Your Net Worth is A Lot Higher Than You Think

Your Net Worth is A Lot Higher Than You Think

How Twig is redefining wealth with a “Bank of Things” that unlocks the value of lifestyle assets

Welcome back to The Innovation Armory! Today’s piece is about Twig’s revolution in consumer finance that is helping users realize liquidity on the value of their lifestyle assets including electronics, apparel, toys and more. This financial unlock fundamentally changes the way consumers will think about their own personal net worth and will have dramatic spillover implications for their consumption, banking and investing habits. Thank you to Geri Cupi (CEO & Founder) of Twig for sharing your perspective for this piece. Read on for more about:

The generational shift towards sustainable consumption and rising popularity of the minimalist lifestyle

How the “Bank of Things” model is superior to both the peer-to-peer and reseller business models

How Twig enables instant cash out on lifestyle assets

The connection between green personal finance and driving more aspirational retail purchases

BNLL? Buy Now, Liquidate Later and how it will change consumption and investing incentives

The “Bank of Things” as a green and personal sustainability operating system

Why Twig’s finance-focused model is superior to traditional pure play B2C and B2B carbon offset approaches to sustainability

This is a long post so if your email gets clipped at the bottom, make sure to click unclip / visit The Innovation Armory to check out the full read.

If you liked this piece feel free to subscribe below:

Or share with your friends :)

Marie Kondo sparked a cultural revolution around love for tidying our living spaces and helped tie our personal identity and psychology to which possessions we choose to keep. She famously said: “It's important to understand your ownership pattern because it is an expression of the values that guide your life. The question of what you want to own is actually the question of how you want to live your life.”

Not only is our personal and cultural identity shaped by what we choose to own, but it even more saliently defines our relationship to the earth. Especially amongst Gen Z and millennials, the choice of which products to own is increasingly influenced by sustainability considerations:

60% are influenced for purchase decisions by brands reducing carbon footprint

90% have focused on making active changes to their lifestyles to be more sustainable, with sustainable fashion and purchasing being a key pillar

The minimalism lifestyle is on the rise amongst millennials and Gen Z, which emphasizes less consumption and ownership and more re-use of goods. This is both impacted by a desire to reduce environmental impact and the cultural impact of “clean-fluencers” like Marie Kondo. It is also influenced by a desire to rebel against the conspicuous consumption of the baby boomer generation and lower purchasing power especially amongst millennials who have been saddled with the largest student debt bill in the history of the US

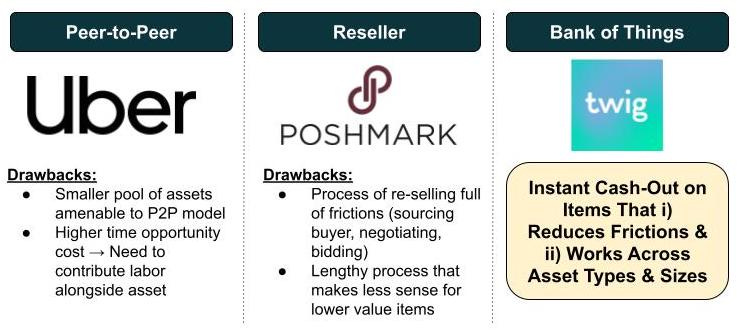

Drives towards minimalism have generated demand for ways consumers and asset owners are able to monetize and extract value out of the possessions they already have, that were previously not thought to be monetizable. Peer-to-peer models and modern re-selling marketplaces are in part a result of this trend:

Twig is revolutionizing these initial business models with a “Bank of Things” model that solves a lot of the frictions of peer-to-peer and reseller systems but also capitalizes on tailwinds in the re-use economy. Peer-to-peer marketplaces (think Uber) only work for a small pool of assets where cost of ownership / alternative service is high (automobile, housing, etc.) and from an asset-owner perspective is highly involved as it requires you to contribute your labor as a driver. Reseller markets like Poshmark are cumbersome processes for sellers where you have to DM and manually negotiate bid prices on items. There is a whole category of consumer goods where the resale price feels too low to even justify the time opportunity cost of finding a buyer:

Twig has created a banking application focused on Gen Z and millennials that starts by helping provide liquidity for goods not traditionally thought of as assets to fund initial deposits. You can liquidate unused or unwanted goods by taking pictures of objects you want to get rid of, get a quote within 30 seconds for the price of the items and then instantly cash out into a bank account opened within Twig. In the background, Twig is a market maker that generates cashout value for your goods either through i) selling them into 50+ different resale marketplaces or ii) executing on pre-designated bids from brokers who agreed to purchase the goods at defined parameters of prices. For all of those hoarders out there, you are in luck, you can now clear your stash and earn meaningful dollars in the process. That is part of what is so magical about Twig’s platform: it turns an unwanted activity like cleaning (that many people don’t enjoy) and transforms it into a money-making opportunity, thereby also aligning our personal financial incentives with doing the right thing for the environment since goods are resold and help fuel the circular economy. Twig is the first grassroots financial platform I’ve seen that aligns individual financial incentives with environmental goals around reduction in consumption and waste. Now that Hoarders is officially canceled by A&E, you can now make money by transforming your hoarding habits:

I caught up with Geri Cupi, CEO & Founder of Twig to learn more about the current state of Twig and his vision for the future of finance and the circular economy:

“Twig is redefining wealth. Traditionally, the generation of wealth is thought to occur in higher end assets, houses, crypto, cash. Most people don’t think about the value of everyday items like phones, toys and our wardrobes. At Twig, we are tokenizing real world assets and make it very easy for people to liquidate them, earning cash and powering a greener, circular economy while simultaneously banking. Our users can get paid in dollars in less than 30 seconds. We make it easy to convert an old iPhone into USD instantly.”

To enable this liquidity layer in its banking app, Twig works with resellers like Poshmark in the apparel space to refurbish, re-sell and recycle goods that consumers cash out of. There is a growing ecosystem of emerging players in other consumer goods categories like jewelry, apparel and electronics that are providing the nodes to cash out and easily recycle and refurbish lifestyle goods. A couple of players in this space specifically for technology include Grover and Circular, which are renters of consumer electronics subscriptions for end consumers. While circular retail subscription businesses do purchase many of their products directly from manufacturers today (often from returns pools), these types of businesses will benefit meaningfully from the proliferation of Twig’s Bank of Things model because the liquidity layer becomes a means for circular retailers to source more product inventory at cost effective prices.

Changing the Equation for Retailers

If you want to buy a Gucci handbag, it will run you an average of $2,400!!! You might even consider pairing it with Gucci’s new Gucci Gucci Goo baby onesie:

For all discretionary goods, amongst those that see value in a product there are those that are buyers at today’s market price and aspirational buyers. Aspirational buyers might see value in a product but not feel comfortable stretching to today’s price. Much of industry assumes that reseller markets are bad for retailers’ new item sales because individuals will become more likely to buy cheaper, refurbished products vs. buy directly from a manufacturer. However, there is also a countervailing force on elevating the purchasing power of aspirational consumers to be able to afford goods with more expensive gross ticket prices. By providing frictionless access to reseller markets and brokers for liquidity, Twig can help incentivize more aspirational purchases for retailers by lowering the total cost of ownership for new retail items.

If you are an aspirational Gucci consumer and you buy a bag at $2,400 today, but know based on historical cash out, that you can resell it in two years at $1,000, your net effective purchase price is only really $1,400 (excluding present value effects). This opportunity is incredibly powerful for retailers who work with Twig and resellers collaboratively in order to drive more high-value aspirational purchases. Retailers that integrate with Twig can show live resale values of goods through their platform to educate consumers about what the net expected price would be post resale depending on how long that consumer wants to hold the product. Being able to extract live reseller data to show lower net effective prices, will help drive greater volume of throughput for consumers that actually have higher net purchasing power than they know today.

At scale, this innovation changes the calculi about which retailers will perform well long-term. Retailers that view refurbished marketplaces as collaborative partners rather than encroachers on market share will be better positioned to wield this aspect of the circular economy to their own benefit. Moreover, If resale value data becomes incorporated into initial purchase decisions, quality of the garment and ease of resale will become some of the most important buying factors. This will be disadvantageous to fast fashion models that have thrived by making cheap goods quickly with a disproportionately high carbon footprint. It will become costly for retailers not to focus on resale quality to the extent their peers are. I believe this will turn one of fast fashion’s historical strengths into its greatest weaknesses especially for Gen Z and Millenials who will care more about garment quality for both environmental and financial reasons:

In terms of its relationships with retailers, Twig’s model is akin to a Buy Now, Liquidate Later. I’m hesitant to call this “BNLL” because of how out of control the proliferation of BNPL models has become and how many new startup founders are capitalizing on its buzz to market their businesses:

Buy now pay later (BNPL) players earn income by charging retailers transaction fees when consumers shop in-store or online with a particular BNPL solution. Retailers are willing to pay these fees because i) they otherwise would be paying some form of a credit card fee in most cases (but BNPL gives consumers more flexibility) and ii) more saliently, BNPL platforms drive more volume throughput for retailers that more than makes up for any net value / pricing loss from the transaction fee. In essence, BNPL platforms generate most of their value as lead generation and extraction platforms for retailers that enable them to generate demand from and close sales from a wider variety of end consumers. In that sense, BNPL helps retailers increase their total addressable markets from a demand perspective.

Twig’s multi-pronged liquidity, payments, spending and savings capabilities can help create similar value for retailers and eventually trading exchanges by increasing their total addressable market on the supply side. Consumers are able to shop directly through Twig with funds they otherwise would not have had access to (value would have been locked up in everyday items). For retailers that integrate with and partner directly with Twig, this opens up access to an entirely new pool of capital to generate retail leads that were previously unimaginable. The same payment supply could also flow to trading and investing products eventually as well through strategic integrations with the likes of Robinhood or Coinbase. Moreover, because a lot of this value comes from goods that consumers previously assumed were nearly worthless, buy execution is likely to be higher. It’s similar to the reason casinos use chips instead of real money, it feels more like “play” money and adds a degree of mental separation from the person and their wallet.

The Green Financial Services Platform and Personal Sustainability OS

Relative to other peers in the nebobanking space, Twig has chosen a financial services vertical that is both highly differentiated / bespoke but also much more wide-reaching in potential application vs. demographic / interest group focused neobanks (e.g. creators, farmers, immigrants, etc.). The vertical is green and sustainability minded consumers, which quite literally needs to continue to grow if our species is going to survive extinction from the effects of global warming. Especially amongst Gen Z and younger generations, this vertical issue will become the defining one of their generation and so positioning yourself as a bank catering to this rapidly growing preferential vertical is a good place to be. While the appeal is wide-reaching at scale, like vertical neobanks, the vertical functionality is quite differentiated and provides unique value in ability to provide liquidity as a means of simultaneously bettering financial well-being and saving the planet. The software to price goods and the vast breadth of reseller and broker network buttresses this vertical depth. Twig has an opportunity to leverage i) the wide appeal of green practices and ii) its differentiated vertical features to create an explosive wedge to drive the adoption of other financial services within Gen Z and Millenials. The marketing war cry is pretty simple to younder generations:

Save the planet while you bank

Increase your net worth simply changing your banking provider to unlock the value of lifestyle assets!

Prevent FOMO by accessing exclusive deals and assets through Twig’s partner network

You can imagine this banking platform being used as a wedge to launch other interesting financial services applications for Gen Z:

Interestingly, if Twig can incentivize users to take pictures of their lifestyle assets before they want to cash out (effectively digitizing their portfolio of lifestyle assets), there are also really interesting supplemental ways they can use that data to monetize. For example, if Twig has pictures of the current condition of a users TV, desk, couch, wardrobe and more, it can impute based on the condition, the replacement cycle of when users might want to procure a new good and use that data to generate even more effective and predictive marketing leads for retailers. Further, if the AI / ML image recognition is strong enough, there are interesting contextual profiles that could be built of a users’ preferences based on digitizing their personal belongings. It doesn’t take a magician to be able to construct a good guess based on lifestyle asset inventories. For the below: sporty, high purchasing power, woman who cares a lot about her looks.

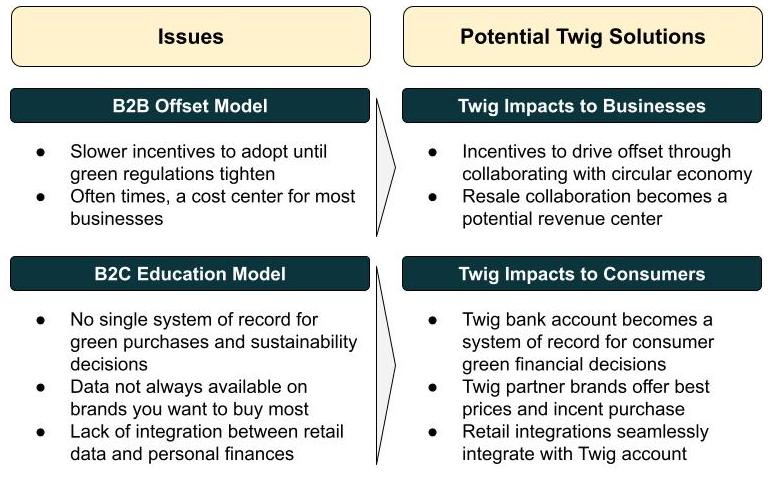

Besides becoming a personal financial hub, Twig is in a unique position to become the operating system to coordinate individuals’ green activities. There are many companies out there in the green data space pursuing two routes: i) B2B model that helps businesses better understand their carbon footprints and offset with projects and ii) B2C model that enables consumers to better understand the footprint of brands so they can make better purchasing decisions. Both of these models suffer from problems that Twig is in a unique position to be able to solve given its focus on green finance:

By tying in investment and retail data with recycling behaviors and a bank account of record, Twig can help close the personal data loop to create unique grassroots level incentives and accountability for personal sustainability initiatives. Similar to B2B and B2C offset models, Twig is even directly building in the ability to offset specific purchases made via Twig accounts through sustainability projects. Tying in green activities directly into a native bank account provides the account, transactional and behavioral visibility to be able to actually hold individuals accountable for green issues. There are also really interesting things that Twig can do at scale in terms of offering rewards points, preferential interest rates, superior cash out, etc. depending on individual behavioral patterns related to sustainability. A bit dystopian, kind of like the social point system in black mirror, but tools that might become necessary transformers to fit capitalism to mesh with our drive towards sustainability:

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.