Waking the Sleeping Giant in the Global Financial System

Empowering emerging market credit unions with next generation digital tools

Today’s piece is about the massive opportunity to empower credit unions in emerging markets all over the world. Kwara is empowering elevating emerging market credit unions with best-in-class digital tools to better engage, service, recruit and deliver value to their members starting in Kenya, South Africa and the Philippines. Thank you Cynthia Wandia (CEO & Co-Founder) and David Hwan (COO & Co-Founder) for sharing your perspectives for this piece. Read on for more about:

Sizing the sleeping giant opportunity of credit unions and their growth potential

How under-penetrated emerging markets are relative to the developed world from a credit union perspective

The historical benefits and considerations of credit unions for potential members

How Kwara is empowering credit unions with its SaaS administrative platform and online / mobile banking tools

How clients with cooperative structures help mitigate competitive risk for startup partnerships

Leveraging credit unions as a distribution channel for other financial services

The opportunity to build pockets of affinity-based neobanks across the world

How credit unions may actually become critical nodes of activity for play-to-earn gaming ecosystems

This is a long post so if your email gets clipped at the bottom make sure to click unclip / visit The Innovation Armory to check out the full read.

If you’re interested in more thought pieces, you can also subscribe below for future updates from The Innovation Armory.

Also, If you like this piece, feel free to share with the link below.

Venture capital has been pouring money into neobanks and digital challenger banks to take on traditional financial institutions. The largest players in this sector have attracted some of the largest funding rounds and valuations within the fintech sector including:

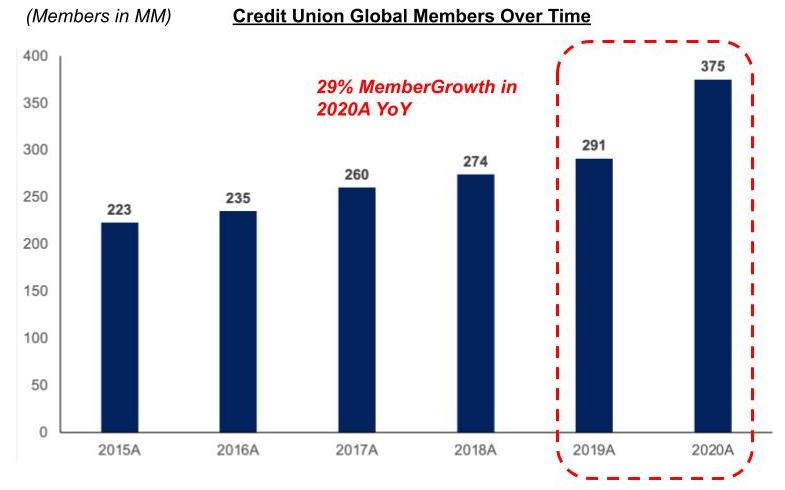

Investors are also flocking to fund more specialized neobanks including those focused on teens, women, under-represented minorities and certain professional groups. However, the neobanking sector is building to largely disrupt traditional globalized financial incumbents, but there is a sleeping giant (with meaningful economic influence) that looms below the surface that many leading players are ignoring: Savings Cooperatives and Credit Unions. According to the World Council of Credit Unions (WOCCU), there are over 375M credit union members served by over 86K credit unions globally across 118 countries. When comparing that membership base to the economically active population in those countries between ages 15-64, this count represents a 12% penetration rate on economically active potential member accounts as compared to banks and other financial institutions:

The pace of credit union membership growth has also been accelerating in recent years with global growth increasing by nearly 29% YoY in 2020 vs. 2019:

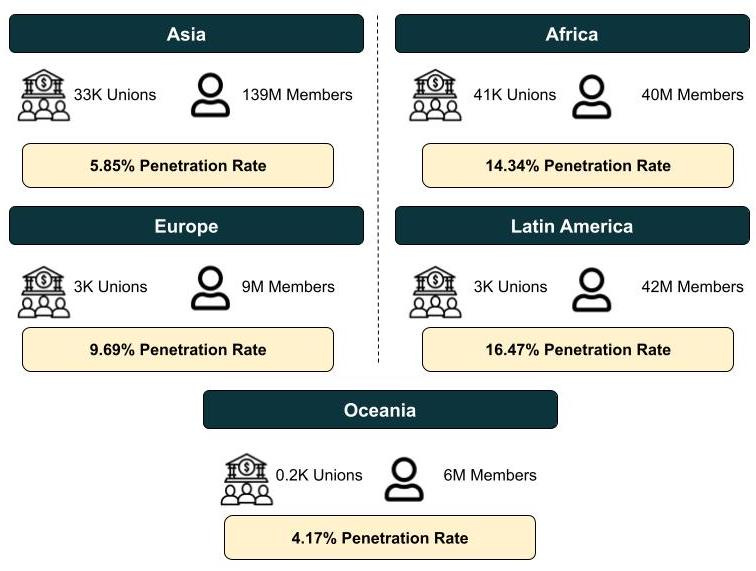

Interestingly, the most meaningfully high penetration rate is in the US at >50% penetration, which includes subscription to financial products (such as auto loans) that are sponsored by credit unions. When comparing such high rates in the US to the rest of the world, there appears to be a large whitespace opportunity to extend and grow the penetration rates of credit unions in emerging markets, particularly in Africa where the average member count / union is lower than other regions across the globe:

The Opportunity to Serve Credit Unions

You might be wondering what exactly is the difference between a credit union and traditional incumbent banks? At a high level, there are a couple of key differentiators:

Banks are for-profit whereas credit unions are not-for-profit and owned by their members. Value is re-distributed back to members in the form of dividends, price cuts or other mechanisms

Credit Unions are more focused than banks in their activities in that they mainly focus on lending and saving activities, whereas banks will generally expand to other financial services products for their clients

Credit Unions are generally more highly localized and often have an affinity-based element to them (e.g. serving farmers, teachers, etc.) whereas banks have a more horizontal customer focus

Credit unions have historically been under-served from a technology perspective relative to other parts of the financial ecosystem largely because they had smaller branch footprints vs. traditional banks and therefore had a lower account monetization potential. Before understanding where and how technology can catalyze growth among credit unions, it is important to understand some of the historical benefits and constraints of credit unions vs. traditional banks. One primary benefit, because credit unions are owned by their members, is that credit union fees tend to be lower because they don’t have a profit incentive / are not beholden shareholders who are not also users of the product or members of the credit community:

Other important considerations when comparing a credit union to a bank include tax benefits, localization, accessibility, product experience and scalability:

Tax Status - In the US, credit unions are exempt from all taxes except for local real property and personal property taxes as outlined in Section 122 of the Federal Credit Union Act (12 U.S.C. § 1768). Globally, industry estimates indicate that 70% of the world’s credit unions do not pay corporate income taxes. While regulations vary by region (for example, Australia does tax credit unions at normal rates), in geographies where unions garner favorable tax status, they are able to retain greater earnings to deliver greater value to members in the form of lower fees and competitive rates.

Localized Service - credit unions are often much more localized than traditional financial institutions and many developed in the context of specific geographic communities. While this can create accessibility problems (to be discussed later) it can also engender greater trust & customer loyalty and foster higher quality white glove service, which can increase customer satisfaction.

Accessibility - because credit unions are more localized or specialized (if affinity based) than traditional banks, they have historically been less accessible due to a couple of factors: a) more limited / less optimized outbound marketing initiatives, b) inability to service customers in distant geographies and c) less of an historical focus on digital distribution. The localization element combined with limited digital distribution has historically made the model less scalable.

Product Experience - while service quality may be high, because credit unions dividend out their excess earnings to union members, they inevitably have less funds available to re-invest in their product to improve value for community members absent members voting to forgo their distributions. Excess funds that are dedicated to in-house technology development inherently reduces the dividends payable to members in a given period. Even if investment could yield higher member fees or reduce internal operational costs, the ROI is uncertain for these unions because technology development is not their core competency and many are not at a scale for this type of development to make sense. Outsourced third party software options have historically been limited as credit unions have been less of a focus in the fintech community until recently. Third party software providers have the opportunity to improve product experience without meaningfully impacting dividends by helping save credit unions costs by helping them run more efficiently

Third party software developers can help credit unions solve these traditional disadvantages that may have dampened historical credit union growth. However, the focus within the technology community to-date has generally been on North America and developed markets, largely ignoring the massive credit union opportunity outside of North America. This has left a large vacuum for a player to win the large credit union digitization opportunity in emerging markets:

Kwara is Making the Financial System Fairer by Empowering Grassroots Players

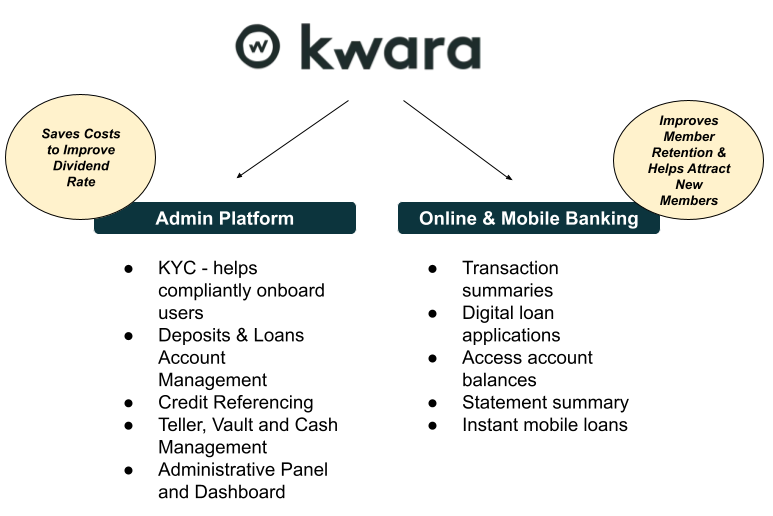

While much of Silicon Valley focuses on developed markets, Kwara is helping digitize the 80,000+ credit unions outside of North America by focusing on emerging markets starting with the Philippines, Kenya and South Africa. In these very same emerging markets, there are multiple neobank players vying to win customers and bring unbanked populations online: think Tonik (Philippines), TAG (Pakistan), FairMoney (Nigeria). Interestingly, in those very same markets, Kwara is selling to and working with credit unions that often have deep local roots, entrenched customer loyalty and on-the-ground distribution. Kwara is providing an end-to-end stack to these unions that help them optimize both back office workflows and enable them to offer best-in-class mobile banking capabilities:

While there are numerous ways Kwara is and will continue to add value to its credit unions, I am most bullish on a couple of opportunities and the transformative impact they will have credit unions’ operational efficiency and growth trajectory:

Deposits & Loans Account Management - automating and digitizing the workflows related to accepting deposits and disbursing and managing loans will help create meaningful operational savings for credit unions that can be returned back to members in the form of higher dividends

Customer Relationship Management - creating proprietary lead and member management systems, will allow credit unions to more effectively convert member leads, manage customer marketing initiatives and accelerate their growth into new geographies. This will help credit unions (especially those that are affinity-based) expand beyond borders / specific regional constraints

Instant Mobile Loans - traditional micro-finance players have been accused of using shaming and intimidation tactics to collect on digital loans. Credit Unions are unlikely to use these methods because they are owned by their members and the community-based nature of the financing already creates more of a social incentive to repay the loan

I caught up with Cynthia Wandia (CEO & Co-Founder) to learn more about how Kwara has the opportunity to help build a fairer global financial system by empowering credit unions. At its core, it comes down to incentive alignment:

“Credit unions at their core are the most incentive aligned financial institutions, given that the shareholder and depositor are the same. By offering low interest rates and a social-based alternative to collateral, they directly address the financially vulnerable who would otherwise resort to predatory loan sharks to make ends meet.”

Where you lack this incentive alignment, it can create mounting debt obligations for citizens of the emerging world where digital lending lacks proper controls and can actually decrease an overall population’s financial resiliency.

Mitigating Competitive Risk Through Cooperative Structures

Kwara has the opportunity to build a global neobank in partnership with credit unions by building a network of its own non-competitive financial products and creating a marketplace for other fintechs to sell into credit unions. This opportunity is uniquely created by the fact that Kwara is selling its software to non-profit or cooperative organizations without the purely capitalist incentive of maximizing value to shareholders. Traditional banks and fintechs that are for-profit have the incentive to build, buy and develop additional fintech products to expand the scope of their business activities and upsell new products to customers to deliver greater economic value for shareholders. Credit Unions are not motivated by the same profit incentives: they are motivated primarily to a) fulfill their mission of providing depository, savings and lending services at a cost-effective price point and b) returning any excess profit in performing that mission to members.

That means that Kwara has the opportunity to sell a whole range of other fintech-related products to members of their client unions, leveraging the unions as distribution channels with limited risk that these credit unions will take on these other fintech activities themselves.

This is not the case for other fintech businesses that sell to B2B customers or partner with businesses who have traditional profit incentives. When dealing with a potential partner incentivized by traditional shareholder profit maximization, that partner is generally incentivized to re-write contract terms and expand the scope of their commercial activities in the name of greater profits for their own core business:

Cooperatives are more trustworthy partners to distribute through that pose less of a potential risk of introducing a conflict of interest / competitive threat. Though likely not needed, Kwara’s business model would still be viable if the credit union mobile banking and administrative software were to be under-priced as a loss leader to instead focus on earning margin from sale of non-competitive fintech products into the credit union membership base through their loyal, local and entrenched distribution channels. Any price reductions or concessions would be at worst a customer acquisition cost with a high ROI and fast payback period. Plus, this B2BC approach allows Kwara to acquire users for these products with effectively no incremental marketing spend. Kwara could develop some of these other fintech products themselves or also distribute the products of other players through its exclusive distribution channels and take a meaningful take-rate by bringing online previously offline and inaccessible consumer finance customers. The list is nearly endless, but some areas where Kwara could either build or offer 3rd party products through a mobile marketplace include:

Affinity Groups Without Borders

Beyond traditional fintech products like insurance, trading, etc., specifically for affinity based credit unions, I think there is a really interesting opportunity to leverage credit union networks to sell vertical-specific SaaS and enterprise software. For example, farmer, faith-based and teacher focused credit unions have historically been popular affinity / profession based credit unions. There are two primary exciting vectors that arise from connecting local affinity groups through Kwara’s global network of credit unions:

Fintech Specialization / Verticalization - just as there are new neobanks emerging that are focused on teens, creators, under-represented groups, etc. who all have unique needs, select affinity groups could also benefit from more bespoke financial / banking products that are customized to their unique circumstances. For example, farmers might benefit from commodity trading to hedge their personal savings against structural risks in crop cycles. Or, a faith-based affinity credit union might appreciate the ability to designate funds to donate to charity. Perhaps an Islamic credit union would appreciate additional compliance workflows to ensure the lending is consistent with sharia law.

Non-Financial Software Distribution - there is a broader trend towards verticalization of previously horizontal technology solutions. For example, there have been the emergence of vertical players in the ERP and POS categories that are disrupting horizontal players in specific verticals where they provide the end-to-end needs of an industry in one solution including order acceptance, payments, CRM, operations management, etc. A couple of examples include:

Kwara could create a marketplace for traditional SaaS vendors to sell into professional affinity groups with members who might be key stakeholders at potential B2B customers. For farmers, for example, if you interface with their banking and financing stack (which is critical for both the farmer and his/her business), there could be value in providing access to a full stack bundle of other farming solutions or in connecting agricultural product / software vendors with your global affinity network and delivering value by integrating affinity finance applications with operational applications. Below is an illustrative example for the farming space:

At scale, this financial and digital infrastructure to service affinity groups combines the trust and retention benefits that come with local distribution with best-in-class digital technologies. This is the best of both worlds by pairing global technology with a local understanding of markets unique to tenured credit unions. This combination exists in the hospitality industry in the case of franchisors / franchisees where franchisors bring global best-in-class products and processes to bear on local markets where entrepreneurs have some creative liberty to tailor the experience to their local markets. While franchisees normally face meaningful operating restrictions from franchisors, in Kwara’s situation, credit unions remain in full control of their operations while subscribing to Kwara’s SaaS technology, but trade independence for allowing Kwara to sell other non-competitive products to their end users.

Credit Unions as Nodes in the Play to Earn Gaming Ecosystem

I see a lot of parallels between guilds, decentralized autonomous organizations and cooperative structures like credit unions. The International Cooperative Alliance defines cooperative legal structures as “people-centered enterprises jointly owned and democratically controlled by and for their members to realize their common socio-economic needs and aspirations.” Structurally similar to cooperatives, DAOs are communally owned by their members and also blend socio-economic, community and financial incentives.

DAOs have further operational superpowers in the organization, administration and financialization of a cooperative through the unique use of web3 technologies. Okay, maybe instead of a kermit mirror meme, a Darth Vader meme is more appropriate since cooperatives are kind of like the legacy father to DAOs enshrined in our legal system before web3:

Further, DAOs, and more specifically gaming guilds have the following characteristics in common with credit unions:

Just as credit unions are grounded in an affinity-based association of members, guilds are often tied to a common affinity (namely the virtual world / game the guild primarily operates in). This gaming affinity is increasingly becoming more of a professional affinity with the advance of play-to-earn business models where scholars “work” in games. Play-to-earn progression is creating this convergence.

In credit unions, members both lend to and borrow from other members, with excess dividends distributed to all members proportionate to their economic share. In DAOs, scholars effectively borrow from other members of the DAO to play in games with digital assets. These assets then generate yield that is distributed back to owners of the DAO proportionate to their economic stake. Sound familiar?

By empowering credit unions in emerging markets, Kwara is building a network that could be used as a superstructure to supercharge a global community of affinity-based virtual world guilds and DAOs. Just as fintech and software vendors will look to sell to financial end users through Kwara’s credit union marketplace, I believe more and more guilds will want to reach emerging market credit union users through Kwara:

Credit union members already understand the importance of economic ownership and require less education about the upside from participating in cooperative / DAO structures. They are amenable to tying the financial lifeblood of their professions inextricably to cooperative and communal structures

Members can contribute their excess dividends to purchase scarce digital assets and in-game assets and property via a guild or DAO. We might even see union members pool would-be distributions with other members to purchase virtual world assets to generate yield for the credit union

Emerging market credit union lending activity will increasingly overlap with loan use cases in P2E gaming where scholars want to borrow funds to purchase scarce assets. It may make sense for some of these types of loans to be paid even be paid back in kind through gameplay vs. financially

For certain affinities, credit unions could pose an interesting guild recruitment source (e.g. farmers in farming guilds could want to supplement their real world income by performing digital work in virtual farming games)

Credit unions can serve as a viable local finance offramp if a company like Kwara were to build the rails to connect a guild crypto wallet to fiat credit union savings accounts

Kwara will have proprietary access to the largest network of emerging market end users that understand and value communal ownership. In my opinion, it is only logical they will play a critical role at least from a distribution perspective in expanding the sphere of participation in play-to-earn games. Involving highly localized, historically offline financial institutions in the global crypto gaming movement. Do I sound crazy?

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.