allocating their salary into enabling infrastructure equity. This is partially why some firms have entrepreneurs in residence, but I think firms should more explicitly think about these smaller earlier stage bets in enabling infrastructure as sourcing acquisition cost for new investments. This could even be done from LP fees or from the balance sheet of the fund as opposed to sitting directly at the fund level. Who do you think would be better at sourcing a fintech investment for a VC firm?

Even though associates dedicate 100% of their time to the fund vs. a startup where the executive team is spending 99.9% of their time on the business and not sourcing investments for you, the quality of average lead and likelihood of converting is likely to be higher. While there is an importance to and time and place for this outbound sourcing strategy, there are a lot of reasons why I think writing more earlier stage checks in enabling technology businesses should be a diversified prong to the sourcing investment strategy for many VC funds:

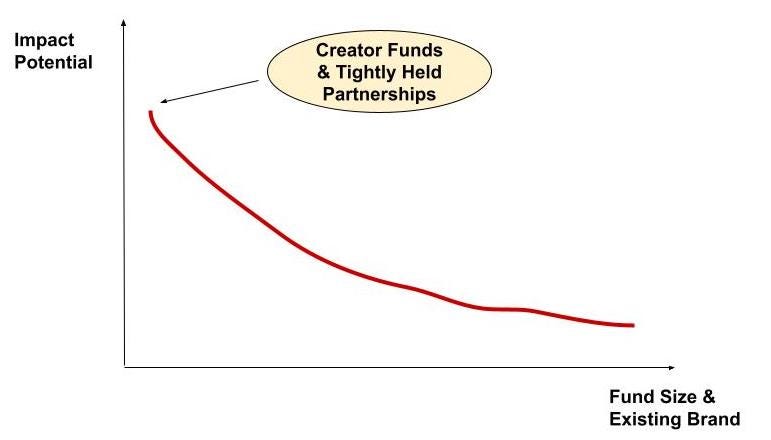

There are diminishing returns to leveraging this enabling infrastructure sourcing strategy as funds mature and brand becomes stronger. In tier 1 global institutional venture firms where brand is incredibly strong, top of funnel lead generation is not a problem. While those firms can benefit from thinking about enabling infrastructure investments through a sourcing lens, I think the highest impact here is especially strong for smaller, tight-knit funds that are still building brand and where they most need to generate a multiplier effect to their sourcing efforts:

As there is a renaissance in creator-driven investing and solo capitalists founding their own funds, looking for infrastructure-type investments with high sourcing leverage will be critical to achieving a multiplier effect to top-of-funnel leads and creating an ability to increase AUM and move up market in an efficient way. Especially in an increasingly competitive venture environment, creative strategies and angles to meet companies faster in a high signal way that cuts through the clutter will become increasingly core especially for creator-led funds.

There is an interesting opportunity to augment this strategy through mutually reinforcing commercial and investor related initiatives, e.g. influencing early activities of an enabling infrastructure startup to carve out a portion of time to focus on efforts that are synergistic on both the commercial and sourcing / investing fronts. It becomes more difficult to wield this influence the less economic ownership you have as an investor so I think this strategy makes the most sense for venture funds that are open to starting captive NewCos where they have a meaningful / control stake in a business specifically in areas where they have identified an enabling infrastructural deficiency either in a specific end market or geography. Some initiatives that are synergistic on both the commercial / go-to-market front and sourcing front include:

It’s important not to view this strategy as adding to the plates of founders who need to focus on executing on operations and product vision. Rather, the point is that existing activities that are already done commercially and for a business’ go-to-market strategy can be optimized with minimal incremental time / capital efforts to drive high sourcing leverage. And to build out organizational best practices to know where investors can and should plug in to these processes to drive outsized portfolio-wide outcomes.

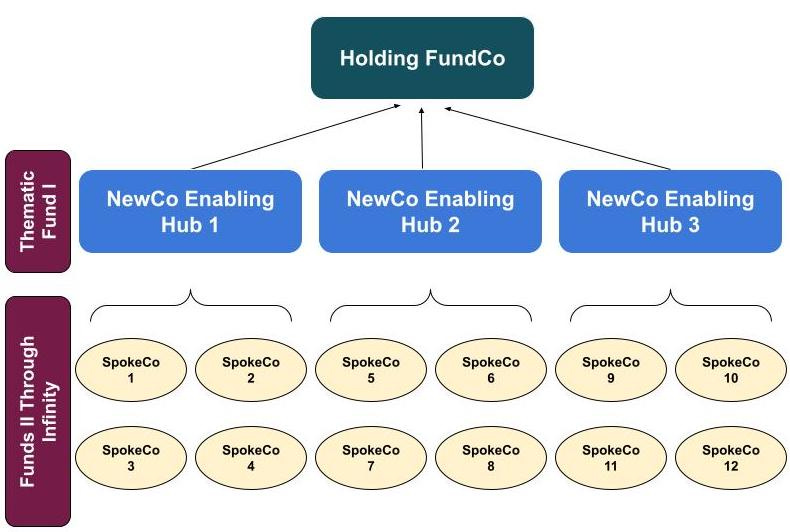

Lots of platforms have adopted the strategy of seeding creators through captive creator funds. Larger enabling technology businesses like VISA and Plaid have active corporate venture units that source investments to drive both commercial and financial upside. Corporate venture units often size their commercial contribution and potential financial returns simultaneously and synergistically. More funds will start creating NewCos in critical enabling technology verticals and leverage those core “hubs” as their primary follow-on vehicles to source, deploy capital in and create value for subsequent “spoke” / secondary investment opportunities.

You can imagine a fund launching a blitzkrieg strategy of seeding a bunch of enabling technology layer “NewCos” with meaningful / majority investments and experienced founders across different thematic verticals. These could all serve as hubs for sourcing and driving value for subsequent smaller / minority equity level 2 investments for subsequent funds across geographies, especially in areas missing important enabling layers of their digital ecosystems:

On sourcing strategies, the smartest funds will be thinking about which enabling technology business types will provide the most sourcing leverage across technology primitives (specifically across the crypto ecosystem), attention / discovery layers and geographies. These areas will become the spokes to the hub(s) that will become the next tier 1 global venture competitor. I have my own thoughts here I’ll share in a future piece, so stay tuned 😎

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.