The Adventures of Robinhood’s Retail Revolution in Emerging Markets

The Adventures of Robinhood’s Retail Revolution in Emerging Markets

How Chaka, Thndr, Infina and Trii are printing local retail traders passports for global financial inclusion

Welcome back to The Innovation Armory. This week’s piece takes you around the world to better understand the state of retail stock trading across various emerging and frontier markets and the players that are aiming to democratize investing access in these countries. Thank you to Seif Amr (COO & Co-Founder of Thndr), James Vuong (CEO & Founder of Infina), Tosin Osibodu (CEO & Founder of Chaka) and Esteban Penaloza (CEO & Co-Founder at Trii) for sharing your perspectives for this piece. Read on for more about:

Why the barriers to stock market participation remain high in emerging markets including Vietnam, Nigeria, Egypt and Colombia

The massive opportunity for players like Thndr, Infina, Chaka and Trii to educate, democratize and elevate emerging market economies through participation in global equity markets

Quantifying the conservative, theoretical valuation potential of these business models at scale by country

How cultural attitudes toward risk and collectivist identity impact fintech business models around the world

The importance of in-product and GTM focus on education in the investing tech sector when building for local communities

How leading players in the space have de-risked their business models from day one through creative partnerships with incumbent brokers

Why the public markets could get even whackier and weirder as large pockets of emerging market capital supplies come online around the world

If you’re interested in more thought pieces, you can also subscribe below for future updates from The Innovation Armory:

Also, If you like this piece, feel free to share with the link below:

The State of Retail Trading in Emerging Markets

By now, everyone in tech (actually anyone on the internet) knows about the digital retail trading boom catalyzed by mobile trading platforms like Robinhood, with retail traders accounting for nearly 24% of trading volumes to start this year. If this is news to you, please get out from under your rock:

What is less spoken about is the incredibly untapped opportunity to democratize access to US, developed markets and local equities in emerging markets… and the players who are leading the charge in their home countries. As I discussed in Play to Earn is About A Lot More Than Gaming, many investors in the West under-estimate the status quo prevalence and penetration of smartphone technology and quality broadband connections in emerging markets. Just as virtual worlds are creating digital employment opportunities for the ascending world through play-to-earn games, local trading platforms are leveraging the same mobile and broadband infrastructure to provide financial passports to their users to access high quality and stable investment opportunities. For purposes of this piece, I am going to focus on 4 markets in particular: Nigeria, Egypt, Colombia and Vietnam which have all been attracting increasingly more venture funding relative to their emerging market peers as of late and are top 30 countries by total population size. The trading platforms leading the way in these markets for retail investors are Chaka (Nigeria), Thndr, (Egypt), Trii (Colombia) and Infina (Vietnam).

In these emerging markets, access to stock trading is still largely a luxury for the rich:

Fees - Access happens through local brokers with legacy business models that charge expensive / extractive fees

Minimums - Account minimums are out of reach for the average local citizen

Geography - Brokerages are often offline and concentrated in tier 1 cities, which excludes a very meaningful portion of the population that could be reached via smartphone instead

Education - Many lack the educational tools to understand how to open an account with a broker and the value of equity ownership

Banking Penetration - some of these countries still have meaningful unbanked populations, which complicates account funding and cash out processes. The neobank funding boom discussed in Waking the Sleeping Giant in the Global Financial System and the rise of mobile wallets are helping alleviate this problem

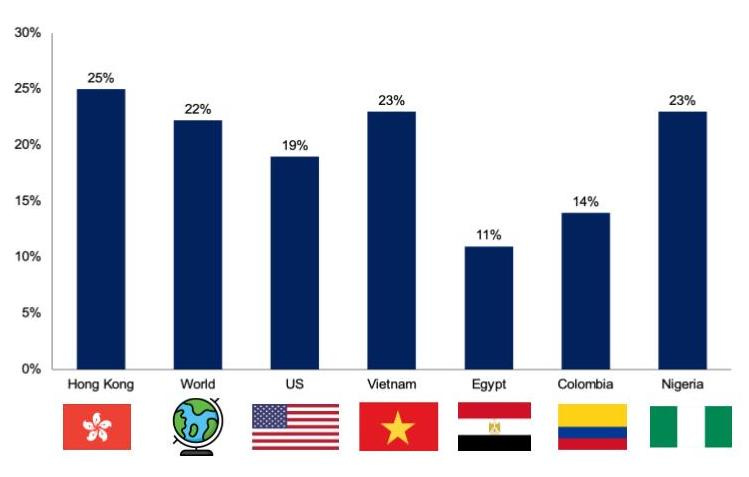

These emerging market digital trading platforms are capitalizing on a mobile first, low / no fee and education forward approach to reaching potential traders. If you look at World Bank estimates of Total Value of Stocks Trading as a % of GDP, this group of emerging market countries lags behind meaningfully with the highest still 87% lower than the US and the lowest 107% lower than the US:

This is certainly not a perfect proxy for stock access as it includes all trades and there could be cultural differences / variations in professional trading activity that inflate figures for certain countries. I included Hong Kong to show this point which has a stock trade value / GDP rate of 886% vs. the US at 108%. Hong Kong has a disproportionately large share of financial services firms based there relative to its economy’s size which inflates this figure, which means the average trader is more likely to be a) an institution and b) have a much higher trading velocity than the average global citizen. It would be inaccurate though to say Hong Kong has nearly 9x more access to equity markets than the US though. Putting aside these fringe case issues using these metrics as a proxy for access, my broader point is that these emerging markets are way below the global average. It is possible these countries never reach parity with the US or similar markets on this metric because perhaps there is a cultural mindset difference that makes the average trader hold stocks for longer and trade less frequently. The best data set to compare here would be public equity assets held by citizens at year end in each respective country. Unfortunately, that World Bank data does not exist. However, the extent of the difference today is still an indicator of unequal access.

These figures are even more interesting when you compare them to the National Savings Rates as a % of GDP for each of these countries:

Vietnam and Nigeria actually have higher savings rates than the US, but the US has 5x and 108x higher stock trading rates vs. national GDP respectively! Many of these countries, especially for Gen Z and Millenials have some of the highest savings rates because of a greater cultural tendency to live at home with parents / extended family, leading to a greater ability to save and rely on parents for income. You might be wondering, maybe citizens of these countries have disproportionate access to other yielding assets so the World Bank statistics are under-representative? Cryptocurrency is certainly increasing especially through the use of stable coins in emerging markets, but is far from mature penetration. What asset do you think is the most commonly held in many of these countries today? Guess who? Cash either physically or digitally through a mobile wallet:

I caught up with James Vuong, Founder & CEO of Infina, building Vietnam’s Robinhood to learn more about how truly under-penetrated the retail investing opportunity is in Vietnam:

"When you have 100M people, a majority of whom are Millennial and Gen Z with accelerating adoption or usage of digital products / services, combined with risk seeking behavior in investing, from stock to cryptocurrency, the opportunity to build Infina to be the on-ramp to existing and emerging asset classes for Vietnamese is very compelling."

To truly understand how much more meaningful developed market investment opportunities are in these emerging markets, it is important to remember that the currency that this cash is held in often depreciates relative to the US dollar on a regular basis per annum. So while, the average US retail investor historically earned a 7% return over the prior 20 years, all of these currencies depreciated relative to the US dollar on an annual basis over the prior 10 years. Note: I used 20 years for the equity returns so as to not inflate too much by the recent bull run.

Let’s focus on stocks specifically and put aside cryptocurrency for purposes of this discussion, which although volatile could also yield an even a better returns profile over the long-term. In fact, there are many players in these same countries building out more intuitive user interfaces for cryptocurrency trading including Yellow Card and Busha for Africa. For citizens that hold their net worth in cash in these countries, they are generally losing purchasing power each year vs. the US due to a depreciating currency. The opportunity for them is the nominal return rate + the depreciation rate vs. holding local cash. It also means they are likely to be willing to accept a meaningfully lower market rate of return (I’ll discuss the implications of this later in detail). It is riskier to hold your money in cash than in equities. Imagine how meaningful access to these sorts of opportunities would have been in countries where currencies have collapsed overnight, including Venezuela.

Back to the World Bank data, if you converge the data from the two charts, the normalized world average ratio of (stock rate / savings rate) is 3.8x. If you assume a discount in trading frequency for emerging markets due to a cultural tendency to hold assets longer vs. speculate (which may not be true in many of these markets), you can calculate incremental normalized trading volume that should be activated over the long-term as these retail trading markets come online assuming a constant savings rate over time.

You can further calculate revenue levels for retail trading platforms at a more normalized scale assuming an illustrative value capture by these platforms. This value capture is not meant to literally mean a take-rate on trading volume (these business models don’t work that way except for PFOF revenue as we’ll discuss later) but rather an illustrative assumption of how much value these players will be able to capture from incremental trading volume, treating is as a proxy for economic value creation. This value capture could take the form of revenue streams these companies are able to unlock from other financial products by virtue of gaining customer loyalty through access to equity trading. More on this later. Looking at Robinhood’s recent EV / revenue multiple you can impute a future valuation. With relatively conserative assumptions you can get to ~$550 million of combined revenue potential and $3.6 billion of enterprise value across just these 4 geographies. I think there are a lot of conservative assumptions here:

I apply the incremental trading % to current GDP, not future GDP. As foreign residents gain access to capital gains in more developed markets, there is a reasonable case to make this will further catalyze even more GDP growth (above historical norms) as there will be more capital to spend in their local economies from gains

There is a case to make that some of these countries could see higher trading frequency because users recognize the even greater income potential of optimizing your trading relative to lower wage cash labor opportunities

In certain of these countries (especially Egypt and Colombia), savings rates will likely go up with greater financial access and more economic growth because greater investment income will help create surplus above today’s needs

I think the 0.1% value capture is relatively low especially when fintech product penetration is meaningfully lower in these economies and there is an even greater opportunity to leverage equity trading as a loss leader to acquire users to cross-sell to other banking and fintech products over time

I took a 30% discount to Robinhood’s multiple as of the time I pulled the data because the market has been so hot but who really knows where multiples will be when these businesses are at scale?

A Case Study of Cultural Impact on Business Model

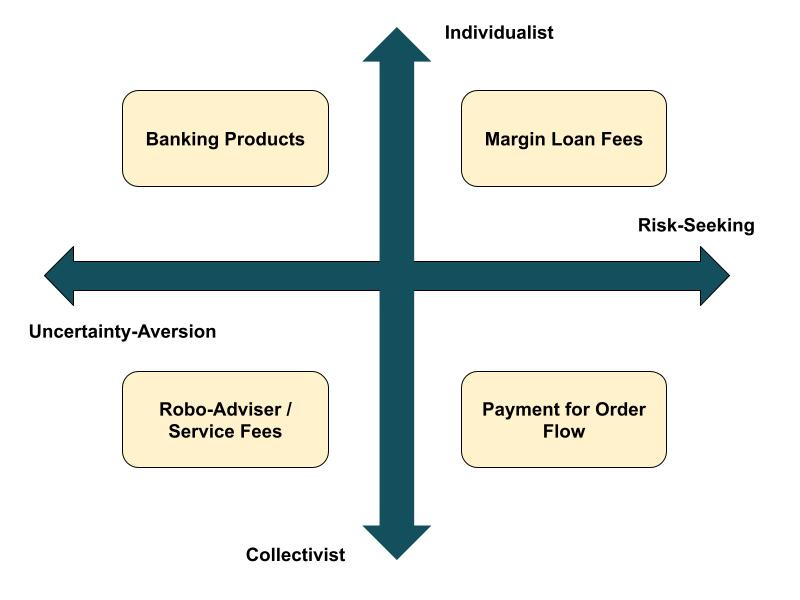

Stock trading platforms provide infrastructure to coordinate the investing activities of millions of people. While the efficient markets hypothesis assumes that all actors are rational in the market, the concept of what is “Rational” is inherently impacted by individual psychology, which is meaningfully influenced by a geography’s culture. Even if rational actors come to similar conclusions, the “when”, “where” and “how” of that conclusion will diverge based on psychology. Especially in the case of financial markets where individuals’ financial wellbeing is at stake, cultural psychology can impact factors like trading cadence, value prescription and capital deployment levels. These trading platforms inevitably make money using a variety of methods including payment for order flow, lending, subscription fees, interest on uninvested cash and more. However, I believe that cultural characteristics can dramatically influence which monetization model will drive the highest potential revenue stream. Two of the most relevant cultural characteristics here are the uncertainty-avoidance / risk-seeking and individualist / collectivist spectra:

The US is highly individualistic and also has some of the largest risk-taking tendencies. This is why a lot of the greatest global innovations have come out of the US throughout history. When a meaningful population of traders makes a variety of high risk-seeking trades, the interest on margin loan fees can help subsidize other parts of the business especially on especially risky / speculative instruments offered like the triple levered VIX index!

In collectivist cultures, there is a greater tendency to see momentum-based speculative trades, which means brokerages can see even higher volumes of trades based on trading patterns of one’s peers. Meme-trading is an odd form of psychological collectivism. When there are dueling collectivist-fueled momentum trades (both short and long), payment for order flow (PFOF) is a great way for brokers to earn more by capitalizing on volume on both ends of a trade. In more uncertainty-averse cultures, individuals generally will tend to want to hold their assets for longer and generally view their investing as less speculative. Where this is combined with individualism, where individuals are both risk-averse but also demand an even more bespoke, customized financial experience, trading can be an interesting wedge into offering personalized digital neobanking products. Because individuals hold their funds for longer, these users view their brokerage accounts as more of a savings account. This can create an interesting opportunity to leverage savings-like broker accounts as a wedge to sell personalized bundles of fintech products. In the case of both collectivism and uncertainty-aversion, the average individual is less likely to believe they can beat the market and more likely to trend towards passivity in their investing strategy, which can lend itself to more of a robo-advising or a greater willingness to pay fees fees into pooled advisor funds.

I caught up with Esteban Penaloza, CEO & Co-Founder at Trii to learn more about some of the unique cultural differences in Colombia and how that impacts his business model and vision for Trii.

In our conversation, Esteban highlighted how culturally many Colombians view their investment portfolio through much more of a long-term mindset relative to other cultures where day-trading and short-term transactions are more common. In effect, investing / brokerage accounts are culturally more akin to savings accounts. This implies that transaction fees and margin loans might be a worse business model, whereas building other fintech products around a pinnacle savings account could be an interesting strategy.

Leaning in on Education

In these emerging markets, lack of financial education is both a barrier and large opportunity. The platforms that first establish best-in-class local educational brands on financial literacy, will garner a meaningful and sustainable competitive advantage over future entrants by tying together community and educational empowerment. It can be difficult to get individuals initially into your ecosystem though because they don’t necessarily even appreciate the financial upside opportunity. Breaking through this barrier requires a dual-pronged approach of leaning in on educational initiatives:

First, from a product perspective through building in budgeting tools to teach individuals how to better manage their finances. Also, I think fantasy equity investing options are particularly important to demonstrate the power of capital compounding over time without forcing individuals to risk their own capital especially in more risk-averse cultures. The fantasy investing angle can help create a localized social layer to investing that gamifies finance in a way that is much more approachable to the average user. But without the ridiculous sh*&-talking endemic to fantasy football… is this good or bad?

And Second, from a go-to-market perspective, newsletters, podcasts and educational finance content can help drive a thriving community. Many of these economies lack local language content that is custom-made for their market. These sorts of community-focused go-to-market initiatives can help drive referral programs and viral word-of-mouth marketing by changing the narrative on who gets to be involved in finance and can make user acquisition that much more efficient

I caught up with Seif Amr, COO & Co-Founder of Thndr, Egypt’s leading retail investing app to learn more about how he has built education into the DNA of his product and his go-to-market strategy by building Egypt’s leading grassroots newsletter:

“Naturally, Egypt is not at the financial literacy level as the US; and this is reflected in the numbers - less than 0.5% of Egyptians invest compared to +50% in the USA.

To offer a culturally relevant service in our region, it wasn't enough that we make access to investing seamless. We needed to take one step back and really focus on the literacy piece by coupling easy account opening with a strong educational push. We designed our material and delivered it in a manner that is compatible with how everyday individuals are currently consuming information and data - Our curriculum includes the following:

Simulator - Risk free way to practice investing with virtual money and app introduction

Podcasts (link)

Webinars (link)

Thndr Learn - Bite-sized articles that are written in-house (link)

Thndr Score - Alternative to fundamentals research that is digestible by unsophisticated user, developed in partnership with the American University in Cairo (initiation blog)

Thndr Claps - Daily bite-sized roundup of major news in a simple manner (link)"

Creative Partnership Approaches

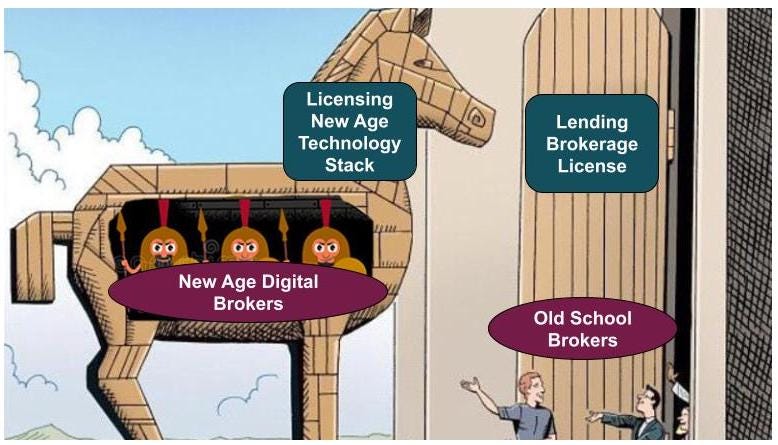

The regulatory process for getting a brokerage license can be cumbersome, lengthy and costly (potentially more than a year, lots of legal fees and tens if not hundreds of thousands of dollars). Plus these licenses need to be procured with each market a player is looking to broker securities in, e.g. with a local regulatory commission for regional securities but then also with the SEC for US securities. This is especially problematic of a dynamic for a startup where fast iteration, low cost improvement and minimal barriers to entry are what enable stealth players to compete with incumbents. Players in the digital brokerage space have gotten really creative with the types of partnerships they have struck to start acquiring and servicing these users while bearing minimum costs.

A lot of these players have started out by forming strategic partnerships with local, incumbent brokerage firms, effectively borrowing their licenses and routing trade traffic through them, powering a better user experience with digital technologies. Paired with community-building and educational features and initiatives, brands can begin to build up a user base, leveraging existing brokers as their regulatory north star and can eventually aim to capture their own user demand once they acquire their own license. For example, Chaka initially partnered with DriveWealth for US Securities and Citi Investment Capital before acquiring its own license in 2021. This strategy lets new digital brokers experience the best of both worlds in a complex, regulated industry: startup speed and license compliance. In the short-term, this is a win-win situation where incumbent brokers get to leverage digital technologies that otherwise their core competencies would not allow them to build and new brokers get to start testing their product and building retail trading communities:

Over time, while these incumbent brokers may get a short-term boost in user acquisition, trade flows and user experience from working with an up-and-coming digital broker, these new-age brokers can become competitive with their core business the moment they are able to procure their own license. It is a really interesting trojan horse strategy that has allowed digital brokerage apps to take local trading firms by storm:

I caught up with Tosin Osibodu, CEO & Founder of Chaka, to learn more about the evolution of Chaka’s business model and how it has impacted their perception of the importance of strategic partnerships:

"As a technology company, we always believed that the right companies would provide a quicker go-to-market and allow us to scale much faster. Even though we've now got our own independent license, seeking the right partnerships is an ethos within Chaka that will continue to leverage for growth"

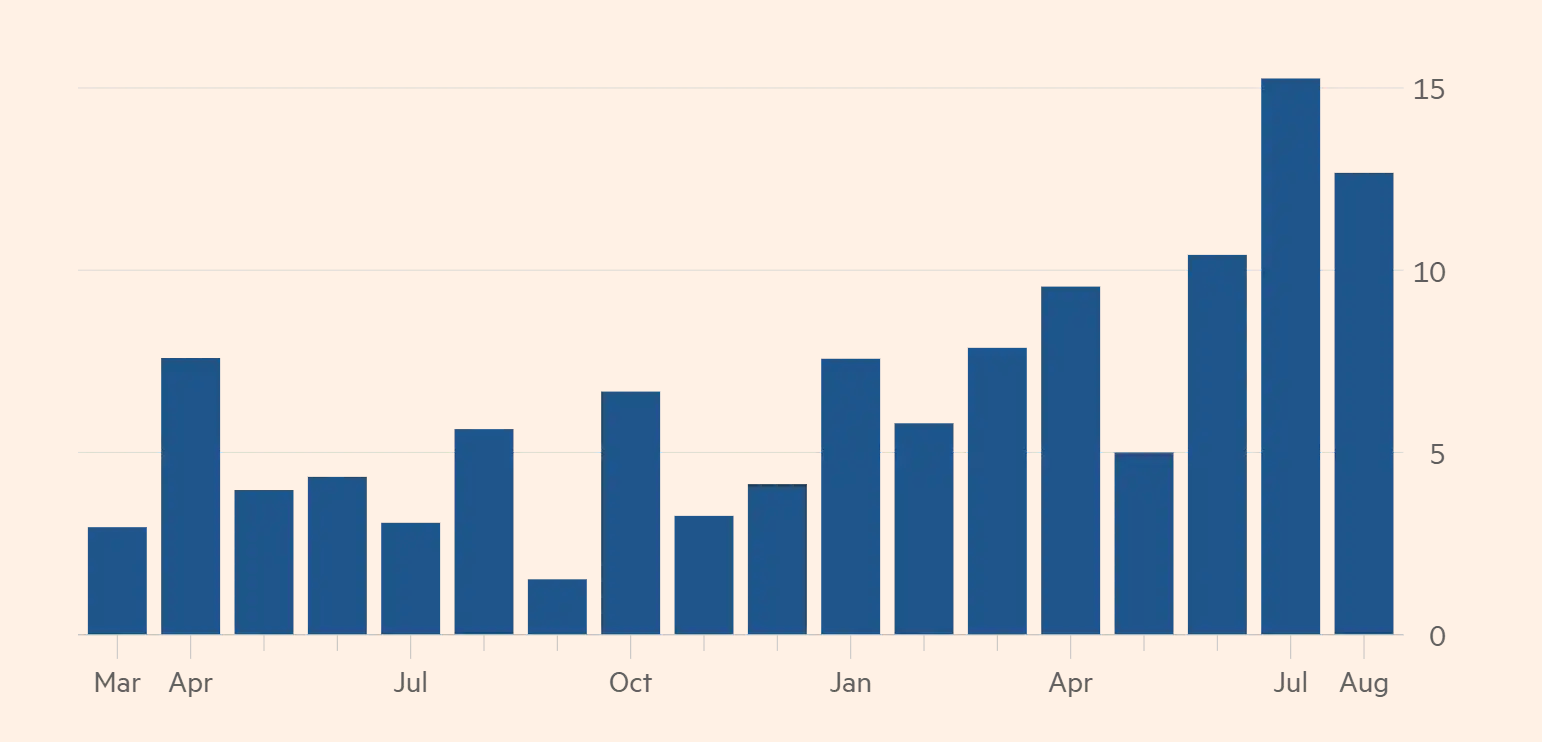

Unlocking Even More Capital Supply in Public Markets

Some economists attribute strong equity performance through covid-19 to a rising surge in retail investor participation in the stock market. Net retail equity deployed increased pretty rapidly over the summer per Financial Times:

There are many different theories of why this retail boom has caused stock prices to balloon:

Simply that greater trading participation means a greater supply of capital is chasing the same pool of quality assets, driving those prices higher

YOLO culture of meme traders

Increased risk appetite of retail investors for leverage and the riskiest of securities

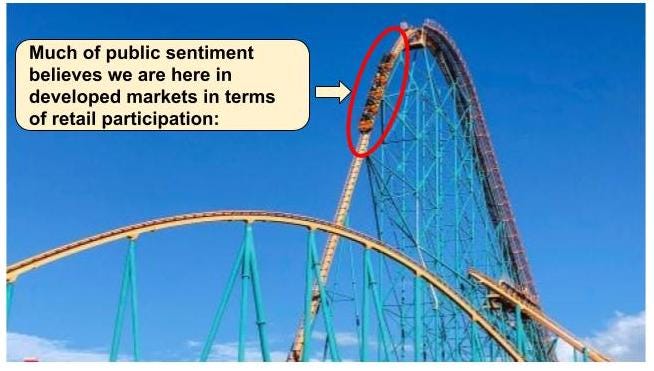

I want to focus on #1 above. Market sentiment of a lot of the public is that we are relatively advanced in developed markets in terms of retail investor participation / saturation in stock trading especially after the boom through covid-19:

However, there are BILLIONS of people in emerging and frontier markets that are not participating in developed market stock exchanges yet. Wages to many of these workers are the input costs that create products sold by some of the largest companies in the S&P 500 and the Dow, yet they don’t share in any of the upside of the financial market where the average American / European has earned a 7% average return historically. In fact those wages have lost purchasing power through currency depreciation. Where will we be when we factor in these billions of retail traders who are offline? To use a different carnival analogy for the Super Shot, a ride everyone knows is better than your generic roller coaster:

As discussed earlier, when your alternative is cash depreciating multiple percentage points per year, you probably don’t need to expect to earn a 7% return to deploy your capital into equities. Perhaps investment becomes a means to preserve value, let alone earn a positive yield. When we start lighting up pockets of demand and access for equities in developed markets, we are potentially introducing a large supply of trader capital that is even less price sensitive relative to capital preservation opportunities locally. Look at the effects that explosion of retail trading in more developed markets already had on valuations, trading velocity and volatility. No one knows what will happen but I am incredibly curious about what will occur as billions of potentially lower-returns accepting investors are lit up online:

The impact will be heavily influenced by the extent to which this capital is redirected into developed markets abroad vs. invested in known brands / companies on local and regional exchanges

Will we see stock prices soar even higher in the short-term because some of these investors are willing to accept a flat or negative return so long as it is lower than the depreciation of their own currency relative to the US dollar?

Will the prices of a select few businesses with truly global brands that are recognizable to the average retail trader in emerging markets balloon the most? Think Coca-Cola, Google, Facebook (WhatsApp)?

Will developed market investors leverage regional digital brokers like Thndr, Chaka, Infina and Trii to gain greater access to riskier, local frontier market investing opportunities? Will this flow of emerging market capital into the developed world counter-intuitively chase more developed market capital into frontier markets to seek higher yield amidst potential public yield compression in the developed world?

Will all of these impacts be dampened from a stock perspective by millennial and Gen Z emerging market investors flowing a greater portion of retail capital into crypto assets rather than traditional equity assets?

No one knows what will happen but with the number of emerging and frontier brokerages popping up, it is certainly foolish to think that this flood of retail traders abroad, especially in those frontier economies growing the fastest, won’t have a large and measurable impact on international capital flows.

All Innovation Armory publications and the views and opinions expressed at, or through, this site belong solely to the blog owner and his guests and do not represent those of people, employers, institutions or organizations that the owner may or may not be associated with in a professional or personal capacity. All liability with respect to the actions taken or not taken based on the contents of this site are hereby expressly disclaimed. These publications are the blog owners’ personal opinions and are not meant to be relied upon as a basis for investment decisions.